.svg)

Product Updates

Product Updates, August 2026

Welcome to our latest release. We are excited for you to try the new features.

July 31, 2026

August Release Notes: Catalyst and Insights

Welcome to our latest release. We are excited for you to try the new features. This release focused on four things: making Mployer AI available throughout every product, rebuilding each product's home page to put the AI assistant front and center, adding new filters in Catalyst to help you find more opportunities, and opening free tiers on all products. Below is a summary of the major changes.

Mployer AI throughout Catalyst

The Mployer AI panel is now available on every Catalyst search grid: Employer, Commercial P&C, Broker, Carrier, Company, PEO, and Retirement. You can ask questions about your results without leaving the search.

The home page search bar has been replaced with the same AI chat. You can ask about companies, OSHA data, or benefits in plain language from the top of the page, and your chat history is retained on your device.

All AI surfaces in Catalyst, including the in-app chatbot and home page search, now run on an updated MCP backend, making every assistant significantly smarter.

Commercial Search

Experience Mod, carrier relationship, modeled payroll, and premium are now available as filters and columns in Commercial Search. OSHA and DOT records show violation gravity, the number of employees exposed, and 12-month trend direction across violations, crashes, and drivers. P&C brokers can now build prospect lists around financial exposure and compliance risk directly in the grid.

PEO Search

PEO Search, Snapshot, and Company Snapshot now show a single view of an employer's most recent PEO affiliation, with full switching history available from the same place. Previously, multiple affiliations could appear as separate records. Filters, columns, and exports now include Filing Source, PEO status, Benefits and Overall Rating, Most Recent Filing, EIN, and NAICS, bringing PEO Search in line with Employer Search.

Export and contact visibility

The export modal now shows your remaining credit balance and the actual record count and cost after exclusions, before you confirm. The "Exclude Previously Exported" option now covers the past 12 months rather than your full export history.

Contact records display an email verification status at all times, and you can filter contacts by that status when prioritizing outreach.

Mployer AI on the Insights home page

You can now ask questions about your book of business directly from the Insights home page. An AI assistant sits alongside your submissions and works against your client data, so you can ask which clients scored below benchmark, which reports are complete, which clients qualify for an award, or "show me completed reports where voluntary STD is offered," and get the answer without building filters by hand.

You can filter submissions by benchmark score, lifecycle state, and award eligibility, run reports from the same view, and export any filtered result to CSV.

Free tiers on all products

Every product now includes a free tier. We encourage you to try out all the resources now available to you.

AI panel on Insights+ reports

The Mployer AI panel on Insights+ HTML reports has been redesigned to match the AI panels in the rest of the platform, with the same layout, controls, and prompt patterns. Generate recommendations and ask any questions about the report and data, and get answers instantly.

Help Center

A new Help Center is live, with a home page, per-product detail pages, and a video tutorial library. Webinars, product updates, a glossary, and FAQs will be added within the same structure.

If you have questions about any of these changes, contact Partner Success or reach us through the Help Center.

The Likely Fastest-Growing Line in Your Benefits Budget

Modern medicine has produced remarkable advances. Cancer therapies that were not available five years ago are now extending and saving lives. Treatments for autoimmune diseases, multiple sclerosis, and rare genetic conditions are giving employees and their families real options where few existed before. As an employer, providing access to these treatments through your benefit plan is one of the most meaningful things your organization does for the people who work there.

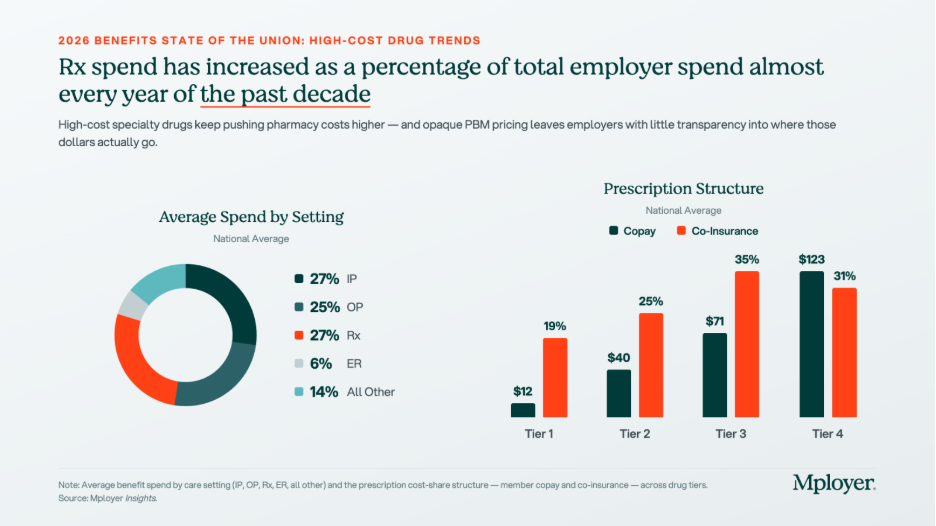

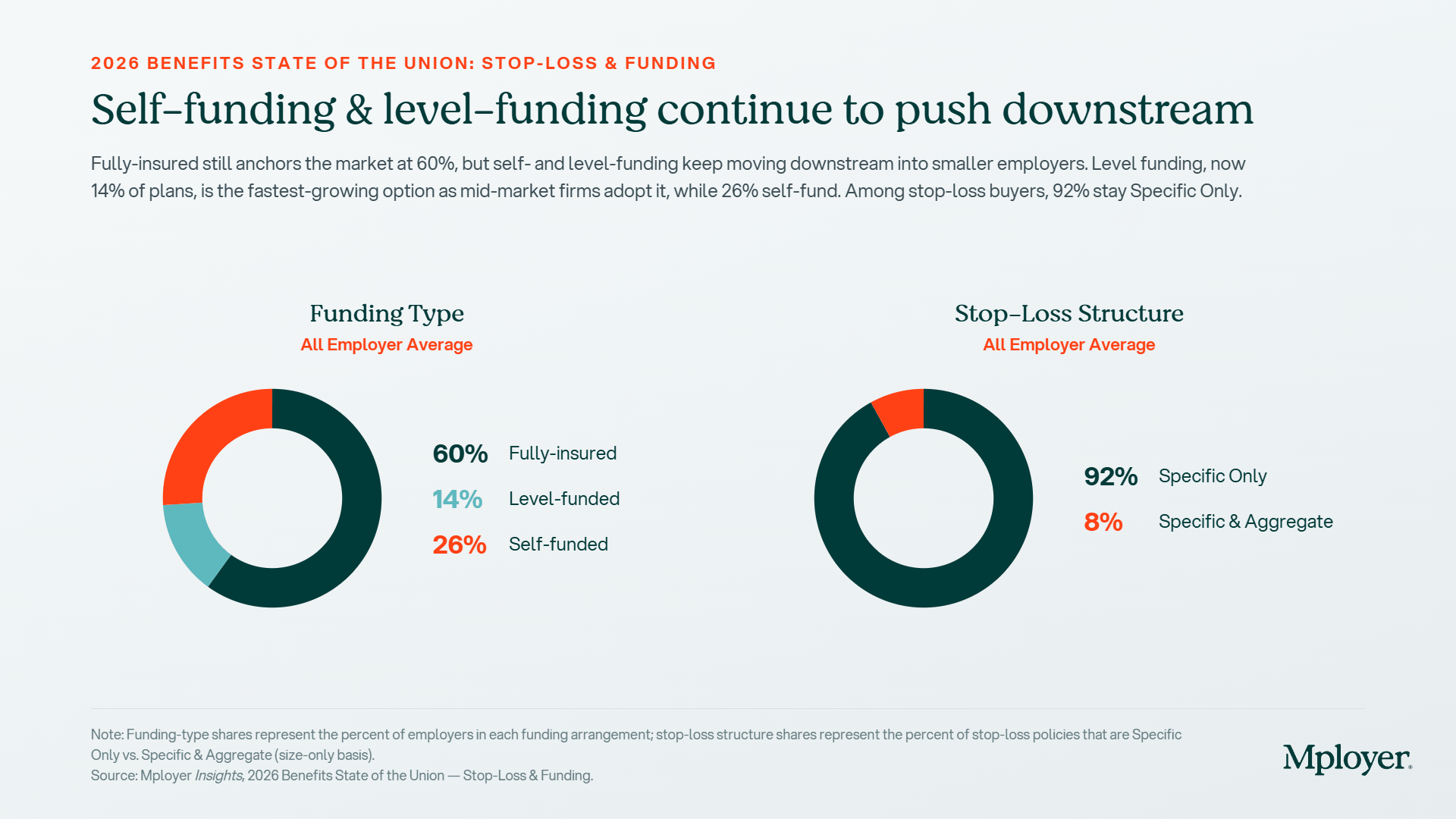

It also comes with a financial reality that every benefits decision maker needs to understand clearly. Over 25% of total employer health benefit expenses are now driven by prescription drugs, and within that figure, a small number of specialty drugs account for an outsized share of the cost. A single covered employee on an oncology therapy can generate $100,000 to $170,000 or more in annual drug spend. A handful of members on these treatments can represent a larger budget impact than the entire pharmacy spend of the rest of your workforce combined. The goal is not to restrict access to these medications. The goal is to understand how the system works, how costs flow, and how to structure your plan so that both your employees and your organization are best positioned for the long term.

This piece covers how the pharmacy benefit system works, how your plan’s tier structure determines who pays what, how stop-loss insurance interacts with high-cost drug claims, and what employers can do to manage this exposure thoughtfully.

The tier structure in the chart above reflects how plans already account for the cost complexity of specialty drugs. Tier 4, which is where specialty biologics and injectables are typically placed, carries significantly higher cost-sharing than the other tiers: an average employee copay of $123 and coinsurance requirements in 31% of plans. But Tier 4 behaves very differently from the other tiers. On Tier 1, 2, and 3 drugs, cost-sharing is relatively predictable and manageable. On Tier 4, the combination of high drug cost and percentage-based coinsurance can generate out-of-pocket exposure that approaches or exceeds a patient’s annual out-of-pocket maximum in a single month of therapy. How Tier 4 is structured, what controls are in place, and how the plan manages cost is one of the most consequential design decisions an employer makes.

Understanding Your Benefit Plan’s Pharmacy Options

How Pharmacy Benefit Managers Work

Most employer health plans do not manage pharmacy benefits directly. That function is delegated to a Pharmacy Benefit Manager, or PBM, which acts as the intermediary between the health plan, the pharmacy, and the drug manufacturer. The PBM builds and maintains the formulary, negotiates drug prices and rebates with manufacturers, contracts with pharmacy networks, and processes pharmacy claims. The three dominant PBMs, Express Scripts (owned by Cigna), CVS Caremark (owned by CVS Health / Aetna), and OptumRx (owned by UnitedHealth Group), together manage the pharmacy benefits of approximately 80% of covered lives in the United States. Each is affiliated with a major carrier, meaning that employers who use an ASO medical arrangement often default to the carrier’s affiliated PBM without realizing it. Independent PBMs such as Capital Rx, Navitus, and MedOne Pharmacy Benefit Solutions operate on transparent, pass-through pricing models that return all rebates to the plan rather than retaining them as PBM revenue. PBMs are compensated through administrative fees, spread pricing (charging the plan more than the pharmacy receives and keeping the difference), manufacturer rebates in exchange for formulary placement, and specialty pharmacy margin. For any employer managing meaningful specialty drug spend, understanding which of these revenue sources applies to your contract is essential.

How Drug Tiers and Cost-Sharing Work

Every pharmacy benefit plan organizes covered drugs into tiers, with cost-sharing that increases as you move from Tier 1 generics (avg. $12 copay) through Tier 2 preferred brands ($40), Tier 3 non-preferred brands ($71), and into Tier 4 specialty drugs ($123 copay, with coinsurance in 31% of plans). The tier placement of a drug affects both what the employee pays and, indirectly, what the plan pays, since tier placement drives utilization patterns. Plan sponsors have real levers here: step therapy (requiring a patient to try a lower-cost drug first), prior authorization, specialty pharmacy channel mandates, and formulary exclusions all affect Tier 4 cost without eliminating clinical access. These controls require balancing cost management with the reality that for many specialty drugs, no lower-cost alternative achieves the same clinical outcome.

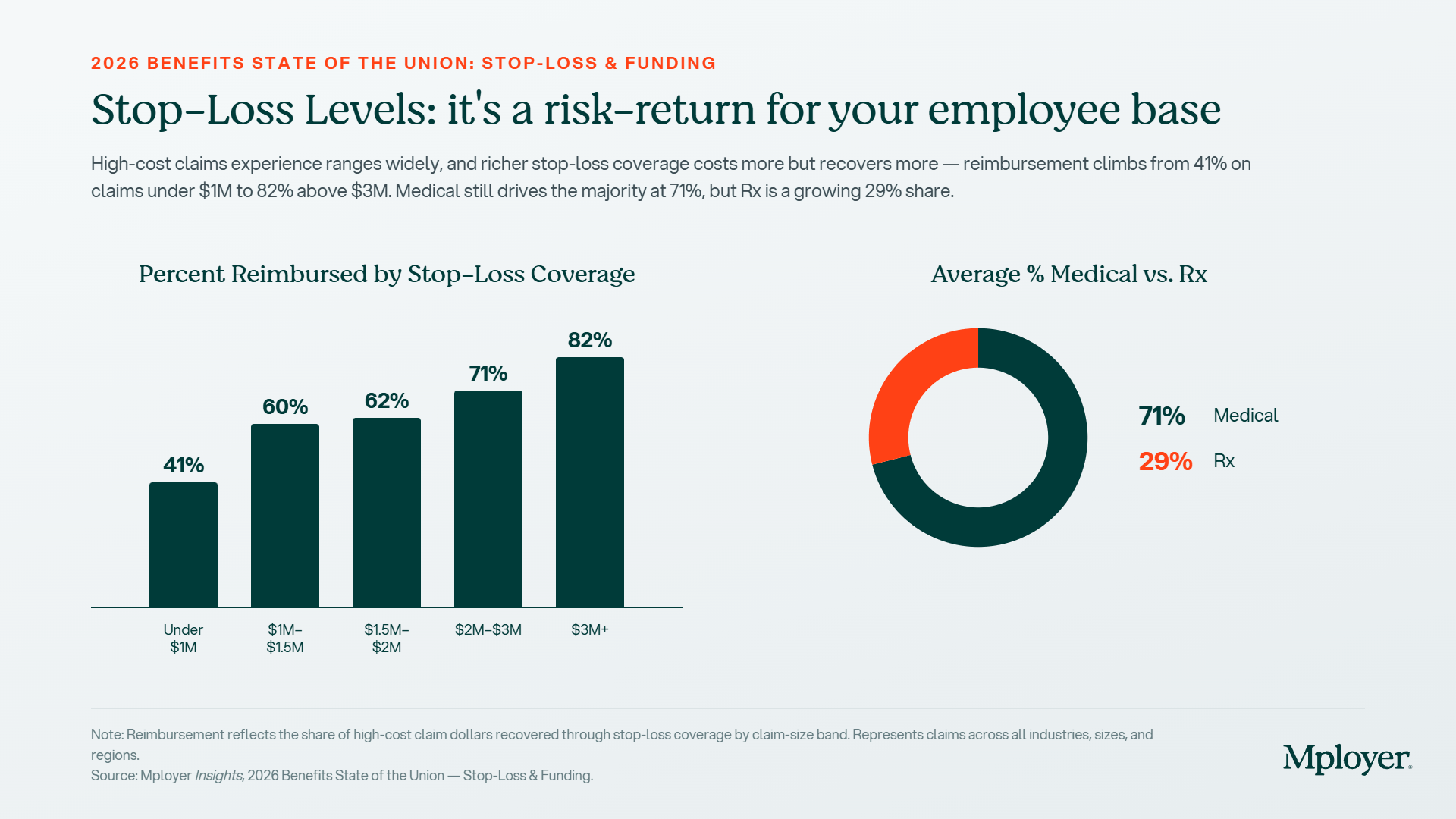

How Stop-Loss Insurance Interacts with High-Cost Drug Claims

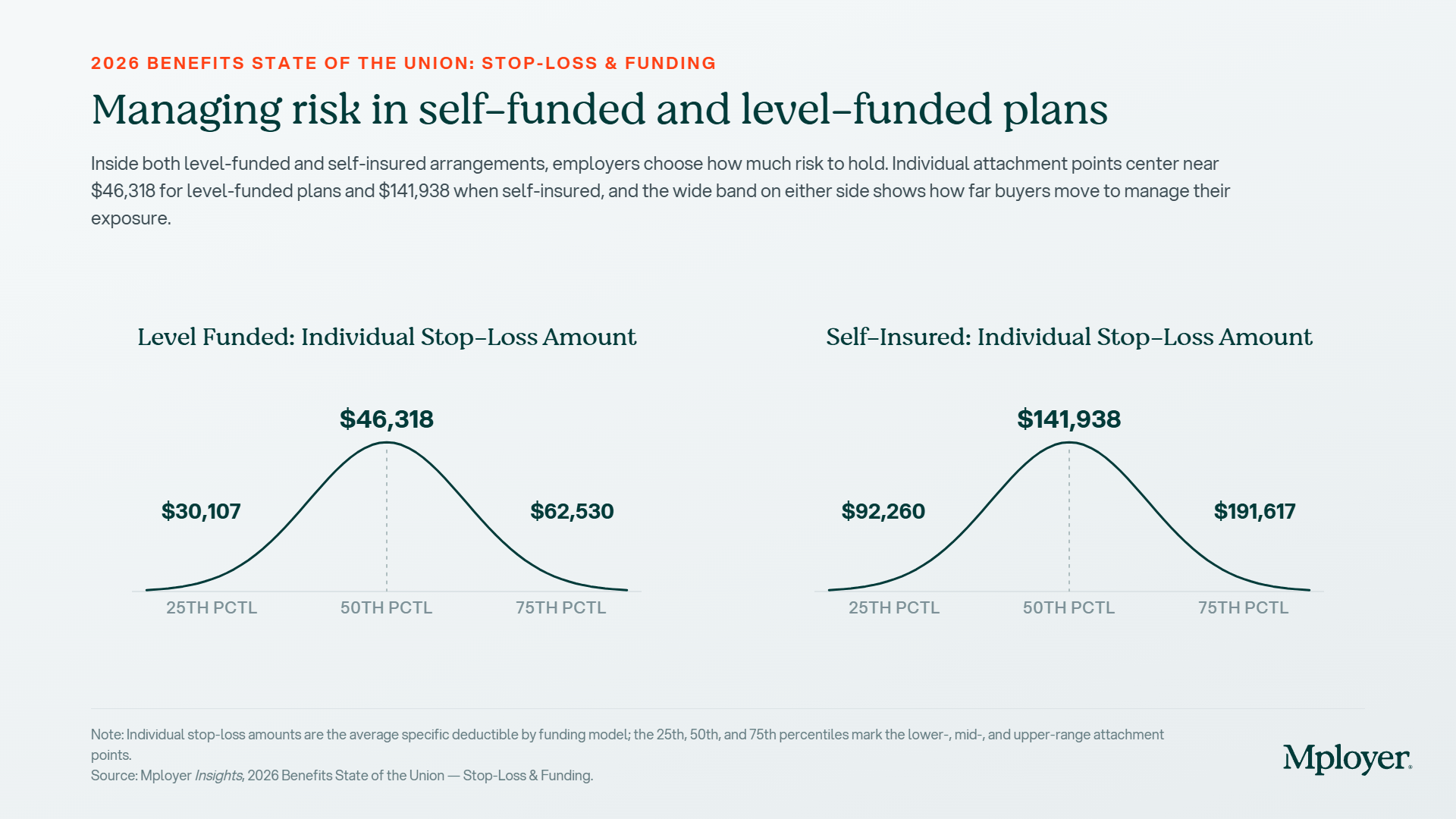

For self-funded employers, specialty drug claims are now among the most common triggers for individual stop-loss reimbursement. A single employee on a cancer therapy or rare disease treatment can generate pharmacy claims that exceed the plan’s specific stop-loss deductible, which averages $141,938 nationally for self-insured plans, within a single plan year. The mechanics: the employer pays all claims up to the deductible threshold, and the stop-loss carrier reimburses costs above it. Several dynamics are specific to high-cost drugs. At renewal, stop-loss carriers may laser a known high-cost member by raising their individual deductible or excluding them from coverage. Some carriers now specifically carve out GLP-1 medications or other high-utilization drug categories from stop-loss reimbursement, so employers adding new drug coverage should verify what their contract covers. Specialty drugs can also be administered under either the pharmacy benefit or the medical benefit depending on whether they are self-administered or clinic-administered, and some stop-loss contracts apply different terms to each channel. Employers should model their actual specialty drug cost distribution against their stop-loss deductible at every renewal to understand where the plan’s real exposure sits.

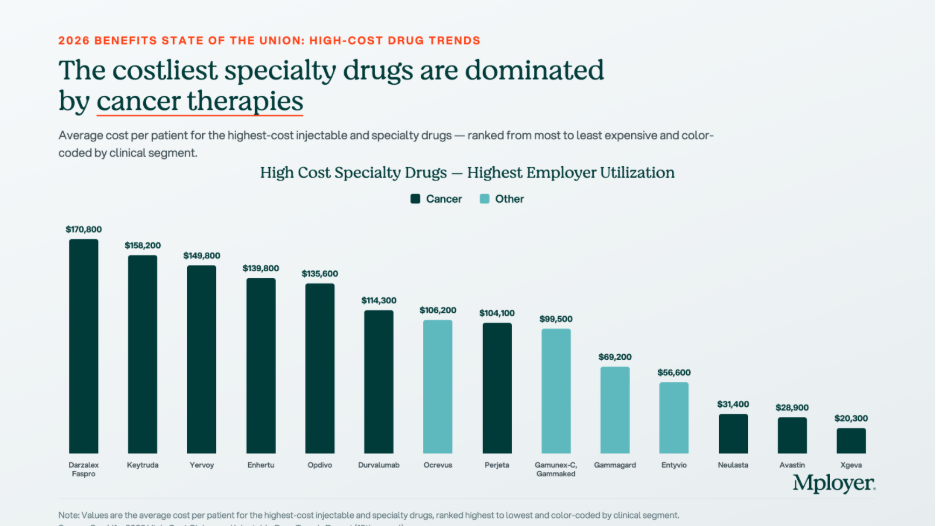

The Costliest Specialty Drugs: What They Treat and What They Cost

The chart below shows the highest-cost specialty and biologic drugs by average cost per patient, ranked from most to least expensive. Cancer therapies dominate the top of the list, but treatments for autoimmune conditions, MS, and inflammatory disease also appear, reflecting how broadly specialty drug spending is distributed across a workforce.

Biosimilars: The Cost Opportunity Most Employers Are Not Fully Using

A biosimilar is a biologic drug that is highly similar to an already-approved reference biologic, with no clinically meaningful differences in safety, purity, or potency. Biosimilars are not generic drugs in the traditional sense, because biologic drugs are complex proteins manufactured from living cells and cannot be chemically replicated exactly. But they go through an FDA approval pathway that confirms their clinical equivalence to the reference product, and they cost significantly less. The biosimilar market has expanded rapidly as major biologic patents have expired. Humira, the world’s best-selling drug for much of the past decade, now has multiple biosimilar competitors in the U.S. Stelara has followed. The oncology biosimilar pipeline is maturing, with more approvals expected in the next two to three years.

The chart above shows what biosimilar substitution looks like in dollar terms. For Humira, the net price after rebates and negotiated discounts is $2,370 per box. The biosimilar Yusimry has an estimated net price of $635, a 73% reduction. For Stelara, the reference drug net price is $7,636 per box. The biosimilar Starjemza has an estimated net price of $4,010, a 47% reduction. For an employee on monthly Humira therapy, the difference between the reference drug and the biosimilar is approximately $21,000 per year in net plan cost. For a Stelara patient, the annual difference is approximately $43,500. Across even a small number of members on these therapies, biosimilar substitution is one of the highest-return cost management interventions available.

Plan sponsors have four main tools to drive biosimilar adoption: preferred formulary placement (putting the biosimilar on a lower tier and the reference drug on a higher tier), step therapy for new patients, automatic substitution where state law permits, and formulary exclusion of the reference drug entirely. The most important variable in any biosimilar strategy is whether your PBM has a financial incentive to keep the reference drug preferred. A PBM earning a large rebate on Humira has a direct financial reason to keep Humira on the preferred formulary, even when the biosimilar costs the plan less on a net basis. Independent PBMs operating on pass-through pricing remove this conflict entirely, because all rebates return to the plan and formulary decisions are made without a competing financial interest.

What Employers Should Be Asking About Their Pharmacy Benefit

High-cost drug management requires active decisions about PBM contract structure, formulary design, specialty pharmacy strategy, and stop-loss alignment. The questions worth asking at every renewal:

Know How Your Pharmacy Benefit Compares

Pharmacy is now one of the two or three most consequential cost management decisions in health plan design. The employers managing it well are not restricting access to the medications their employees need. They are ensuring that the structure of the benefit, the PBM contract, the formulary design, and the stop-loss coverage work together in the plan’s interest, and that every dollar spent on high-cost drugs is spent as efficiently as possible.

Mployer’s benefits rating evaluates pharmacy benefit design as part of the Medical pillar score, benchmarked against a custom cohort matched by size, region, and industry. Knowing where your pharmacy benefit stands relative to employers who actually look like you is the starting point for making better decisions.

See how your benefits package compares to your custom cohort at MployerAdvisor.com.

Sources

Mployer Insights: Average Spend by Setting, Prescription Structure, and High-Cost Specialty Drugs. Source: Mployer Insights analysis.

MedOne Pharmacy Benefit Solutions: Biosimilar substitution impact data for Humira/Yusimry and Stelara/Starjemza. MedOne is a leading independent PBM focused on improving health outcomes and reducing net costs for self-funded employers. [email protected].

Mployer 2025 and 2026 Employee Benefit Plan Design Study, covering 50,000+ employer plans. Individual stop-loss avg $141,938 self-insured.

Consolidated Appropriations Act of 2021, Section 202: broker/consultant compensation disclosure requirements for group health plans.

FDA Biosimilar approval framework: 42 U.S.C. Section 262(k).

Parental and Maternity Leave: What Employers Need to Know

If there is one area of employee benefits where employer decisions signal values as loudly as economics, it is parental leave. How an organization treats employees who are growing a family, both during the leave itself and in how it structures the financial support, tells candidates and employees a great deal about whether the organization means what it says about supporting its people.

This is Part 2 of our leave benefits series. Part 1 covered the foundations: vacation, paid holidays, sick leave, consolidated vs. non-consolidated plans, workplace flexibility, and the federal and state legal framework. This post goes deeper on maternity and parental leave specifically: what the terms mean, how the programs are structured, what federal and state law requires vs. what employers choose to provide, and how the data from 50,000+ employer plans describes the current state of the market.

The data in this post is at the national all-employer average. The variation beneath that headline, by industry, employer size, and region, is significant. A technology employer in a major metro area competing for mid-career talent faces a very different parental leave benchmark than a regional manufacturer or a healthcare employer in a mid-size market. Both contexts are worth knowing. The national benchmarks in this post show where the floor and the ceiling are. Knowing where your specific cohort sits requires a custom comparison.

Key Terms Every Benefits Decision Maker Should Know

What the Law Requires: Federal and State Baseline

Federal FMLA

Federal FMLA, covered in depth in Part 1, provides the baseline: up to 12 weeks of unpaid, job-protected leave for the birth, adoption, or foster placement of a child. This applies to employers with 50 or more employees. The critical word, again, is unpaid. FMLA does not require the employer to pay anything during parental leave. It only requires that the job be protected and that group health insurance continue during the leave period on the same terms as if the employee had not taken leave.

FMLA also applies to both parents, which is a point often overlooked. The non-birth parent, whether an adoptive parent, a same-sex partner, or a non-birth parent of any kind, is entitled to the same 12 weeks of unpaid job protection under federal FMLA as the birth parent, assuming all eligibility requirements are met.

State Paid Family Leave Programs

The paid leave piece, when it exists at state level, comes from state paid family and medical leave programs. These are state-administered insurance programs that pay a wage replacement benefit, typically 60 to 90 percent of the employee’s wage up to a weekly cap, to employees on qualifying parental or family leave. The most established programs are in California, New Jersey, New York, Washington, Massachusetts, Connecticut, Oregon, Colorado, Rhode Island, and the District of Columbia, with additional states phasing in programs in the coming years.

These programs are funded through payroll contributions, typically deducted from employee wages, sometimes matched by employers. The benefit is paid by the state program, not directly by the employer, though the employer is responsible for administering eligibility, managing payroll deductions, and coordinating the state benefit with any employer-provided leave. Employers in states with paid leave programs should understand how the state benefit interacts with their own leave policy, including whether employees are required or permitted to use accrued PTO concurrently with state paid leave.

Pregnancy Discrimination and PUMP Act

Two additional federal laws shape the employer’s obligations around pregnancy and parental leave. The Pregnancy Discrimination Act prohibits employers with 15 or more employees from discriminating against employees on the basis of pregnancy, childbirth, or related conditions. The PUMP for Nursing Mothers Act, enacted in 2022, requires employers to provide reasonable break time and a private space for nursing employees to express breast milk for up to one year after the child’s birth. These are separate from FMLA and apply to a broader range of employers.

Maternity Leave: What the National Data Shows

68% of employers nationally offer dedicated maternity leave beyond statutory short-term disability. 32% do not, meaning those employees rely entirely on STD for any paid income during leave, typically six to eight weeks at whatever percentage the disability plan covers. Among the 68% who do offer dedicated maternity leave, eight weeks of additional paid leave is the most common duration at 31%, with twelve weeks close behind at 26%. Together those two categories account for more than half of all programs. 16% of employers offer thirteen or more weeks of additional paid leave, placing them at the generous end of the market nationally.

Reading this data correctly requires understanding what these weeks represent. The duration bars in the chart show the additional paid leave added on top of disability coverage, not the total leave period. An employee at an employer offering eight weeks of additional leave on top of a six-week STD benefit has fourteen weeks of paid leave total before any unpaid FMLA job protection kicks in. That total is what candidates and employees are actually comparing when they evaluate a parental leave program.

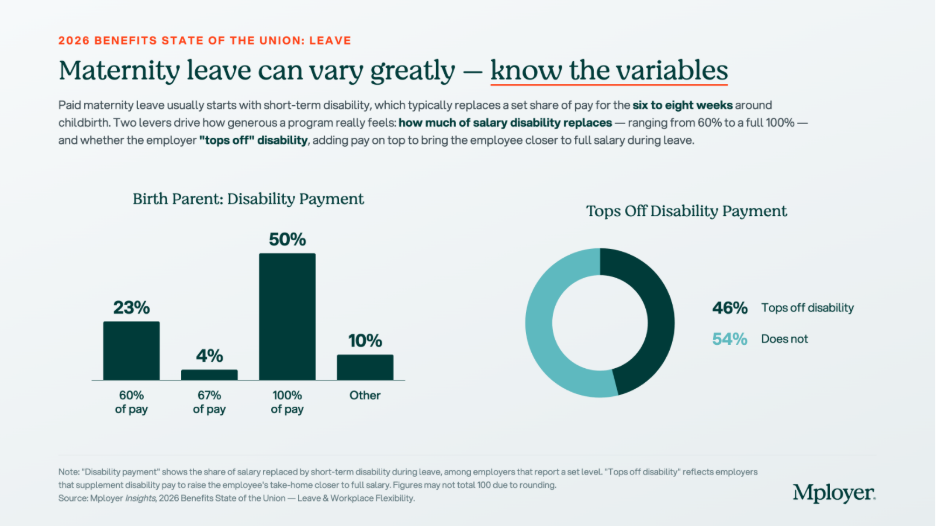

Disability Payment Rates and Top-Off: The Variables That Define Generosity

The chart above tells the real story of how financially supportive maternity leave programs are. On the disability payment rate, the market has split sharply: 50% of employers with a defined disability payment rate pay 100% of salary during the disability period, while 23% pay the traditional 60% of salary. The gap between these two is meaningful. An employee earning $80,000 per year on a six-week disability period at 60% of pay receives approximately $5,538. At 100% of pay, she receives $9,231. That $3,693 difference is real money for a new parent.

The top-off picture is similarly divided. 46% of employers supplement the disability benefit to bring the employee closer to full salary. 54% do not. An employer who pays STD at 60% of salary and does not top off is providing the minimum financial support that a standard disability plan delivers. An employer who pays 100% of salary or who tops off a 60% plan to full pay is making a meaningfully different statement about how much they value employees during one of the most important transitions of their lives

The combination of these two variables, disability payment rate and top-off, is what candidates from competitive talent markets are increasingly asking about directly. It is not enough to say your company offers paid maternity leave. The question they are asking is: how much will I actually receive, and for how long?

Non-Birth Parent Leave: A Growing Expectation, Not Yet a Standard

41% of employers nationally offer dedicated non-birth parent leave, meaning leave specifically provided for partners, fathers, adoptive parents, and same-sex parents who are not the birth parent. 59% do not. Among those who do offer non-birth parent bonding leave, twelve weeks is the most common duration at 32%, with six weeks next at 23%. The 30% in the Other category reflects the wide variation in how these programs are structured, including tiered policies, programs that vary by tenure, and policies that provide different durations based on the type of parental event.

The gap between maternity and non-birth parent leave offer rates, 68% vs. 41%, reflects the historical pattern of parental leave being designed primarily around biological motherhood and disability recovery. That framing is shifting. Candidates across generations, and particularly millennial and Gen Z candidates who are entering or approaching family formation years, are increasingly evaluating parental leave as a package: not just what the birth parent receives, but whether the partner can also be present. An employer offering generous maternity leave but no paternity or bonding leave is offering a program that structurally assumes only one parent takes significant time away, which does not match how many families today want to organize the early months of a child’s life.

Non-birth parent leave also has a practical retention implication. Employees who take bonding leave and feel supported by their employer during it are more likely to return to work and remain engaged. The data on parental leave and retention consistently shows that leave policies affect long-term retention rates, not just initial job acceptance.

Fertility and Adoption Benefits: Rare but Rising

28% of employers nationally offer IVF coverage as part of their medical or family-building plan. 11% offer adoption assistance. Both numbers reflect concentrated adoption among larger employers and in specific geographies and industries, particularly technology, financial services, and professional services employers in major metropolitan markets. Coverage terms, lifetime maximums, and eligibility criteria vary widely among the minority of employers who offer these benefits, making direct comparisons difficult without plan-level detail.

IVF treatment costs can reach $15,000 to $30,000 or more per cycle, with most patients requiring multiple cycles. For employees who need IVF to build a family, employer coverage is not a luxury benefit. It is a financial necessity that directly affects whether they can afford to pursue treatment at all. For employers, IVF coverage is a high-signal benefit: it communicates investment in the full arc of an employee’s family life, not just the period after a child arrives. Among employers competing for talent in industries where IVF coverage has become a common offering, its absence is noticed.

Adoption assistance typically covers qualified adoption expenses such as legal fees, agency fees, home study costs, and travel, up to an annual maximum that varies by employer. The IRS allows employers to provide up to $17,280 in adoption assistance per child tax-free in 2026. Adoption leave policies, separate from adoption assistance, are covered under FMLA for qualifying placements and under many state paid leave programs as well.

Parental Leave as a Talent and Retention Strategy

Parental leave is one of the most emotionally charged benefit decisions a candidate makes. It is also one of the most concrete. Unlike dental coverage or life insurance multiples, parental leave generates direct, personal financial calculations: how much will I receive, for how long, and what will that mean for my family’s finances and my ability to be present during a period that does not repeat?

Employers who have invested in a strong parental leave program and are not talking about it are leaving one of their best recruiting assets on the table. A program that offers twelve or more weeks of additional paid leave, a top-off to full salary, and bonding leave for non-birth parents is well above the national market on all three dimensions. That is a specific, documentable competitive advantage in candidate conversations, offer letters, and employer brand communications. It does not require marketing language. It requires knowing what your program provides and being willing to state it clearly.

Employers who are uncertain about where their program stands face a different challenge. If you are not sure whether your maternity leave duration, your disability payment rate, your top-off policy, and your non-birth parent bonding leave compare favorably to the employers recruiting against you, you cannot use those elements as differentiators, and you cannot address them strategically at renewal. The national benchmarks in this post give you the market context. The custom cohort analysis Mployer builds from employers matching your industry, region, and size gives you the specific comparison that matters for your talent market.

Parental leave policy is not static. The market has moved meaningfully in the past five years and continues to move. Employers who last reviewed their parental leave program three or more years ago are likely benchmarking against a standard that has already shifted. Knowing where you stand today is the starting point for deciding whether to maintain, improve, or actively use your program as a recruiting asset.

See how your parental leave and full benefits package compare to your custom cohort at MployerAdvisor.com.

Sources

Mployer Insights, 2026 Benefits State of the Union: Leave & Workplace Flexibility. Source: Mployer Insights analysis of 50,000+ employer benefit plans. All Nation Average.

Family and Medical Leave Act of 1993 (FMLA), 29 U.S.C. Section 2601 et seq. Applies to employers with 50+ employees.

Pregnancy Discrimination Act, 42 U.S.C. Section 2000e(k). Applies to employers with 15 or more employees.

PUMP for Nursing Mothers Act (2022), amending the Fair Labor Standards Act. Applies to most employers.

State paid family leave programs: California (SDI/PFL), New Jersey (TDI/FLI), New York (NY DBL/PFL), Washington (WA PFML), Massachusetts (MAPFML), Oregon (OPFML), Colorado (FAMLI), Rhode Island (TCI), Connecticut (CTPFML), District of Columbia (DC PFML).

IRS adoption assistance exclusion 2026: $17,280 per child, per IRS Notice 2025-61.

Leave Is the Benefit Employees Feel Every Week

Mployer rates employer benefit plans across four pillars: Medical, Ancillary, Leave, and Retirement. Of the four, leave carries the lowest direct cash cost to the employer outside of the opportunity cost of time away from work. And yet leave is consistently among the highest-valued benefits employees cite, particularly among workers entering the workforce in the past two decades. For younger employees who grew up with greater flexibility as an expectation rather than a perk, PTO policies, remote work options, and holiday calendars are not peripheral considerations. They are factors that influence job acceptance decisions, day-to-day job satisfaction, and the calculus of whether to stay or leave.

This is Part 1 of a two-part series on leave benefits. This post covers the foundational elements: vacation, paid holidays, sick leave, consolidated vs. non-consolidated leave structures, workplace flexibility, and the legal framework that governs when leave is required vs. when it is discretionary. Part 2 will go deep on maternity and parental leave, including benefit duration, disability payment interaction, top-off provisions, and how this rapidly evolving category varies by industry and employer size.

The Legal Framework: What Is Required and What Is a Choice

Before reviewing the benchmarks, it is important to understand the distinction between leave that employers are legally required to provide and leave that is entirely discretionary. Many employers conflate these, either overclaiming legal mandates that do not apply to them or unknowingly underdelivering on ones that do.

FMLA: The Federal Floor

The Family and Medical Leave Act of 1993 (FMLA) is the primary federal law governing employee leave. It requires covered employers to provide eligible employees with up to 12 weeks of unpaid, job-protected leave per year for qualifying reasons, including the birth or adoption of a child, a serious health condition of the employee or a close family member, or qualifying military exigencies. A critical word in that sentence is unpaid. FMLA guarantees job protection and continuation of health insurance during leave. It does not require the employer to pay the employee during that time.

FMLA applies to employers with 50 or more employees within 75 miles. Eligible employees must have worked for the employer for at least 12 months and logged at least 1,250 hours in the prior year. Employers below 50 employees are not covered by federal FMLA, which is a meaningful distinction for the substantial share of small employers in the national workforce.

State Leave Laws: A Patchwork Expanding Rapidly

State leave laws have multiplied significantly over the past decade and frequently go beyond FMLA in scope, coverage thresholds, or paid leave requirements. Several categories are worth understanding:

The practical implication for any multi-state employer: your leave compliance obligation is not a single federal standard. It is the most protective standard that applies in each jurisdiction where you have employees. Staying current requires active monitoring as state laws continue to evolve.

Paid Holidays: No Federal Requirement for Private Employers

Here is a fact that surprises many employees and even some HR professionals: private sector employers in the United States have no federal legal obligation to provide any paid holidays. The list of federal holidays, which includes New Year’s Day, Independence Day, Thanksgiving, Christmas, and others, applies to federal government employees. Private employers are entirely free to choose which holidays to observe, how many to provide, and whether they are paid.

In practice, the market has established strong norms around holiday calendars. Employers who observe fewer than the common major federal holidays face a competitive disadvantage in recruiting. But the specific holidays offered, the total number, and whether floating holidays or personal days supplement the calendar are all employer-determined choices with real variation in the market.

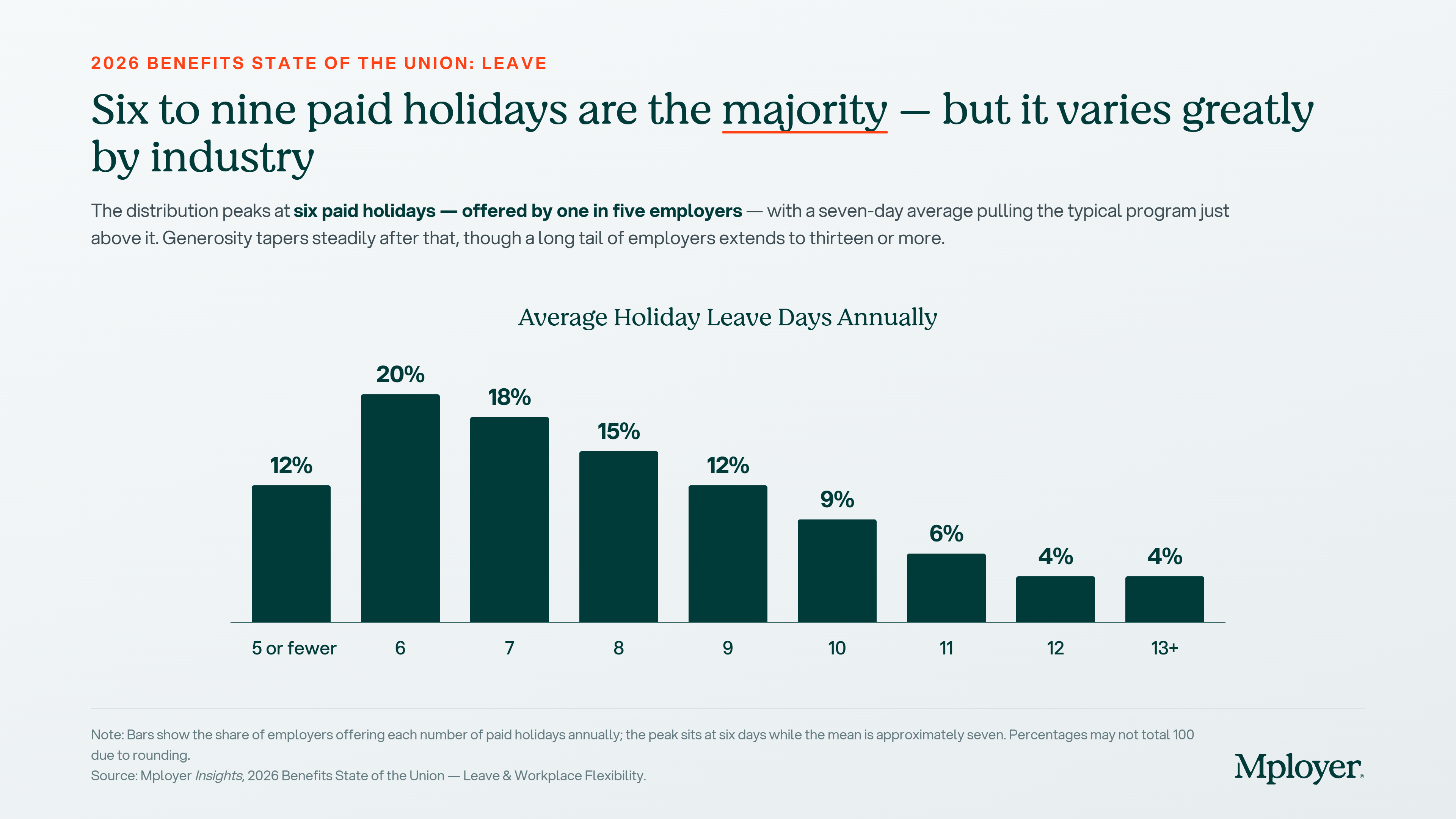

Six paid holidays is the single most common offering nationally, provided by one in five employers. But the distribution spans from five or fewer to thirteen or more, and the seven-day average is pulled upward by generous employers at the top of the range. The practical range of six to nine days covers 65% of employers. An employer offering five or fewer paid holidays is below market in a way that is visible to candidates who are comparing offers. An employer offering ten or more is offering a genuinely above-market benefit that is worth communicating explicitly in recruiting.

It is also worth noting the difference between public and private sector norms. Federal and state government employers typically observe all federal and state holidays, often reaching 11 or more paid days annually. Private employers who compete for talent against government roles, especially in certain regions or professional categories, face a visible gap if their holiday calendar is at the lower end of the private sector range.

Key Terms Every Benefits Decision Maker Should Know

The chart above shows a consistent pattern across all tenure milestones: employees at employers with consolidated leave plans receive meaningfully more vacation days than those on non-consolidated plans. At one year of tenure, the gap is 4.3 days (13.5 consolidated vs. 9.2 non-consolidated). At 20 years, the gap is 4.2 days (22.3 vs. 18.1). This reflects the structural reality that consolidated plans typically set a total PTO balance that includes what would otherwise be split across vacation, sick, and personal categories. The total bank is larger because it is serving multiple purposes.

The tenure progression also matters for employers thinking about leave as a retention tool. An employee at year 5 in a consolidated plan has 17.6 days. Their counterpart at a non-consolidated employer has 13.2. That 4.4-day difference compounds over a career and becomes a meaningful factor in whether a tenured employee considers leaving. Employers who have not benchmarked their vacation accrual schedule by tenure against peers in their industry and size band may not realize how their program compares at the years of service where retention pressure is highest.

Workplace Flexibility: The Post-Pandemic Recalibration

Workplace flexibility surged during the pandemic and became one of the most cited employee preferences in every post-2020 benefits survey. The 2026 data shows the market pulling back from its pandemic peak. Fully remote arrangements are now offered by 23% of employers, work-from-home options by 22%, and unlimited PTO by just 9%. These numbers are lower than what many employees experienced at the height of 2020 to 2022, and that gap between expectation and current market reality is one the most active sources of employee dissatisfaction in leave-related discussions.

For employers, the flexibility picture requires honest self-assessment. If your organization has pulled back from flexibility arrangements that were extended during the pandemic, the competitive context has shifted: the employers who maintained those arrangements are now differentiating on a dimension that is highly visible to candidates. If your business model genuinely requires in-person work, the relevant benchmark is not the fully remote employer but the other employers in your industry and region competing for the same workforce. That is exactly the kind of cohort comparison a custom benchmarking analysis provides.

Sick Leave and Carryover: The Details That Matter

Sick leave policy is one of the most administratively variable elements of a leave program. 65% of employers offer a carryover provision that allows unused sick days to roll into the following year. 19% allow unlimited carryover, placing no cap on the sick day balance an employee can accumulate over time. Use-it-or-lose-it sick policies, while simpler to administer, can create employee hardship in years with significant illness and may conflict with state-level sick leave mandates in jurisdictions that explicitly require carryover.

The interaction between sick leave and short-term disability coverage is also worth understanding. For many employers, sick leave effectively serves as the waiting period, or elimination period, before short-term disability benefits begin. An employee with 10 accrued sick days who experiences a two-week illness may use those sick days before STD coverage activates. Employees without sufficient sick leave balances, or in plans where sick leave and STD do not coordinate, face an income gap. How these two programs interact is a design decision that affects real employee financial security and is worth reviewing explicitly.

A Note on Maternity and Parental Leave

Nationally, 68% of employers offer dedicated maternity leave beyond what statutory short-term disability provides. 32% do not. That statistic is at the national level and covers all employer sizes and industries. The variation beneath that headline number is significant: duration of paid leave, how disability income is structured, whether employers top off the disability benefit to approach full salary replacement, bonding leave for non-birth parents, and adoption leave policies all vary widely. These dimensions are among the most actively discussed benefits in today’s candidate conversations and are closely tracked by employees considering family formation.

Part 2 of this series will go deep on maternity and parental leave. We will cover average paid leave duration by industry, how short-term disability interacts with maternity leave, what topping off disability means and how common it is, paternity and non-birth-parent bonding leave benchmarks, and adoption leave trends. If your organization is actively recruiting in competitive talent markets or is thinking through a parental leave update ahead of open enrollment, that post is worth reading closely.

Leave as a Competitive Differentiator: How to Use It, How to Talk About It

Leave benefits are one of the most emotionally resonant elements of an employee’s relationship with their employer. They represent how an organization actually treats its people when life happens: when someone is sick, when a child is born, when a family member needs care, or when an employee simply needs time to recharge. Employees who feel their leave program is generous are more likely to stay. Employees who feel it is stingy are more likely to leave, and more likely to say so in exit interviews and public reviews.

The challenge for most employers is that they do not know how their leave program actually compares. They know their own policy, but they do not know whether their vacation accrual schedule, their holiday count, their sick leave carryover rules, and their flexibility arrangements are above market, at market, or below market against the specific employers competing for the same candidates. Without that context, it is impossible to talk credibly about leave as a differentiator or to address an employee’s complaint about time off with anything more than a defensive response.

The next time an employee raises a concern about paid time off, or a candidate asks how your leave program compares, you should be able to answer with data. Not a general impression that your program is competitive, but a specific, benchmarked answer: our employees at five years of tenure receive 17.6 days of paid time off, which is above the national average for employers in our industry and size band. That answer requires knowing where you stand, and knowing where you stand requires a benchmark built from employers who actually look like you, not a national average that flattens the variation that matters.

Strong leave programs are also an underused marketing asset. Employers who score at Market Leading or above in the Mployer Leave pillar have a specific, documented, independently verified statement to make in offer letters, careers pages, and job postings: our leave program has been rated above market against employers in our industry, region, and size. That is a recruiting signal most employers are not making, because most employers have never taken the step of finding out whether they could make it.

See how your leave program compares to your custom cohort at MployerAdvisor.com. Part 2 on maternity and parental leave is coming soon.

Sources

Mployer Insights, 2026 Benefits State of the Union: Leave & Workplace Flexibility. Source: Mployer Insights analysis of 50,000+ employer benefit plans.

Family and Medical Leave Act of 1993 (FMLA), 29 U.S.C. Section 2601 et seq. Applies to employers with 50+ employees within 75 miles.

U.S. Department of Labor: Federal holidays apply to federal government employees; private employers have no federal obligation to provide paid holidays.

State paid family and medical leave programs: California (CFRA/SDI), New York (NY PFL), New Jersey (NJFLA), Washington (WA PFML), Massachusetts (MAPFML), Oregon (OPFML), Colorado (FAMLI), Connecticut (CTFMLA), and others.

.png)

Mployer materially expands the AI and agentic capabilities across its product suite and expands access to its MCP Server and Claude Connectors, making Mployer's proprietary 2 billion data points across benefits and insurance accessible inside partners' own LLMs.

Nashville, TN, July 16, 2026 /PRNewswire-PRWeb/ --

Mployer, the industry's leading employee benefits and insurance intelligence platform, today announced its Expanded AI Release powered by Anthropic. This release is a major expansion of the AI and agentic abilities already built across its products, and it includes the broad release of its MCP (Model Context Protocol) Server and Claude Connectors. This Expanded AI release allows our partners to access Mployer's 2 billion proprietary benefit and insurance data points both inside Mployer and inside their own LLM.

This functionality is coupled with an expert benefit AI-agent trained on these 2 billion data points to provide superior strategic advice and support for our partners at every step in their workflow, across every Mployer solution - from market analytics to benchmarking, claims and compliance. It is similar to having a highly educated insurance expert with 30+ years of experience sitting side by side with every individual partner at every step.

In addition, in line with the company's goal of better enabling all industry participants, Mployer is releasing a limited, free version of every product. There will be a national training on July 28 and August 5 that is for everyone in the industry. To sign up for limited free access and the national training on July 28th, or request access to the Mployer MCP, please see further details below.

"This release raises the bar for what AI can do for our industry," said Brian Freeman, CEO of Mployer. "Applying this next level of AI

across our platform and the broker and carrier workflows gives insurance industry leaders powerful, proprietary market data to support their strategies and decisions. We are entering an awesome era for our industry, where the brokers and carriers using the best analytics will deliver differentiated outcomes for their employer partners. That will continue to drive collective, positive industry impact. We're excited for our partners and for Mployer to play a material role in this next era."

Infusing AI into every step of the workflow:

Mployer's benefits and insurance AI Agent has been highly trained on Mployer's 2 billion unique benefits and insurance data points, and sits alongside leading producers across each step of their workflow, including:

"Imagine being a producer today and starting your morning with updates from your expert benefits AI assistant: 'Your client's renewal is trending 14% above their cohort benchmark, attached are draft strategies for your review,' or 'An HR director from one of our partners is now the CHRO at a new company, attached is a draft congratulatory email,' or 'A new proposed Texas law impacts three of our groups, attached is a communication for your review.' That is the reality of what this release and the next era bring," said Anthony Waters, Chief Growth Officer of Mployer. "It is a great time to be a part of this industry."

To receive limited, free access to every product, you need to attend one of the trainings:

Each product training is 20 minutes. You can join only the specific solutions you would like to learn more about.

To request access to Mployer's MCP Server and Claude Connectors, please reach out to [email protected].

About Mployer

Mployer is the industry's leading employee benefits and insurance intelligence platform, built for brokers, carriers, GAs, PEOs, and the employers they serve. Powered by more than 2 billion unique benefit data points and Anthropic, Mployer's suite of Catalyst, Insights, Vista, Pulse, and Atlas works for industry leaders benchmarking plans, analyzing claims, recommending growth strategies, and interpreting complex policies and legislation, in one platform. With its MCP Server and Claude Connectors, Mployer's data and AI are accessible across its products and directly within Claude. Learn more at MployerAdvisor.com.

Media Contact: Anthony Waters Chief Growth Officer, Mployer [email protected]

Media Contact

Anthony Waters, Mployer, 1 774 2879741, [email protected], https://MployerAdvisor.com

.png)

What Every Benefits Decision Maker Needs to Know

If you sit on a benefits committee, approve vendor contracts, set plan design, or sign off on employee benefit programs, you are a fiduciary under ERISA. That responsibility comes with real legal exposure, and the litigation environment surrounding it has grown substantially over the past decade. The Consolidated Appropriations Act of 2021 added new teeth to this exposure by requiring health insurance brokers and consultants to disclose all direct and indirect compensation they receive in connection with employer health plans. That disclosure requirement has become a direct underpinning of a new and expanding wave of ERISA lawsuits, as plaintiff firms use disclosed compensation data to allege that employers failed to monitor whether their brokers were acting in the plan’s interest or their own, including in voluntary benefit programs where broker commissions are now under direct scrutiny. Understanding that environment is not a reason for alarm. It is a strong reason to ensure your process is documented, your decisions are benchmarked, and your programs are structured in a way that reflects the care the law requires.

The Employee Retirement Income Security Act of 1974, known as ERISA, was enacted to protect employees from the mismanagement of benefits promised to them. It does that by imposing fiduciary duties on anyone who exercises discretionary authority over a benefit plan or its assets, from benefits committee members and HR leaders to the brokers and consultants who advise them.

This post explains who is at risk, what the key legal theories are, and where this is heading.

Defined contribution plans still drive the majority of ERISA class actions, representing 63% of the 155 cases filed in 2025, tracked by Encore Fiduciary in partnership with the Dorsey & Whitney law firm. But health plan cases are the fastest-growing category, accounting for 25% of all filings in 2025. That share reflects the direct impact of the CAA’s disclosure requirements and the growing sophistication of plaintiff firms in applying ERISA fiduciary standards to health plan administration. Annual excessive-fee and imprudent-investment filings remain elevated, with 2025 among the busiest years on record at 94 cases, and the trajectory since 2020 reflects a litigation environment that has become structurally elevated, not cyclical.

Who Bears Fiduciary Responsibility

ERISA fiduciary status is not limited to the HR department or the plan administrator on the plan document. Anyone who exercises discretionary authority over a benefit plan, controls plan assets, or provides investment advice for a fee can be a fiduciary under ERISA. In practice, that includes:

The standard that applies is the prudent expert standard under ERISA Section 404(a)(1)(B): decisions must reflect the care, skill, and diligence of a person familiar with such matters, acting in the sole interest of plan participants. Courts do not evaluate fiduciary duty by asking whether the outcome was good. They ask whether the process was sound. Process is the protection.

How This Litigation Actually Works

Most benefits decision makers are surprised to learn how these cases get started. Plaintiff law firms do not wait for disgruntled employees to call. They use publicly available Form 5500 annual filings, which ERISA plans must submit to the Department of Labor, to screen for plan characteristics that have historically generated successful claims. Once a target is identified, the firm recruits a plan participant to serve as the named plaintiff in a class action, frequently through outreach to current or former employees. That participant’s role is to provide legal standing, not to describe a personal grievance. The firm files the complaint, and the employer is now in litigation that can cost millions to defend regardless of the merits.

This explains a pattern that otherwise seems contradictory. Recordkeeping fees and investment fees for large 401(k) plans have declined steadily for more than a decade, yet fiduciary litigation has accelerated over that same period. Plaintiff firms have found that surviving the early stage of litigation generates settlement leverage, and their business model does not require the underlying fees to actually be excessive. In our internal data, over the past five years there have been more than 200 settlements of excessive fee and imprudent investment lawsuits totaling more than $1.3 billion. Plaintiff firms typically receive approximately one-third of those settlements. Individual plan participants, by contrast, have received an average of $55 to $70 each per settlement according to analysis from the Davis & Harman law firm.

Excessive Vendor Fees Drive the Surge

Excessive-fee allegations jumped 64% in a single year, from 45 cases in 2024 to 74 in 2025, outpacing every other claim category. Forfeiture allegations rose from 29 to 48. Imprudent investment claims grew from 48 to 53. Across all three categories, the trend is consistently upward. The right panel of the chart below shows what that volume translates to in settlement dollars: total reported settlements peaked at $352.8 million in 2023 and have remained elevated, with $151.9 million settled in 2025 alone. Watchful, deliberate fee benchmarking is the plan sponsor’s strongest defense against all three of these claim types, because each ultimately turns on whether the fiduciary made a documented, reasonable, and informed decision about what the plan was paying and to whom.

One category deserves particular attention for employers running wellness programs: tobacco surcharge claims. Plans that impose premium surcharges on tobacco users must offer a reasonable alternative standard that allows employees to earn or recoup the full reward, typically a tobacco cessation program. Nearly 50 tobacco surcharge lawsuits were filed in 2024 and 2025, with multiple settlements reaching close to $5 million each. Courts have ruled in favor of plaintiffs in the large majority of motions to dismiss decided so far. This is one of the highest-frequency, most correctable compliance risks in health plan design today.

The Main Legal Theories: A Brief Overview

In defined contribution plans, the dominant allegations are excessive recordkeeping or investment fees, imprudent investment selection, and forfeiture allocation disputes. Health plan litigation has grown significantly since the CAA’s fee disclosure requirements took effect, with the most active categories now being prescription drug cost claims, tobacco surcharge violations, ghost network failures, and, most recently, voluntary benefit broker compensation arrangements where undisclosed or unreasonable commissions are now being scrutinized directly under ERISA Section 406.

Cases That Illustrate Where the Exposure Lives

These cases show the range of conduct generating ERISA fiduciary liability claims across both retirement and health plans, and why the risk is expanding well beyond the traditional 401(k) space.

What Well-Prepared Employers Are Doing Differently

The employers best positioned in this litigation environment treat fiduciary process as an ongoing discipline. The specific practices courts and regulators look for are consistent across plan types.

How Mployer Insights+ Supports Your Fiduciary Process

One of the most direct steps a benefits decision maker can take to strengthen their fiduciary position is to run an independent, third-party benchmarking review of their plan on a regular basis. This is what Mployer Insights+ is built to produce.

Completing an Insights+ review generates documentation that speaks to three of the core ERISA fiduciary obligations. On the prudent expert standard under Section 404(a)(1)(B), the report demonstrates that an independent, structured benchmarking analysis was conducted across all plan components. On cost reasonableness under Section 404(a)(1)(A), the cohort comparison against employers matched by size, region, and industry creates a data-driven, documented basis for evaluating whether plan costs fall within a reasonable market range. On the duty to monitor under Section 404(a)(1), running the review annually establishes a consistent cadence of evaluation with a written output each cycle.

Because Mployer has no carrier relationship, broker relationship, or financial arrangement with the plan being evaluated, the report reflects an objective assessment free of commercial bias. That independence speaks directly to the implicit requirement in the prudent expert standard that fiduciary analysis be conducted free of conflicts of interest, and it distinguishes the Insights+ review from a benchmark produced by a broker from their own book of business.

None of this is a substitute for legal advice, and employers should work with qualified ERISA counsel to confirm all applicable obligations are identified and satisfied. But in a litigation environment where 155 fiduciary class action lawsuits were filed in a single year and the scope is actively expanding into health plans and voluntary benefits, a documented annual benchmark is one of the most practical and defensible steps a benefits team can take.

See how your benefits package compares to your custom cohort at MployerAdvisor.com.

Sources

Encore Fiduciary / Dorsey & Whitney LLP: ERISA Fiduciary Litigation in 2025. 155 class lawsuits filed in 2025. Justin Bove, Chief Revenue Officer, Encore Fiduciary.

Mployer Insights analysis of public ERISA class-action filings and settlements, 2016-2025.

Davis & Harman LLP: 2025 Underperformance and Excessive Fee Settlement Survey. Average individual participant recovery $55-$70.

Consolidated Appropriations Act of 2021 (CAA), Section 202, broker/consultant compensation disclosure requirements for group health plans.

Kraft Heinz Co. Employee Benefits Administration Bd. v. Aetna Life Ins. Co., No. 2:23-cv-00317 (E.D. Tex., filed June 30, 2023).

Lewandowski v. Johnson & Johnson, No. 3:24-cv-00671 (D.N.J., filed February 5, 2024).

Navarro v. Wells Fargo & Co., No. 0:24-cv-3043 (D. Minn., filed July 30, 2024).

Hecht v. Cigna, filed 2024; fiduciary duty claim survived motion to dismiss February 2025; settled approximately $6 million October 2025.

Singh v. Capital One Financial Corporation, PACER Docket 1:24-cv-08538; settled approximately $10 million 2025.

Cunningham v. Cornell University, 604 U.S. 693 (2025).

Hughes v. Northwestern University, 595 U.S. ___ (2022).

ERISA Section 404, 29 U.S.C. Section 1104. DOL Voluntary Plan Safe Harbor, 29 C.F.R. Section 2510.3-1(j).

HIPAA Nondiscrimination Rules for Wellness Programs, 26 C.F.R. Section 54.9802-1.

A Quiet Docket, a Loud Signal for Benefits Leaders

The Supreme Court closed its October 2025 Term on June 30, 2026, and for once the biggest story for employee benefits is what the justices didn’t take up. After several years of consequential ERISA rulings, this term was unusually light on benefits cases. ERISA was the only major regulatory area the Court touched at all this cycle.

For CHROs and CFOs, that quiet is deceptive. The decided cases were narrow, but the case the Court agreed to hear for next term, combined with a fast-moving wave of litigation in the lower courts, means the exposure landscape is shifting under your feet even in a slow year. Here is what actually happened, and what belongs on your calendar.

A quick scheduling note. The Court runs on a fixed rhythm, opening the first Monday in October and running through late June. This term began October 6, 2025 and wrapped June 30, 2026. The next term, October Term 2026, begins October 5, 2026. That is when the case worth watching most closely will be argued.

The One Decided Case: M&K Employee Solutions

The term’s marquee ERISA decision was M&K Employee Solutions, LLC v. Trustees of the IAM National Pension Fund, decided unanimously on May 21, 2026, in an opinion by Justice Jackson.

The case concerned multiemployer pension plan withdrawal liability, the “exit tax” an employer owes when it stops contributing to an underfunded union pension plan. The narrow legal question: must the plan’s actuary lock in the actuarial assumptions, most importantly the interest and discount rate, as of the measurement date, or can those assumptions be set later? The Court held that assumptions do not have to be fixed on the measurement date. The measurement date fixes the facts about the plan, its assets, its participant data, but the actuary may select assumptions afterward, so long as they rest on information available as of that date.

Why It Matters, and to Whom

If your organization participates in a multiemployer plan, this decision removes a timing-based defense to a withdrawal liability assessment. The stakes are not theoretical. In the underlying dispute, a single change in the discount rate swung the fund’s unfunded liability from roughly $500 million to $3 billion. Employers can still challenge an assumption as unreasonable on the merits, but they can no longer argue it is invalid simply because it was adopted after the measurement date.

For CFOs with any multiemployer exposure, the practical takeaway is straightforward: keep current withdrawal-liability estimates in hand and treat assumption volatility as a live balance-sheet risk, not a historical footnote.

For the majority of employers, those sponsoring 401(k) or other single-employer defined contribution plans, M&K is informative but not directly actionable. Which is exactly why the next case deserves your attention.

The Case to Watch: Anderson v. Intel

In January 2026, the Court granted review in Anderson v. Intel Corp. Investment Policy Committee. This is the decision benefits leaders should be tracking closely. It has not yet been argued. It sits on the October 2026 calendar, with a ruling expected sometime in 2027.

The question is deceptively technical but enormously consequential: when a 401(k) participant sues plan fiduciaries for imprudently selecting or retaining an underperforming investment, must the complaint identify a “meaningful benchmark,” an appropriate comparator investment, to survive a motion to dismiss?

That pleading standard is the gate through which nearly every fiduciary-breach class action must pass. Set it high, and many suits end early, before discovery costs accumulate. Set it low, and far more cases proceed into expensive, prolonged litigation. However the Court rules, it will reset the cost-benefit calculus of fiduciary litigation for every plan sponsor in the country.

The action item here is concrete: put Anderson v. Intel on your 2027 watch list now, and revisit your investment-monitoring documentation in anticipation. Whatever standard the Court ultimately adopts, employers with a thin or informal fiduciary process will be the most exposed.

The Real Action Is Below the Supreme Court

If you read only the SCOTUS headlines, you would miss the trend most relevant to your benefits program today. Two lines of litigation are accelerating in the lower courts, and both are worth understanding now, well before either reaches the Supreme Court, if either ever does.

Voluntary and Ancillary Benefits Litigation

Building on the Court’s 2025 decision in Cunningham v. Cornell, last term’s ruling that lowered the bar for pleading an ERISA prohibited-transaction claim, plaintiffs’ firms have begun filing class actions over voluntary benefit programs such as accident, critical illness, and hospital indemnity coverage.

The theory: that employers failed to ensure premiums were reasonable, and that the brokers and consultants who placed those products acted as plan fiduciaries and engaged in self-dealing through undisclosed commissions. Notably, these suits name not just employers but their advisors directly.

The first line of defense is the Department of Labor’s voluntary-plan safe harbor. If your voluntary offerings do not satisfy all four of its requirements, ERISA fiduciary duties may attach to programs you never treated as fiduciary plans. That means the governance, documentation, and disclosure standards you apply to your 401(k) may now be relevant to your accident and critical illness offerings as well.

Forfeiture Litigation

A growing set of cases is challenging whether plan sponsors may use forfeited employer contributions, the unvested employer match dollars left behind when an employee departs before vesting, to offset future company contributions, rather than using those dollars to defray plan administrative expenses.

The Supreme Court has not taken these cases up, but the circuits are actively sorting through conflicting outcomes, and the resolution will shape a routine plan-design choice that most sponsors make without a second thought. If your plan document allows forfeitures to offset future employer contributions, a common and previously uncontroversial provision, it is worth understanding where the circuit split currently stands and how exposed your specific plan language is.

On the Health Side: A Notable Non-Decision

In January 2026, the Court declined to wade in. It denied review in Guardian Flight v. Health Care Service Corp., leaving intact a lower court ruling that there is no private right of action to enforce arbitration awards under the No Surprises Act’s dispute-resolution process. It’s a quiet development, but a meaningful data point for any employer managing surprise-billing and network-adequacy issues. The enforcement mechanism for No Surprises Act arbitration outcomes remains narrower than some plan sponsors may have assumed.

What to Do Before October

A light term is a planning window, not a reprieve. Three concrete moves worth making before the Court reconvenes:

The Justices Return October 5. The Quiet Won’t Last.

This term’s light docket should not be mistaken for reduced risk. The lower courts are actively developing theories around voluntary benefits, forfeitures, and fiduciary process that will shape benefits litigation for years regardless of whether the Supreme Court ever weighs in directly. And the one case already on next term’s calendar, Anderson v. Intel, has the potential to reset how every fiduciary-breach claim in the country gets pleaded and litigated.

Benefits compliance is not a once-a-year exercise triggered by a Supreme Court ruling. It is an ongoing discipline of documentation, benchmarking, and process, and the employers best positioned heading into next term are the ones treating it that way now.

Mployer’s benefits rating evaluates plan design and employer investment across Medical, Ancillary, Leave, and Retirement, giving CHROs and CFOs a documented, benchmarked view of how their plans compare to a custom cohort. That is precisely the kind of process discipline courts are increasingly looking for.

This is also where Mployer Insights+ does double duty. Running an Insights+ review produces the kind of independent, third-party documentation that speaks directly to ERISA’s prudent expert standard under Section 404(a)(1)(B). The report benchmarks your plan against a custom cohort matched by size, region, and industry, which gives you a data-driven basis for evaluating whether your costs and plan design fall within a reasonable market range under the cost reasonableness standard in Section 404(a)(1)(A).

It also addresses the duty to monitor under Section 404(a)(1), which is an ongoing obligation, not a one-time exercise at plan inception. An annual Insights+ re-rating establishes exactly the kind of recurring, documented review cadence that obligation calls for, with a written output each cycle that shows the analysis was conducted. Because the report is produced by an independent third party with no carrier or broker relationship to the plan being evaluated, it also speaks to the independence of assessment that the prudent expert standard implies.

None of this is a substitute for legal advice, and plan sponsors should work with qualified ERISA counsel to confirm all applicable obligations are identified and satisfied. But for CHROs and CFOs looking to strengthen their fiduciary process ahead of a term where the lower courts are actively raising the bar on documentation, an annual Insights+ review is a concrete, repeatable way to build that record.

See how your benefits package compares to your custom cohort at MployerAdvisor.com.

Sources

M&K Employee Solutions, LLC v. Trustees of the IAM National Pension Fund, decided May 21, 2026 (unanimous, opinion by Justice Jackson).

Anderson v. Intel Corp. Investment Policy Committee, certiorari granted January 2026; argument calendared for October Term 2026.

Cunningham v. Cornell University, decided 2025 (prior term).

Guardian Flight v. Health Care Service Corp., certiorari denied January 2026.

American Bar Association, October 2025 Term preview.

July brings major updates across Insights+, Catalyst, and Vista, focused on helping our partners work faster with more automation, deeper intelligence, and expanded AI capabilities, from instant benchmarking reports and smarter prospecting to more flexible reporting. Explore the updates below.

Insights+

Catalyst

Vista

Vision Benefits: The Most Widely Offered Ancillary Benefit Employers Get the Least Credit For

Vision is the most commonly offered ancillary benefit in employer-sponsored plans. In fact 89% of employers offer it nationally, higher than dental, higher than life insurance, and higher than any voluntary benefit. And yet vision is also one of the most underfunded benefits in the market. The average employer contributes $3 per month toward a single employee’s vision premium. For a family, the average is $6.

That disconnect: near-universal offer rate, near-zero employer contribution, is the central story in vision benefits today. Employees enroll in vision at a 74% rate when it’s offered, making it a high-utilization benefit. But the financial signal most employers are sending through their contribution level is that vision is an afterthought: available, but not invested in. This piece covers the national benchmarks on offer rates, plan structure, contributions, coverage design, and the carrier market so employers can see exactly where their vision program stands.

Offer Rates and Plan Structure

Vision is offered by 89% of employers nationally the highest offer rate of any ancillary benefit. Among those who offer it, 74% of eligible employees enroll. That utilization rate is significant: nearly three out of four employees who are given access to vision coverage use it, which means the benefit is genuinely visible to your workforce. Employees notice when they use a benefit and when their coverage is adequate or not.

On plan structure, vision is even simpler than dental. A strong majority of employers offer a single vision plan 95% nationally. Two-plan structures are rare, and three or more plans are essentially nonexistent. Vision plan design is standardized enough that a single well-designed plan serves most workforce demographics without requiring the complexity of a buy-up option. The decision is less about how many plans to offer and more about whether the single plan you offer is adequately structured.

Employer Contribution: A Market-Wide Gap

Vision employer contributions are low across the board, and that’s not unique to any particular employer it’s a market-wide pattern. The national breakdown:

The 41% contributing nothing stands out it’s materially higher than the comparable figure for dental (26%). Nearly half of all employers offering vision are passing the entire cost to employees. Among those who do contribute, the averages are modest: $3 per month for single coverage and $6 per month for family coverage, representing 50% of the single premium and 36% of the family premium.

The total vision premium is low enough that the contribution gap may seem inconsequential in isolation: $7 per month for single coverage, $21 per month for family. But the contribution pattern sends a signal that employees read into the broader benefits package. An employer covering 50% of a $7 single premium a $3.50 monthly contribution is technically contributing, but the gesture is so small it barely registers. Employers who cover vision premiums in full, or contribute at a meaningful level, stand out against a market where most employers are doing the minimum.

Plan Design: What Vision Coverage Actually Covers

Vision benefits are structured around a set of specific coverage elements: the annual eye exam, corrective lenses (glasses or contacts), and frames. Understanding how each element is designed and how frequently coverage refreshes is where meaningful plan differences emerge.

Copayments

Vision plans typically use copayments rather than coinsurance at the point of service. The national benchmarks:

A $10 exam copay and $25 materials copay are well-established market standards. Employers above these benchmarks charging $25 for an exam or $50 for materials are meaningfully above the market norm on employee cost-sharing for a benefit that costs very little to provide generously.

Lens and Contacts Reimbursement

For corrective lenses and contact lenses, plans reimburse up to a maximum allowance. The national benchmarks by percentile:

The tight clustering at the 50th and 75th percentiles both at $150 reflects how standardized vision reimbursement levels have become. The median and the 75th percentile are the same number, which means the majority of competitive vision plans land at or near $150 for lens reimbursement. An employer with a $100 allowance is visibly below market; an employer at $150 is squarely competitive.

Contacts Coverage

Contact lens coverage comes in two structures, and the difference matters for employees who wear contacts exclusively:

The in-lieu-of-frames structure is the more important benchmark for contact lens wearers. An $80 allowance is the national average, but contact lens costs can easily exceed that a year’s supply of daily disposable contacts often runs $400–$800 before any reimbursement. Employers evaluating their vision plan should check both the contacts allowance and whether the plan requires contacts to be used in lieu of frames or allows both.

Coverage Frequencies: When Benefits Refresh

Vision plans specify how frequently each benefit type refreshes how often employees can get a new exam, new lenses, and new frames under the plan. This is one of the most variable design elements across vision plans, and one employees frequently compare:

The frames frequency is the most differentiated element. A majority of employers refresh frame benefits every 24 months meaning employees can get new frames every other year. The 41% who refresh frames annually are offering a more generous benefit in a category employees notice, since frames are both a functional and aesthetic item that employees actively choose. Annual frame refresh is a low-cost way to differentiate a vision plan from the majority of the market.

How Larger Employers Approach Vision Funding

Like dental, vision benefits are fully insured for the vast majority of employers the employer pays a fixed monthly premium, the carrier assumes the claims risk, and the administrative relationship is simple. This is appropriate for most organizations, particularly those without the scale to make self-insured vision economically meaningful.

For larger employers, self-insured vision follows a similar logic to self-insured dental: vision claims are highly predictable, low in severity, and consistent year over year. At sufficient scale, the carrier’s built-in risk margin becomes a visible cost that can be recaptured through direct claims funding. Self-insured vision adoption follows the same employer-size curve as dental low among small employers and growing significantly as covered-life counts increase, with the most meaningful adoption among employers with 250 or more covered lives.

As with dental, the most common path to self-insured vision at large employers is through the medical plan. When a large employer moves to an ASO arrangement for medical with a major carrier, vision is frequently bundled into the same structure administered by the same carrier, using the same TPA infrastructure, with the employer funding claims directly. The major medical carriers UnitedHealthcare, Aetna, Cigna, and the BCBS plans all offer vision as part of bundled ASO arrangements for large employer groups. This explains why major medical and group insurance carriers appear alongside dedicated vision carriers in the market share data: the two are often linked at the administrative level for large accounts.

The Carrier Market: Who Administers Vision Benefits

The vision carrier market divides into two segments: dedicated vision carriers that specialize in vision benefits, and group insurance and medical carriers that offer vision as part of a broader benefits portfolio.

Vision Service Plan (VSP) is the largest dedicated vision carrier in the country by both employer count and participant count. VSP operates as a not-for-profit and has built one of the largest provider networks in the vision market, which is a meaningful advantage for employers with geographically dispersed workforces. EyeMed, owned by Luxottica (the parent company of LensCrafters, Pearle Vision, and Sunglass Hut), offers broad retail network access as a differentiator particularly for employees who prefer the convenience of in-store vision care. Both VSP and EyeMed are purpose-built for vision and offer strong plan design flexibility.

Guardian Life is a major group insurance carrier with a strong vision product alongside its dental, life, and disability offerings. Guardian’s presence in vision reflects its model of offering bundled ancillary products to employers who want to consolidate their ancillary carrier relationships.

The participant-count view of the carrier market shifts noticeably from the employer-count view. Fidelity Security Life and Sun Life appear prominently when measured by participants but are smaller by employer count a pattern similar to what we see in dental, reflecting their disproportionate presence at large employer accounts. Carriers like Sun Life often enter the vision market through bundled ancillary arrangements with large employers who are already Sun Life customers for stop-loss or group life, giving them access to high-headcount accounts without broad employer-count market share.

For employers evaluating their vision carrier, the key considerations are network access (VSP and EyeMed have the broadest provider networks nationally), retail network options (EyeMed’s retail presence is a genuine differentiator for employees who prefer in-store care), and whether bundling vision with dental or medical creates administrative efficiencies. As with dental, employers who are not bundling through a medical ASO arrangement have full flexibility to select the best-fit vision carrier independently.

What Employers Should Be Asking About Their Vision Plan

Vision is a low-cost benefit relative to medical, which means the gaps between a below-market plan and a competitive one are correctable at modest expense. The key questions:

See How Your Vision Plan Compares to Employers Like You

Most employers don’t know whether their vision plan is above or below market because they’ve never seen it benchmarked against employers who actually look like them. A national average tells you very little. What matters is how your vision contribution, your coverage design, and your carrier compare against other employers in your industry, your region, and your size band.

Mployer rates your vision plan as part of the Ancillary pillar score evaluated against a custom cohort matched to your specific industry, region, and employer size. Whether you’re a 75-person technology company in the Southeast or a 500-person manufacturing employer in the Midwest, the benchmark that matters is the one built from employers who are actually competing with you for the same people.

See how your vision plan — and your full benefits package — compares to your custom cohort at MployerAdvisor.com.

Sources

Mployer 2025 and 2026 Employee Benefit Plan Design Study, covering 50,000+ employer plans. All Size Average, All Region Average, All Industries.

Carrier market share data sourced from Catalyst, a leading analytics platform for carrier market share in the benefits industry. Data reflects fully insured vision plans; market share patterns are broadly representative of self-insured vision plans as well.

Dental Benefits: Small Dollar, High Visibility