June's product updates are here, and there's a lot to be excited about. We're continuing to build on the foundation we've established across Catalyst and Insights benchmarking, with this month's updates focused on giving users more precision in how they search, prospect, and manage data.

Author:

June 2, 2026

June's product updates are here, and there's a lot to be excited about. We're continuing to build on the foundation we've established across Catalyst and Insights benchmarking, with this month's updates focused on giving users more precision in how they search, prospect, and manage data.

On the Catalyst side, that means expanded AI assistant capabilities, more flexible export controls, and deeper CRM customization. For benchmarking, we've added AI-powered recommendations and made meaningful improvements to the report experience, including how you access completed reports and how data flows through the submission wizard.

Read on for the full details.

Catalyst

Proximity-Based Geographic Search — The AI assistant now supports radius-based company searches around a city, so territory prospecting works the way territories actually do — not just by state, city, or zip.

Product Line Gap Queries — Ask the AI assistant which product lines — Stop Loss, EAP, Voluntary, TPA — an employer has or is missing. Cross-sell identification now happens in a conversation, not a spreadsheet.

Headcount Milestone Flags — The AI assistant can surface employers who've recently crossed key thresholds: 50, 100, 500 employees. Growth signals and compliance triggers, surfaced automatically.

Flexible Export Range Selection — When exporting data, users can now choose the current page, a page range, or a specific record count. Providing precise control without bumping into system limits.

Experience Mod Data on Account View — Experience Modification data now appears directly on the Company Overview and Commercial P&C tab, so risk context is right there when you need it.

Custom CRM Field Mapping — Account admins can now map platform fields to custom CRM fields, including custom schemas. Providing full control over how data flows in without overwriting existing records.

Retirement Search: Total Assets Filter — The Retirement Search Assets filter now filters on Total Assets.

Insights+

AI-Powered Recommendations in Insights+ Users can now access AI-generated recommendations directly within Insights+. The new recommendations tool surfaces actionable guidance across four categories. Highest Impact, Cost Strategy, Coverage Gaps, and Underwriter Notes, giving users a faster path from report data to next steps.

Completion Email Links to HTML Report — When your report is ready, the notification email now links directly to the interactive HTML report including Mployer AI and all report tools, instead of a PDF download.

Redesigned Chart Layout — Plan Score and Cohort Market Data sections are now clearly differentiated, and Dental and Vision pages consolidate their left-side tables. Easier to read, faster to interpret.

Report Opens Without Losing Your Place — Clicking a company name in the Request History Grid now opens the HTML report in a new tab, so your search state stays exactly where you left it.

Rate Availability Edits No Longer Clear Rate Data — Adjusting Rate Availability selections mid-wizard no longer wipes Medical, Dental, or Vision rate and contribution data previously entered. No more lost work.

Age-Banded Entry Hidden When Not Applicable — When 'Use employee contributions only' is selected, Age-Banded rate entry is no longer shown — cleaner form, fewer distractions.

That's a wrap! Stay tuned for what's coming next month.

Insurance brokers can help your business choose policies and coverage types that make the most sense for you. Their job is to help clients understand their liabilities and how those risks can be managed through proper insurance coverage.

Insurance brokers do not sell insurance, but they can find insurance companies and coverage policies that align with your business, and then negotiate with multiple insurers to find competitive rates.

To finalize and initiate a business insurance policy, you or your insurance broker will need an insurance agent working on behalf of the insurer to close the deal.

In this post, we explain the difference between insurance agents and brokers, who pays an insurance broker, and companies’ requirements for business insurance.

What are insurance agents and insurance brokers?

Insurance brokers help you review and shop insurance and benefits policies best suited for your needs and your budget.

The main difference between an insurance broker and an insurance agent is whom they represent. Insurance agents represent one or more insurance companies, but when you hire an insurance broker, they work directly for you not the insurer.

While independent agents work with more than one insurer, they have contracts with companies that often limit them to selling certain policies. Brokers, meanwhile, can solicit price quotes from multiple insurers. So, you can think of an insurance broker as an intermediary between insurers and businesses, with no stakeholder interest in the policy itself.

Importantly, you can't buy insurance from an insurance broker, but they can help you find the best policies and manage claims. Put another way, an insurance broker cannot complete the sale of a policy that right is reserved by the insurance agent or insurance company. Once a broker has done all of their research and presented their clients with options, the policy selected must be bound by an insurance agent or company.

Independent agents and brokers approach their work similarly, because they can offer several policy options from multiple insurers. Captive insurance agents, meanwhile, work on behalf of a single insurer, and brokers are not contracted with any insurers.

Are companies required to use insurance agents?

Regulations require each company with employees to have workers’ compensation insurance, and most states have additional requirements. These typically include policies such as general liability for lawsuits or business property insurance for workspaces and equipment.

In some cases, you are legally required to purchase certain types of business insurance. Since insurance companies may require state licensed insurance agents to sell their products, companies purchasing business insurance may be required to use insurance agents.

Some states do not recognize brokers and only license agents for insurance. With insurance being state regulated, each state handles brokers and agents all differently.

Many insurers rely on agents and brokers to distribute their business insurance products. They don't often sell policies directly to businesses, due to regulations and industry best practices. If you do not use a broker, you will most likely have an assigned agent at each company you contact.

To initiate policy coverage for a business, a broker or agent must obtain a binder signed by an underwriter or other representative of the insurer.

The type of license an agent or broker needs depends on the state and the type of insurance coverage required.

Good brokers and agents stay on top of legislation changes and tax reforms, making sure your policies are up to date. They can help ensure you are covered for unexpected legal and tax issues related to your insurance benefits.

Who pays an insurance broker?

An insurance broker makes money from commissions when your business buys and renews policies from insurance companies, along with any broker fees, if applicable. They may charge both commissions and fees, or only a commission.

Insurance broker commissions

Commissions are typically included in the price of the annual premium charged by insurers to policyholders. These could include base commissions and supplemental commissions, which are smaller, ongoing annual payments.

Most commissions fall between 2% and 8% of premiums, according to Investopedia.

Insurance broker fees

Brokers may also be paid broker fees, which can be combined with a commission structure.

Broker fees are usually non-refundable, so your money will not be returned if you cancel your policy mid-term, unless your insurance broker was dishonest or broke your contract. Fees are generally paid directly to the broker, but in some cases are included in annual premiums.

You should know if your broker or agent charges fees, and what those fees are, before they start searching for insurance policies on your behalf.

Are you ready to find a top rated insurance broker that can find you a cost effective policy that best fits your needs? Search for a broker with Mployer Advisor’s online broker marketplace.Looking for more exclusive content? Check out what’s trending on the Mployer Advisor blog, and be sure to catch the latest episode of This Week in Benefits.

The article explores the hourly cost for hiring an insurance consultant, including the factors that affect the cost and the average rates in different regions. It provides insights for employers who are considering using an insurance consultant to navigate the complexities of the healthcare system.

As regulations and business expenses rise, so has the value employers place on advice about insurance and benefits. Insurance consultants and advisors are sought for many risk management and insurance services.

The hourly fees for an insurance consultant depend on the size and complexity of the insurance policy being taken out, along with the scope of the consultant’s services.

It is critically important to know what is included in standard fees and/or commissions for consultants, advisors, and brokers as you look for help with insurance and benefits.

In this post, we explore what it costs to hire insurance consultants and what makes these advisors valuable.

What Does It Cost to Hire an Insurance Consultant?

The cost of using a consultant to insure your business depends on the type of business, amount of coverage you need, optional coverage policies, and complexity of your insurance and benefits management.

A consultant’s fees, also called “intermediary fees,” are fees that insurance buyers pay consultants or brokers on top of a policy’s premium. The cost to hire an insurance consultant ranges depending on the size of your company, your operations, and complexity of the insurance policy or services provided.

Broadly speaking, commissions and fees usually fall between 10% and 25% of the base premium amount. It all depends on your state, your size, and what type of insurance you need, but average consulting fees are typically 15% of the policy premium.

Traditionally, an insurance consultant works on a fee for service, and an insurance broker works for commission based on the policy’s premium.

Consultants usually charge fees instead of, or in addition to, a commission that’s included in your premium payment. This is in the form of a direct invoice of billable hours or direct offset billable hours with commissions received.

As opposed to brokers, consultants are usually not paid commissions from the insurance company, which means they charge a consultant’s fee for services. Unless of course, the client prefers them to receive commissions and offset their billable hours or fees.

Why Hire an Insurance Consultant for Your Business?

A good insurance consultant will understand coverages and policies tailored specifically to your business, and will find ways to maximize protection and minimize cost with your coverage.

Consultants should be involved with your business strategy and involved with you several times per year or as often as you need their services.

Here are key services that insurance consultants offer:

Find and implement insurance policies, advise on employee benefits, offer plan administration and provide compliance documentation.

Create strategic, long-term plans suited to the needs of the business, including financial modeling, risk management and large claims processing.

Competitive benchmarking to assess the role of benefits in recruitment and retention, making benefits a talent attraction and retention tool.

Specialized expertise in Risk Management and Health and Welfare.

How Do I Vet an Insurance Consultant?

There are about 413,000 insurance consultants and associated businesses in the U.S. as of January 2021, according to IBIS World. But how do you vet an insurance consultant to find the one that is right for your company?

Insurance buyers should compare brokers and consultants based on professionalism, demonstrated knowledge in insurance, understanding of your industry, transparency and cost.

When you are looking to hire a broker, consultant or advisor, you can focus on three things: what they do, how well they’ve done it, and how they get paid. The right expert for your business will have a proven track record of helping businesses like yours solve their insurance and benefits problems.

The quickest way to vet your insurance consultant is to visit Mployer Advisor, a free broker marketplace that allows employers to compare licensed insurance consultants in every state.Looking for more exclusive content? Check out what’s trending on the Mployer Advisor blog.

The article discusses the difference between an insurance broker and an insurance carrier. An insurance broker works on behalf of the client to find the best insurance coverage and rates, while an insurance carrier provides the insurance policy directly to the client.

From “policyholder” to “premiums” and “providers,” much of the jargon used in the insurance industry isn’t easy to keep straight. For those unfamiliar with the difference between an insurance broker and carrier, Mployer Advisor outlines the distinction below.

What Is an Insurance Broker?

An insurance broker is a licensed professional who helps businesses evaluate and select insurance policies. Unlike insurance agents, brokers do not work for a particular insurance company. Rather, they represent employers and work to help businesses find the best plans and coverage for their needs.

Some brokers work with individuals rather than companies. However, the type of broker an employer will work with deals primarily or exclusively with procuring insurance coverage for businesses. These brokers are often called business insurance brokers or commercial insurance brokers.

There are several types of commercial insurance brokers, such as health insurance brokers, property & casualty (P&C) insurance brokers, liability insurance brokers and more.

Insurance brokers assess the unique needs of a given employer, then work with insurance carriers to negotiate and select an array of coverage options. For this reason, employers who work with a broker often end up with more choices than those who shop online or purchase directly from an insurance provider.

As a result, employers are able to evaluate a variety of plans and policies that an insurance broker brings to the table. Employers can compare coverage, costs and more in order to select the best plans for their company and their employees.

An insurance broker typically gets paid by commission. Usually this commission is built into the premiums paid by policyholders every month. Thus, it’s not a separate payment, but included in the price of the policy purchased through the broker.

An insurance carrier is the company that actually provides the insurance policy. Also called an insurance provider or insurance company, a carrier offers one or more insurance products to individuals or groups, such as health insurance, property and casualty insurance, workers’ compensation and more.

In other words, a carrier is the company you pay premiums to. They underwrite your insurance policy and pay out for claims.

Examples of large insurance carriers include State Farm, Allstate, Humana, Cigna and Progressive.

Insurance carriers can offer policies for individuals, such as Geico’s car insurance or Liberty Mutual’s life insurance. However, carriers can also offer business insurance which covers a company or a group of employees. Examples include Blue Cross Blue Shield’s group health plans and Delta Dental’s group dental insurance. Looking for more exclusive content? Check out what’s trending on the Mployer Advisor blog.

In this article, the author explains that it is possible to negotiate insurance broker fees and commissions. The article provides tips for negotiating with brokers and suggests that employers should be prepared to ask for a breakdown of fees and commissions and consider multiple broker options before making a decision.

Is it Possible to Negotiate Insurance Broker Fees?

Negotiating the fees you pay to your business insurance broker may be possible, and is largely dependent on the size of your company, as well as the specific internal incentive policies of your insurance provider.

Anytime that fees and especially commissions are involved in business transactions, the first question that often comes to mind for the customer or client is, ‘Can those commissions and fees be reduced?'

Given that insurance is a field in which commissions and fees make up most if not all of broker compensation packages, this is a question that comes up a lot.

In many ways, buyers are almost conditioned to have this response, given that so many industries use reduced commissions and fees as one of the primary incentives to induce a potential buyer into closing the sale. But is that how it works with insurance brokers, too? Can a buyer negotiate their way to lower broker compensation?

In What Situation Might a Company Negotiate Broker Fees?

While far, far less common of an occurrence in the world of insurance than it is in car sales, the answer is that it may be possible to negotiate for reduced fees and commissions with a broker.

The likelihood of that negotiation being successful, however, varies widely depending on a few key factors – specifically, the size of the buyer’s company, the type of fees and commissions in questions, and the policies of the provider with regard to matters of broker compensation.

Company Size: As with many factors involving insurance, whether or not your company is able to negotiate-down brokers fees is largely a function of the size of your company. If you have fewer than 100 employees, it will be nearly impossible to negotiate your broker fees as a general rule. While there may always be exceptions to any rule, this tends to be a fairly firm general guideline.

With more than 100 employees, it never hurts to ask for a fee reduction, though the likelihood of effectively negotiating for such a reduction goes up significantly as your employee pool size passes several hundred and approaches 1,000.

Types of Fees and Commissions: Any attempt to negotiate a reduction in fees or commissions must first begin with a complete understanding of how all fees and commissions are being paid out to the broker. Many states have laws requiring the disclosure of how brokers earn their compensation, and even where such laws aren’t on the books, just about any broker with which you’re likely to want to work will be forthright with such information. As a result, gaining a thorough understanding of how your broker is compensated and incentivized can usually be accomplished simply by asking.

While brokers are more rarely going to be able to offer reductions in their base commission, they may have more flexibility to work with additional incentive compensation such as contingent or supplemental commissions.

Provider Policy: Even if your company is large enough to make negotiating-down commissions and fees feasible, and even if your broker has agreed in principle to such a fee reduction, the specific policies of your provider will most likely be the determining factor as to whether or not such a fee reduction can be implemented.

Similar to determining and having a thorough understanding of all the ways in which your broker will be compensated, figuring out whether such brokerage fee and commission negotiating is even possible is something that you’ll want to do at the outset of the process when vetting various brokers and providers and policies in the first place. Further, along the same lines as determining the ins-and-outs of your broker’s compensation package, if you neglected to inquire about these details prior acquiring your insurance coverage, it’s still never too late to ask!

Why Not Try to Negotiate Your Broker Fees?

Whether or not you and/or your company are ultimately successful at negotiating a lower rate for your broker’s commission and fees, there is little to no downside to inquiring about the possibility.

When evaluating potential new insurance brokers with whom you’re considering working, such a discussion can be a good way to broach the subject of the various ways and contingencies that your broker may be compensated, which is always good information to have available.

In situations where your company may have been working with the same broker for years, raising this issue may be a good way to come by a better understanding of your broker’s compensation structure if you’re not familiar with it already. Additionally, such a discussion may serve as inspiration and motivation to reassess your insurance situation in general, potentially leading to a desire to compare your broker’s and provider’s negotiation flexibility with that of other brokers and providers on the market.

In any case, if such an inquiry leads you to consider changing brokers or reevaluating and potentially refreshing your insurance policies, access Mployer Advisor's searchable database. You can find and contact brokers who meet all the criteria and qualifications most relevant to you and your business.Search Insurance Brokers Near You

This article examines the differences between employer health insurance brokers and employee benefits advisors, and provides guidance on choosing the right type of professional to meet a company's needs. It discusses the services each type of professional typically offers, how they are compensated, and what factors to consider when making a decision.

There are many challenges to overcome when an organization is determining what employer health insurance plan is the best fit for their specific needs. However, there are professionals who can help guide you through the process, such as health insurance brokers, employer benefits advisors, and consultants. What are each of these roles and how do they differ?

To help navigate the potential advantages and pitfalls in their paths, employers and their HR departments have historically turned to outside employer health insurance brokers in order to present them with options and help advise the decision-making process. As the employer health insurance market has in many ways become increasingly complicated over the years (and because there can be a perceived conflict of interest with regard to broker commission structure), additional guidance roles have been established to fill the informational gaps.

Those roles are often labeled employer health insurance advisor/consultant or employee benefits advisors, but - as with employer health insurance brokers – their function is guiding employers toward their ideally optimized health and benefit plan coverage. Given that all of these labels accompany a similar advisory role, one of the main differences is how each may be compensated – although there is a great deal of overlap there, as well.

What is an Employer Health Insurance Broker?

Traditionally, employer health insurance brokers have been the primary means through which companies have attained employer health insurance benefits for their employees. Brokers often work directly with one or more insurance providers and will typically be required at some point in the coverage process even when working with an outside advisor or consultant to build the coverage plan for the employer.

Primary function: Analyze the circumstances of a given employer and provide options to resolve their employer health insurance needs.

Payment and compensation: Typically commission-based, though there are exceptions.

Differentiating factor: Brokers are licensed professionals who work directly with one or more health insurance providers. The options they are able to provide an employer may be limited by their relationships with affiliate insurance providers, but they are also the most direct way to access those insurance providers given that employee benefits consultants and advisors will still need to go through an employer health insurance broker in order to execute the plan.

What is an Employee Benefits Advisor?

Employee benefits advisors primarily serve a complementary role to brokers in an employer’s effort to attain health insurance coverage for the company employees.

In fact, after working with a client to determine the ideal scope of coverage for that client, employee benefits advisors will then assist the client in evaluating potential brokers in order to assess which broker can provide the coverage that best fits the client’s needs.

Primary function: Analyze the circumstances of a given employer and provide options to resolve their employer health insurance needs, including making connections with relevantly specialized brokers and vetting choices in accordance with their clients’ goals.

Payment and compensation: Typically fee-based, though commission-based and other arrangements are also possible.

Differentiating factor: In addition to employer health insurance coverage, employee benefits advisors may take a broader approach to optimizing employee benefits plans and have more tools at their disposal than employer health insurance coverage alone when helping an employer put together a comprehensive benefits package uniquely suited to their organizational needs.

What is an Employee Health Insurance Consultant?

Similar to an Employee Benefits Advisor, Employee Health Insurance Consultants serve a complementary role to brokers. In many ways, the designations of benefits advisors and consultants can be interchangeable, although such designations can be used to convey distinctions between fee structure or the depth of background analysis involved in general.

Primary function: Analyze the circumstances of a given employer and provide options to resolve their employer health insurance needs, including making connections with relevantly specialized brokers and vetting choices in accordance with their clients’ goals.

Payment and compensation: Can be either fee or commission-based.

Differentiating factor: As a term, employer benefit consultant can for the most part be used interchangeably with employer benefit advisor, although using ‘consultant’ may imply a greater degree of emphasis on the initial conditional analysis while using ‘advisor’ typically places more focus on the advisement with regard to selecting from among employer health insurance coverage and brokerage options going forward.

How to Find a Good Employee Benefits Advisor

When selecting someone to help guide your organization through the procurement of employer health insurance – whether it be a broker, an employee benefits advisor, or a consultant – the key questions to ask are what relationships and specialization does this person have that may either limit or expand the options that they can present me with as a result.

Also, it is important to understand how this person will be compensated for their work and how that incentive structure may in turn affect the advice you receive, how reliable you feel that it is, and with what confidence you can assure others in your organization that you have achieved the optimum result.

Additionally, in the process of selecting a broker, employee benefits advisor, or consultant to work with, you may find it advisable to search among professionals in those fields who operate locally and/or who specialize in your industry if there are industry-specific factors that may require special consideration.

In fact, you may wish to contact such a professional to help determine if there are industry-specific considerations that you may be able to benefit from and to which you are otherwise currently unaware.

You may even want to contact the brokers, consultants, and/or employee benefits advisors who have been working with those tiresome competitors who keep poaching your talent – or perhaps you’d be better served by contacting the advisors and brokers of the competitor with such thoughtful and comprehensive benefits packages that their employees can’t seem to be poached.

Find the Right Insurance Broker Today

Luckily, searching for the right broker, consultant, or employee benefits advisor to best serve the needs of your organization is easier than ever before through harnessing the power of public databases. Not only can you refine your search by a variety of different criteria, you will also have access to an algorithmically compiled rating system, thereby ensuring that the professional you choose to work with is verifiably capable of meeting your needs.

With such powerful tools at your disposal - despite that the employer health insurance and benefit plan market may seem murkier than ever - finding the perfect broker, consultant, or employer benefits advisor to suit your organization’s needs requires little more than a few clicks to get the process started.

Mployer Advisor helps employers find top-rated insurance brokers, advisors, and consultants. Our listing database also showcases customer reviews and feedback to help you compare and evaluate different brokers. Start your search today.

How an employer funds its health plan sits quietly in the background of every benefits decision. Most CHROs and CFOs know their premium cost. Fewer understand the mechanics of how their plan is actually structured: who holds the risk, who administers the claims, how costs flow, and what flexibility, if any, they have to change any of it.

Author:

Understanding How Your Health Plan Is Funded Matters More Than Most Employers Think

How an employer funds its health plan sits quietly in the background of every benefits decision. Most CHROs and CFOs know their premium cost. Fewer understand the mechanics of how their plan is actually structured: who holds the risk, who administers the claims, how costs flow, and what flexibility, if any, they have to change any of it.

This post is not an argument for any particular funding model. It is an explanation of how each one works, what the national data shows about adoption by employer size, the key terms you need to understand, and the questions worth asking at your next renewal, whether you are fully insured today and want to stay that way, or whether you want to understand what moving to a different model would actually involve.

One important framing note upfront: funding model decisions are not one-size-fits-all. Fully insured arrangements are the right choice for a significant portion of employers, particularly smaller organizations, because the risk transfer and administrative simplicity is genuinely valuable. The goal here is clarity, not a prescription.

The Three Funding Models: What They Actually Mean

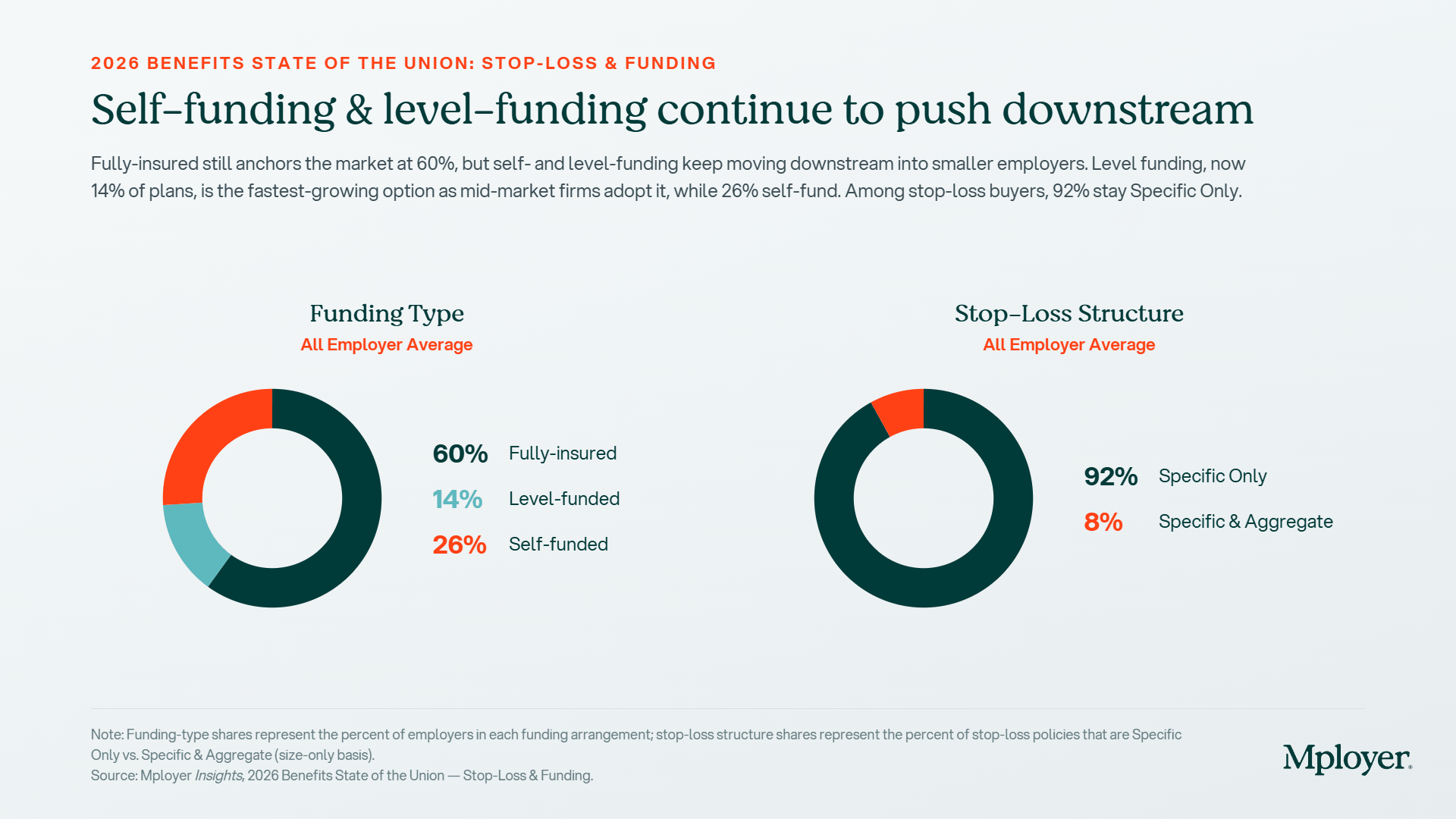

Nationally, 60% of employers are fully insured, 14% are level-funded, and 26% are self-funded, according to Mployer’s 2026 plan data covering 50,000+ employers. But those percentages look very different when you break them out by employer size. Among employers with fewer than 50 employees, fully insured is nearly universal while level-funded and self-funded require a minimum threshold of covered lives to be actuarially viable. The self-funded number rises sharply as employer size grows: roughly 27% of firms with 100–199 employees self-insure, compared to over 90% of firms with 5,000+ employees (DOL).

Fully Insured

The employer pays a fixed monthly premium to a carrier. The carrier assumes all financial risk for claims, manages the network, processes claims, and handles member services. The employer knows their cost in advance, there are no surprises if utilization spikes, but there is also no upside if the workforce has a healthy year. Premium increases at renewal are driven by the carrier’s projections, not the employer’s actual claims experience.

Per Member Per Month (PMPM) costs under fully insured arrangements include the carrier’s built-in risk margin and profit load, typically estimated at 10–15% of premium above what actual claims would cost. For a 200-person employer paying $700 PMPM in premium, that margin can represent $140,000–$210,000 per year in cost that never returns to the employer regardless of utilization. Fully insured is the right choice when an employer values predictability and simplicity above all else, or when their workforce is too small to absorb claims risk directly.

Level-Funded

Level-funded plans are the middle ground that has expanded significantly in the past decade, particularly for mid-size employers. The employer pays a fixed monthly amount, similar to a fully insured premium, but that payment is split into three components: a claims fund (to pay expected claims), a stop-loss premium (to cover catastrophic claims above a threshold), and an administrative fee. If actual claims come in below the funded level, the employer receives a refund of the surplus at year-end.

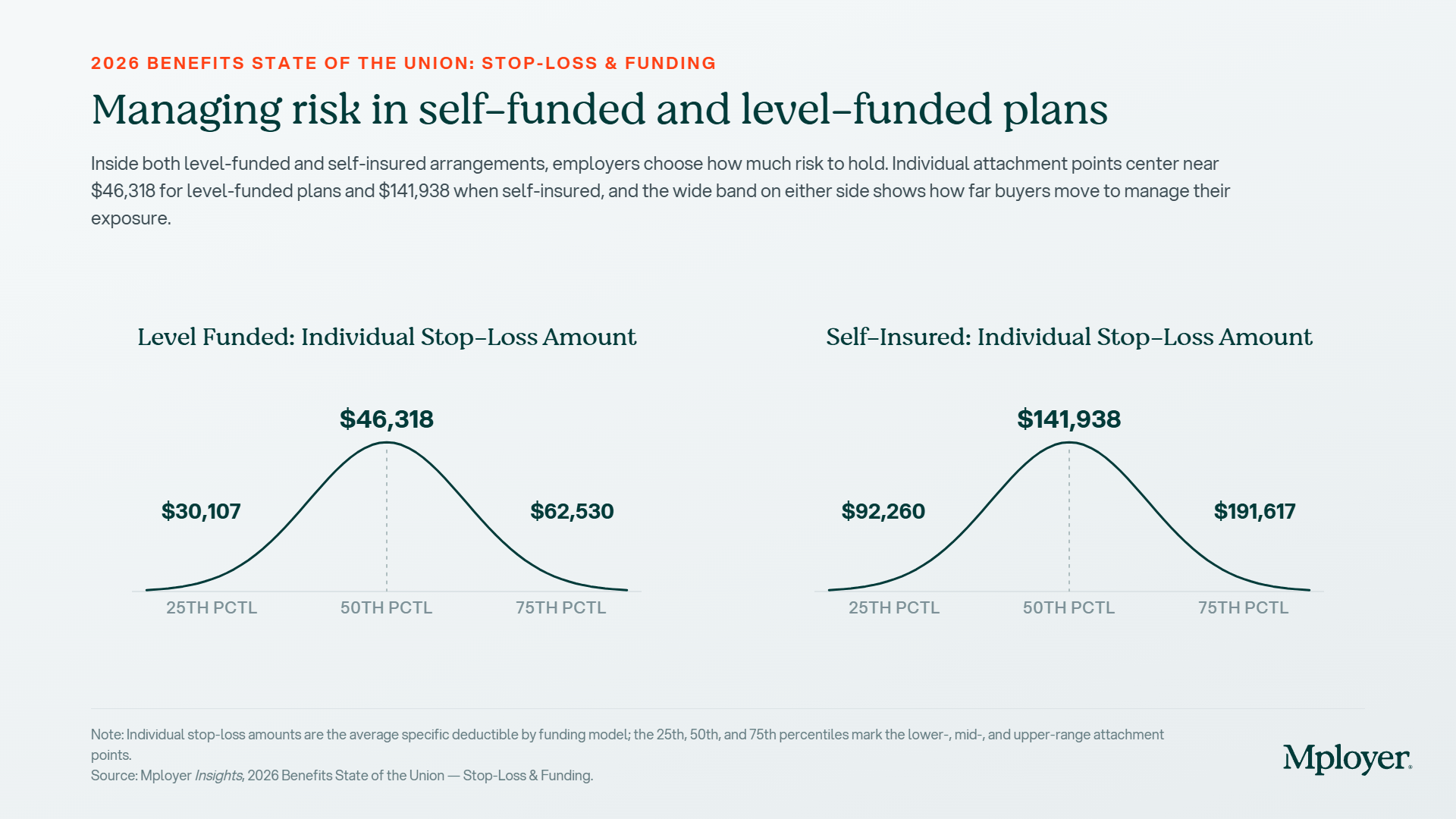

The average individual stop-loss deductible for level-funded plans is $46,318, meaning the employer’s claims fund absorbs the first $46,318 of any individual’s claims before stop-loss coverage kicks in. Level-funded plans give employers their first look at actual claims data, something a fully insured employer never sees, which is often the most valuable outcome of making the switch, independent of any refund.

Self-Funded (Self-Insured)

In a self-funded arrangement, the employer pays claims directly as they are incurred rather than paying a fixed premium. A third-party administrator (TPA) or carrier handles plan administration (network access, claims processing, member services),while the employer retains the financial risk. Stop-loss insurance caps the employer’s exposure on catastrophic individual claims and, optionally, on aggregate plan-wide costs.

The average individual stop-loss deductible for self-insured plans is $141,938, three times the level-funded equivalent, reflecting the higher risk tolerance required to make self-funding economically viable. PMPM costs in self-funded plans are highly variable month to month because costs track actual claims rather than a fixed premium. In a good year, a self-funded employer pays less than they would have under a fully insured arrangement. In a bad year, one with high utilization or a catastrophic claim, stop-loss coverage is what prevents the plan from becoming a financial crisis.

Key Terms Every CHRO and CFO Should Know

Benefits funding conversations move quickly into jargon. These are the terms that matter most:

PMPM (Per Member Per Month): The standard unit for measuring health plan costs. Total annual plan cost divided by total member months. Used to compare costs across plans, funding structures, and years. A fully insured employer often doesn’t know their PMPM, a self-funded employer tracks it monthly.

Stop-Loss Insurance: Insurance purchased by self-funded and level-funded employers to cap their claims exposure. Specific stop-loss covers individual catastrophic claims above a deductible. Aggregate stop-loss covers total plan costs that exceed a set percentage of expected claims (typically 120–125%). Nationally, 92% of self-funded employers carry specific-only stop-loss; 8% carry both specific and aggregate.

Specific Stop-Loss Deductible: The per-person threshold above which the stop-loss carrier begins reimbursing claims. Level-funded average: $46,318. Self-insured average: $141,938. Setting this number too high exposes the employer to more risk per claim; too low raises the stop-loss premium.

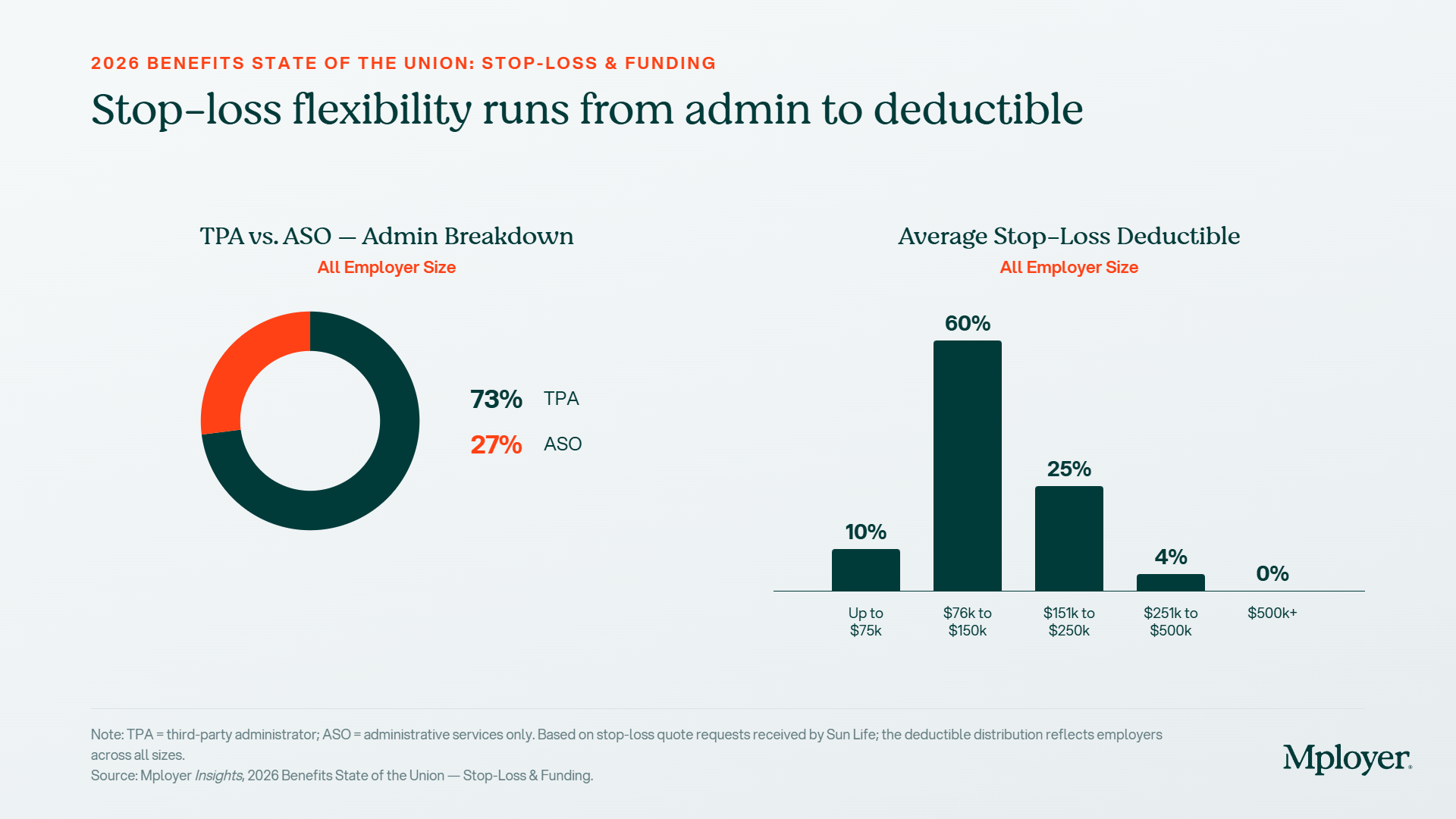

TPA (Third-Party Administrator): An independent organization that administers a self-funded plan, processing claims, managing networks, and handling compliance. 73% of self-funded employers use a TPA. TPAs are carrier-agnostic and give employers more flexibility in how they assemble their plan.

ASO (Administrative Services Only): An arrangement where a major carrier (UnitedHealthcare, Aetna, Cigna, BCBS) administers the plan while the employer retains financial risk. 27% of self-funded employers use ASO. Provides access to the carrier’s national network and integrated services.

Run-Out Claims: Claims incurred before a plan year ends but submitted after. A critical concept when switching funding structures, an employer moving from fully insured to self-funded must account for run-out liability from the prior plan year.

Lasering: A stop-loss carrier practice of excluding a specific high-cost individual from coverage, or charging a higher deductible for them, at renewal. Common for known catastrophic claimants. Employers should understand their stop-loss carrier’s lasering policy before selecting a deductible.

Aggregate Risk Corridor: The band above expected claims before aggregate stop-loss kicks in, typically 120–125% of projected costs. An employer with $10M in expected claims and a 1.22 corridor absorbs the first $12.2M before aggregate coverage begins.

Plan Administration: TPA vs. ASO and How Vendors Fit Together

One of the most underappreciated aspects of moving to a self-funded model is that it separates plan administration from plan financing. Under a fully insured arrangement, the carrier does both. Under a self-funded arrangement, the employer can assemble a best-of-breed stack: choosing a TPA for administration, a separate stop-loss carrier for risk protection, a PBM for pharmacy, and a network rental arrangement for provider access. That modularity is both the primary advantage and the primary complexity of self-funding.

Third-Party Administrators (TPAs)

TPAs administer the day-to-day operations of a self-funded plan without carrying any of the insurance risk. They process claims, manage member ID cards, handle appeals, provide reporting, and ensure compliance. Because they are carrier-agnostic, employers using a TPA can select their network, stop-loss carrier, and PBM independently. Key TPA vendors in the market include:

Imagine360 — self-funded and reference-based pricing specialist; strong mid-market focus

Allied Administrators — independent TPA with regional strength and flexible plan design

Trustmark — TPA with integrated level-funded and self-funded products

Benefit Administration Company (BAC) — mid-market TPA with stop-loss relationships

Sun Life — major stop-loss carrier that also provides TPA services and data analytics

Administrative Services Only (ASO) Carriers

Under an ASO arrangement, the employer accesses a major carrier’s infrastructure — their provider network, claims processing systems, and member services, while self-funding the actual claims. The primary advantage is network breadth: UnitedHealthcare, Aetna, Cigna, and the Blue Cross Blue Shield plans have national networks that most TPAs cannot replicate. The tradeoff is less plan design flexibility and, typically, less direct access to claims data. ASO is the most common path for large employers who want the benefits of self-funding without building an entirely independent plan infrastructure.

Carving Out Vendors: Where Employers Have the Most Leverage

One of the most powerful moves available to self-funded and level-funded employers is selectively replacing the default vendor stack with purpose-built alternatives. The most common carve-outs:

PBM Carve-Out: Most ASO carriers bundle their own PBM (UHC uses OptumRx, Aetna uses CVS Caremark, Cigna uses Express Scripts). Employers can carve out the PBM and contract directly with an independent pharmacy benefit manager, often achieving better rebate pass-through and lower net drug costs. Employers with 500+ covered lives typically have the leverage to negotiate meaningfully. Independent PBMs like Capital Rx, Navitus, and SmithRx are built specifically for transparent, pass-through pricing models.

Specialty Pharmacy Carve-Out: Specialty drug spend (oncology, biologics, GLP-1s) is the fastest-growing cost component in most plans. Carving specialty pharmacy to a dedicated specialty PBM or white-bagging program, where drugs are dispensed through the employer’s preferred channel rather than a hospital pharmacy, can generate material savings on a small number of high-cost claimants.

Centers of Excellence (COE) Carve-Out: For high-cost procedures like joint replacement, cardiac surgery, bariatric surgery, and oncology treatment, employers can steer members to designated high-quality, lower-cost providers. COE programs through vendors like Included Health, Transcarent, and the major carrier networks have demonstrated both quality improvements and cost reductions for self-funded employers.

Mental Health / EAP Carve-Out: Traditional EAPs have low utilization and limited clinical depth. A growing number of self-funded employers are carving out behavioral health to dedicated platforms (i.e. Lyra Health, Spring Health, Headspace Health) that offer broader access and measurable utilization outcomes.

Stop-Loss Carve-Out: ASO carriers often offer stop-loss as part of their package. Self-funded employers can go to market independently with stop-loss carriers (i.e. Sun Life, Tokio Marine HCC, Voya, Symetra) to find better rates, higher deductibles, or more favorable lasering terms.

Each carve-out adds administrative complexity and requires coordination between vendors. The benefit of a TPA is that it can serve as the integrating layer, managing data feeds, eligibility, and claims adjudication across a multi-vendor stack. For employers considering their first carve-out, the PBM is usually where the most immediate financial opportunity exists.

High-Cost Claimants and What the Stop-Loss Data Shows

For any self-funded or level-funded employer, understanding high-cost claimant dynamics is essential. A single member with a catastrophic diagnosis, a premature birth requiring NICU care, an oncology case requiring immunotherapy, or a rare disease requiring gene therapy, can represent more claims cost than dozens of average members combined.

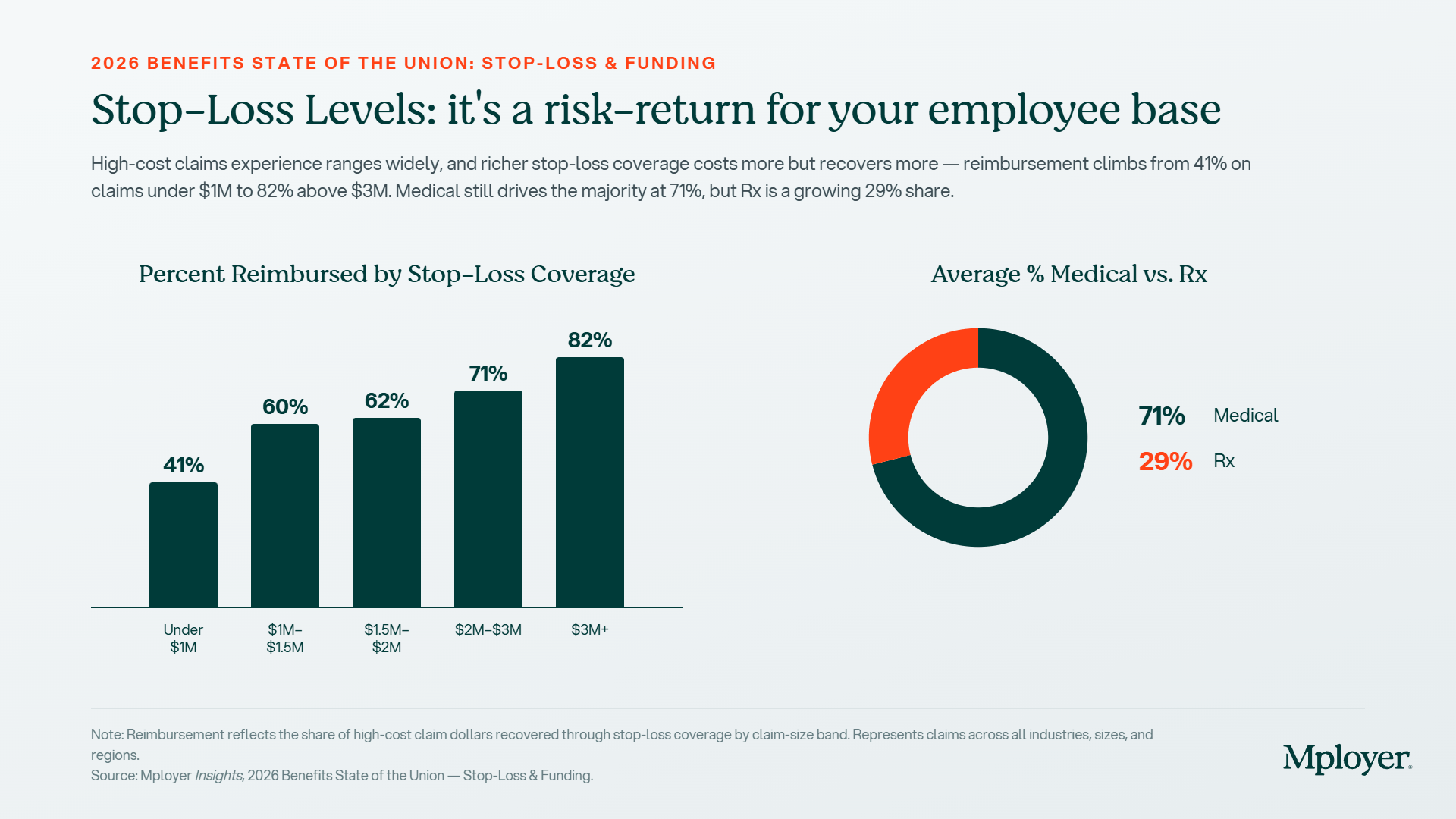

The stop-loss reimbursement data illustrates how the financial burden of large claims is distributed between employers and their stop-loss carriers:

Claims under $1M: 41% reimbursed by stop-loss, employers absorb the majority

Claims $1M–1.5M: 60% reimbursed, stop-loss begins to shoulder more

Claims $1.5M–2M: 62% reimbursed

Claims $2M–3M: 71% reimbursed

Claims over $3M: 82% reimbursed, stop-loss is covering the vast majority

The practical implication: stop-loss coverage is most valuable at the extremes. Below $1M in total claims, the employer is absorbing nearly 60 cents of every dollar. Above $3M, the stop-loss carrier is covering 82%. Setting the right specific stop-loss deductible is therefore a meaningful financial decision, higher deductibles reduce stop-loss premiums but increase the employer’s per-incident exposure.

The composition of those high-cost claims matters too. Nationally, 71% of high-cost claim dollars are medical and 29% are pharmacy. That pharmacy share is rising. Specialty drugs, like particularly oncology therapies, biologics, and increasingly GLP-1 medications, are driving the Rx portion higher year over year. For self-funded employers, a specialty drug claim for a single member can now approach or exceed the average $141,938 stop-loss deductible in a single plan year. This is why formulary design, specialty pharmacy strategy, and stop-loss adequacy are increasingly interconnected decisions rather than separate ones.

What to Consider If You Are Fully Insured and Want to Understand Your Options

Moving from fully insured to level-funded or self-funded is not a decision to make lightly. It requires the employer, their CFO, their CHRO, and their broker or consultant to answer a set of questions honestly before modeling the economics:

Size: Do you have enough covered lives to make the model actuarially viable? Level-funded is generally accessible at 25–50+ lives. True self-funding typically requires 100+ covered lives to carry meaningful claims risk, and 200+ before the economics are compelling without level-funded guardrails.

Cash flow: Can your organization absorb monthly claims variance? Self-funded plans pay claims as incurred; a bad month is a real cash event, not just a future premium increase. Stop-loss reimbursement typically runs 30–90 days after the claim is paid, creating a temporary cash flow gap.

Risk tolerance: Is your leadership prepared for year-to-year cost variability? Self-funding can produce meaningful savings in good years and meaningful overruns in bad ones. The multi-year economics almost always favor self-funding at sufficient scale, but the path is not smooth.

Administrative capacity: Self-funded plans require more active management, including stop-loss renewals, TPA oversight, claims audits, and compliance filings. Your broker or consultant needs to have genuine self-funded expertise, not just familiarity with the concept.

Data readiness: The primary non-financial benefit of self-funding is access to your own claims data. Are you prepared to actually use that data to make plan design decisions? Employers who self-fund without using their claims data are paying for a capability they’re not capturing.

Run-out liability: When leaving a fully insured arrangement, the employer is responsible for claims incurred during the fully insured period but submitted afterward. This run-out must be accounted for in the financial model, it is often the surprise that derails first-year self-funded economics for employers who didn’t plan for it.

If the answers to these questions are uncertain, level-funded is almost always the right first step. It provides the refund upside and data transparency of self-funding with the fixed monthly cost and administrative simplicity of fully insured. For many employers in the 50–250 life range, level-funded is not a stepping stone, it is the right permanent answer.

The Point Is Not Which Model; It’s Whether You Know What You’re In

The most important outcome of understanding plan funding is not deciding to switch models. It is being able to have an informed conversation with your broker, your CFO, and your board about what you’re paying, what you’re getting, and what the alternatives look like.

An employer who has been fully insured for ten years and has never modeled a level-funded alternative does not know what that decision is costing them. An employer who is self-funded but has never analyzed their claims data does not know what that structure is worth. In both cases, the answer starts with a benchmark, knowing where your plan sits relative to employers who actually look like you.

Mployer’s benefits rating evaluates plan funding structure, stop-loss levels, and PMPM costs as part of the Medical pillar score, so employers can see not just what they’re paying, but how that compares to their custom cohort.

.svg)

.jpg)

.svg)

.svg)

.svg)

.svg)