Editor's Note: This report is based on survey data from April 2025 that was published in May 2025. This is the most recent data available. (Source: Bureau of Labor Statistics)

US employers exceeded job forecasts by almost one-third, adding 177 thousand new entries to their payrolls last month, which was almost 40 thousand more than had been predicted.

Only 5 states saw a net increase in jobs, however, while the remaining states and Washington DC recorded no meaningful movement in net job figures.

Meanwhile, the national unemployment rate remained essentially unchanged through April at 4.2%.

Over the course of the month, however, 3 states plus Washington DC recorded an increase in statewide unemployment, while 2 states registered a decrease in unemployment rate and the remaining states saw no significant change.

16 states have seen an increase in net jobs throughout the last 12 months, while the remaining 34 plus Washington DC have recorded no net movement over the year.

Below is the breakdown of the Bureau of Labor Statistics’ (BLS) market employment summary from the May 2025 report.

States With the Highest Unemployment Rates

Washington DC was the ‘state’ with the highest unemployment rate last month at 5.8% overtaking Nevada which had been on a 5-month streak with the highest unemployment rate.

The unemployment rate in Washington DC climbed from 5.6% to 5.8% over the month, while Nevada’s unemployment rate continued its downward trajectory, decreasing from 5.7% to 5.6%.

Only 5 other states recorded an unemployment rate that was significantly above the national average in April - Michigan (5.5%), California (5.3%), Kentucky (5.2%), Ohio (4.9%), and Illinois (4.8%).

Besides Washington DC, there were only 3 states that recorded an increase in unemployment rate - Massachusetts (+0.2% unemployment, climbing from 4.4% to 4.6%), Iowa (+ 0.1%, rising from 3.4% to 3.5%), and Virginia (+0.1%, increasing from 3.2% to 3.3%).

Over the last 12 months, 27 states have recorded an increase in unemployment rate, led by Mississippi at plus 1.2% and Michigan at plus 1.1%.

States With The Lowest Unemployment Rates

South Dakota notched its 16th consecutive month as the state with the lowest unemployment rate, holding steady at 1.8% through April.

In total, 19 states recorded unemployment rates significantly below the national average of 4.2%. While South Dakota was the only state to show unemployment below 2%, there were 4 states with unemployment rates below 3% last month - Hawaii (2.9%), Montana (2.7%), Vermont (2.7%), and North Dakota (2.6%).

Over the last month, only 2 states recorded a drop in unemployment rate - Indiana (-0.2%, decreasing from 4.1% unemployment to 3.9% over the year), and Nevada (-0.1%, falling from 5.7% to 5.6%).

Over the last 12 months, only Montana posted a net decrease in unemployment rate at - 0.3%.

States With New Job Losses

No state recorded significant net job losses over the last month or over the last year.

States With New Job Gains

5 states saw a significant increase in net jobs over the course of April. Texas had the largest increase in raw state payroll count at almost 38 thousand, followed by Ohio at about 22 thousand, and North Carolina at about 18 thousand.

In terms of proportional job growth, Arizona, Connecticut, North Carolina, and Ohio all recorded a 0.4% increase, while Texas posted 0.3% growth.

From April 2024 through April 2025, 16 states recorded a net increase in job growth, with the largest raw figure increases occurring in Texas (plus about 216 thousand jobs), Florida (plus about 144 thousand jobs), and New York (plus about 114 thousand jobs).

The largest percentage increase in the state workforce over the last 12 months, however, was claimed by Hawaii (plus 2.7%), followed by South Carolina (plus 2.4%), and Idaho (2.3%).

Mployer’s Take

This report represents the final data from Trump’s first 100 days in office during his second term, which is historically when presidents accomplish a disproportionate amount of their agendas.

That said, many of the workforce cuts in the federal government that have taken place since Trump repurposed the Department of Government Efficiency led by Elon Musk to the task have yet to impact the unemployment and jobs data due to how and when those job reductions are captured and measured.

Similarly, while the threat and implementation of tariffs may yet have a more significant impact on national employment, the vast majority of tariffs that Trump implemented are currently on pause for another 6 weeks, and while the uncertainty is likely affecting the labor market to some degree, the impacts thus far have been relatively minimal.

The continued strength of the labor market has significantly reduced the likelihood that the Fed will bring down interest rates when they meet again to discuss the matter next month. In fact, rate reductions at any point over the summer are looking less realistic at this point, although conditions can change very quickly, especially in the event that the tariff pause is not extended when it expires in early July.

Perhaps the most significant indicators of economic problems that may lay ahead are the interest rates attached to US Treasury bonds, which have been increasing as current investors (both foreign and domestic) unload their bond holdings to a buyer pool that is demanding increasingly higher returns.

Those bond interest rate increases reflect decreased confidence in both short and long term US economic health and increased concern in the ability of the US government to service its growing debt.

Further, these issues may become exacerbated should the Senate get on board with the House’s Big Beautiful Bill given the trillions of additional debt the plan will result in if ultimately enacted into law and if the US GDP growth is unable to offset the spending increases and tax cuts included in the bill.

The US recorded negative GDP growth in the first quarter of 2025 and if that trajectory holds or continues downward, the US economic conditions will be formally labeled as a recession as early as July as well, and while negative GDP growth in the current quarter is not a foregone conclusion, crossing that threshold would likely result in other negative economic feedback effects to pile on the situation.

In short, July may be a very meaningful month when it comes to both determining and assessing the US economic trajectory going forward.

Mployer Launches Sun Life Stop-Loss Data Integration, Enhancing Access to Stop-Loss Insights for Leading Consultants & Employers

Nashville, TN – May 22nd, 2025

Mployer, the nations’ leading employee benefit ratings platform, has partnered with Sun Life U.S. to bring expanded stop-loss analytics into its Mployer Insights platform — giving leading consultants, brokers and employers more powerful tools to navigate rising healthcare costs with clarity.

This partnership introduces Sun Life’s multi-year claims analytics, including detailed stop-loss patterns, trends in high-cost conditions and high cost drug utilization, directly into Mployer’s benchmarking and reporting features. With this addition, consultants and brokers can better anticipate risk patterns and deliver stronger, data-driven guidance to clients.

“Mployer and Sun Life are partnering on new ways to bring valuable stop-loss information and other cost-containment strategies into the hands of employers and leading brokers,” said Brian Freeman, CEO at Mployer. “We are excited to work with leading benefits advisors supporting their work in turning complex claims trends into smarter strategies for their clients.”

The new Sun Life-powered features are available now, with more updates and data expansions to follow later this year.

“This partnership strengthens our mission to provide clear, actionable insights that help brokers guide their clients through complex healthcare and benefit decisions,” said Brian Freeman, CEO at Mployer.

The updated Insights platform is available now, with additional data sources and enhancements planned throughout 2025. To access sample reports or request more detail, go to MployerAdvisor.com.

About Mployer

Mployer is redefining the industry standard for benefits analytics by empowering employers, employees, and benefits consultants to easily assess, rate, and communicate the value of employee benefits. Driven by rising employer costs and increasingly competitive hiring markets, Mployer brings transparency to an industry that affects the over 160 million Americans on employer-sponsored health plans.

About Sun Life

Sun Life is a leading international financial services organization providing asset management, wealth, insurance and health solutions to individual and institutional Clients. Sun Life has operations in a number of markets worldwide, including Canada, the United States, the United Kingdom, Ireland, Hong Kong, the Philippines, Japan, Indonesia, India, China, Australia, Singapore, Vietnam, Malaysia and Bermuda. As of December 31, 2024, Sun Life had total assets under management of C$1.54 trillion. For more information, please visit www.sunlife.com.

Sun Life Financial Inc. trades on the Toronto (TSX), New York (NYSE) and Philippine (PSE) stock exchanges under the ticker symbol SLF.

Sun Life U.S. is one of the largest providers of employee and government benefits, helping approximately 50 million Americans access the care and coverage they need. Through employers, industry partners and government programs, Sun Life U.S. offers a portfolio of benefits and services, including dental, vision, disability, absence management, life, supplemental health, medical stop-loss insurance, and healthcare navigation. Sun Life employs more than 8,500 people in the U.S., including associates in our partner dental practices and affiliated companies in asset management. Group insurance policies are issued by Sun Life Assurance Company of Canada (Wellesley Hills, Mass.), except in New York, where policies are issued by Sun Life and Health Insurance Company (U.S.) (Lansing, Mich.). For more information visit our website and newsroom.

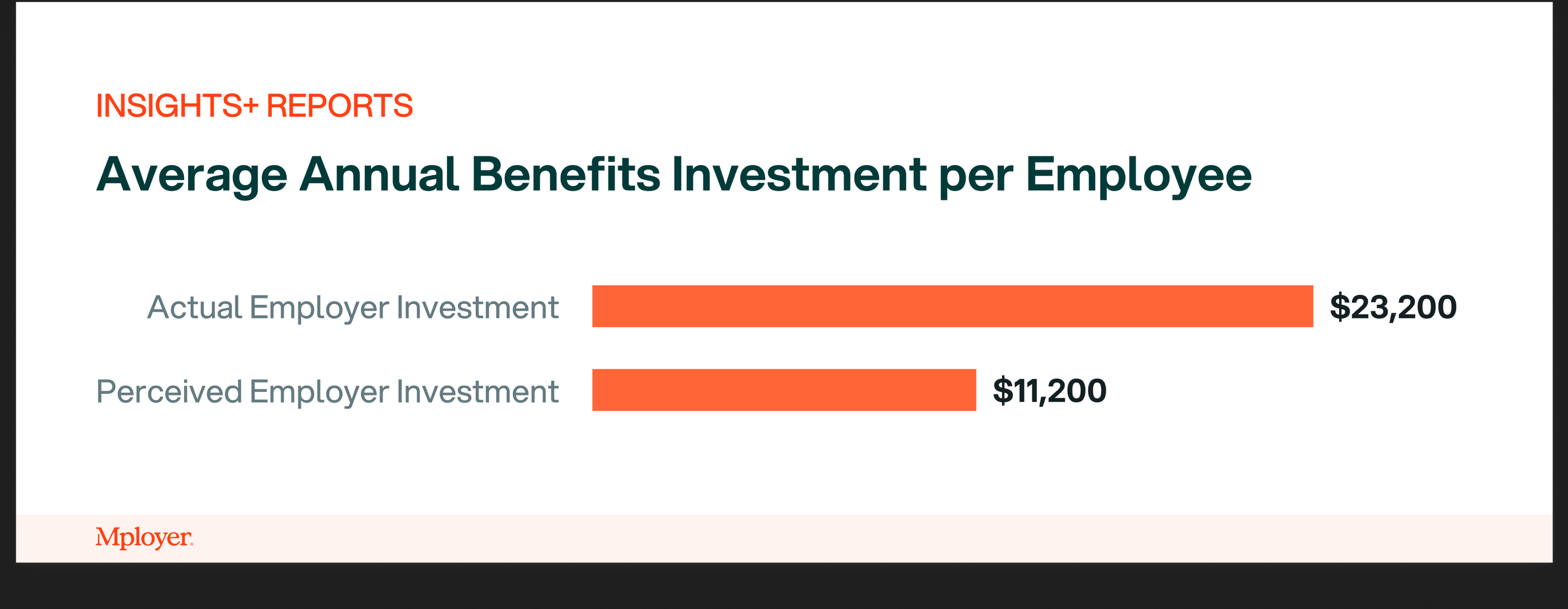

Most employees drastically underestimate the value of their benefits—valuing them at $11,200 on average vs. a true value of $23,200

Employers lack a clear, credible way to showcase the value of their benefits or compare against the market

Proving you offer competitive benefits lead to lower voluntary turnover, shorter time to fill roles, and a 9X increase in quality applicants

Mployer’s Insights+ platform uses a proprietary, data-backed scoring methodology to benchmark your benefits across the four core pillars of employee benefits – medical, ancillary, leave and retirement

With access to the largest benchmarking dataset in the industry, Insights+ enables custom cohort comparisons and ratings by your by industry, region, and size

To see how your benefits compare to companies just like you, reply and let us know

The Perception Gap: Why Competitive Benefits Are a Strategic Advantage

Ask any employer if they offer competitive benefits, and you’ll likely get an awkwardly confident “yes.” But dig a little deeper—compared to who? Based on what? That’s where things break down immediately.

The reality is: employee benefits today are judged almost entirely based on perception, not proof.

Employees, on average, believe their benefits are worth about $11,200. In truth, employers are investing nearly $23,200 per employee per year per Mployer’s Insights+ 2025 study across companies representing over 1M employees. That’s a massive gap in perceived value—and one that significantly undermines retention, recruiting, and engagement.

When you can prove that your benefits are competitive—not just internally, but compared to your true market—you unlock a measurable strategic advantage:

Lower voluntary turnover

Faster time to fill roles

9X improvement in qualified applicants

But proving benefit competitiveness takes more than guesswork or gut feel. That’s why we built Insights+—a first-of-its-kind platform that turns perception into data-backed proof.

Introducing Insights+: The Industry Standard for Benefits Benchmarking

At Mployer, we’ve spent years building Insights+ in partnership with the top insurance brokerages in the country. It’s the most advanced, statistically accurate benchmarking system on the market, designed to give employers a true understanding of their benefits competitiveness.

Here’s how it works:

We ingest your benefits guide or a quick intake form

Our engine scores your plan across four core components (more on that below)

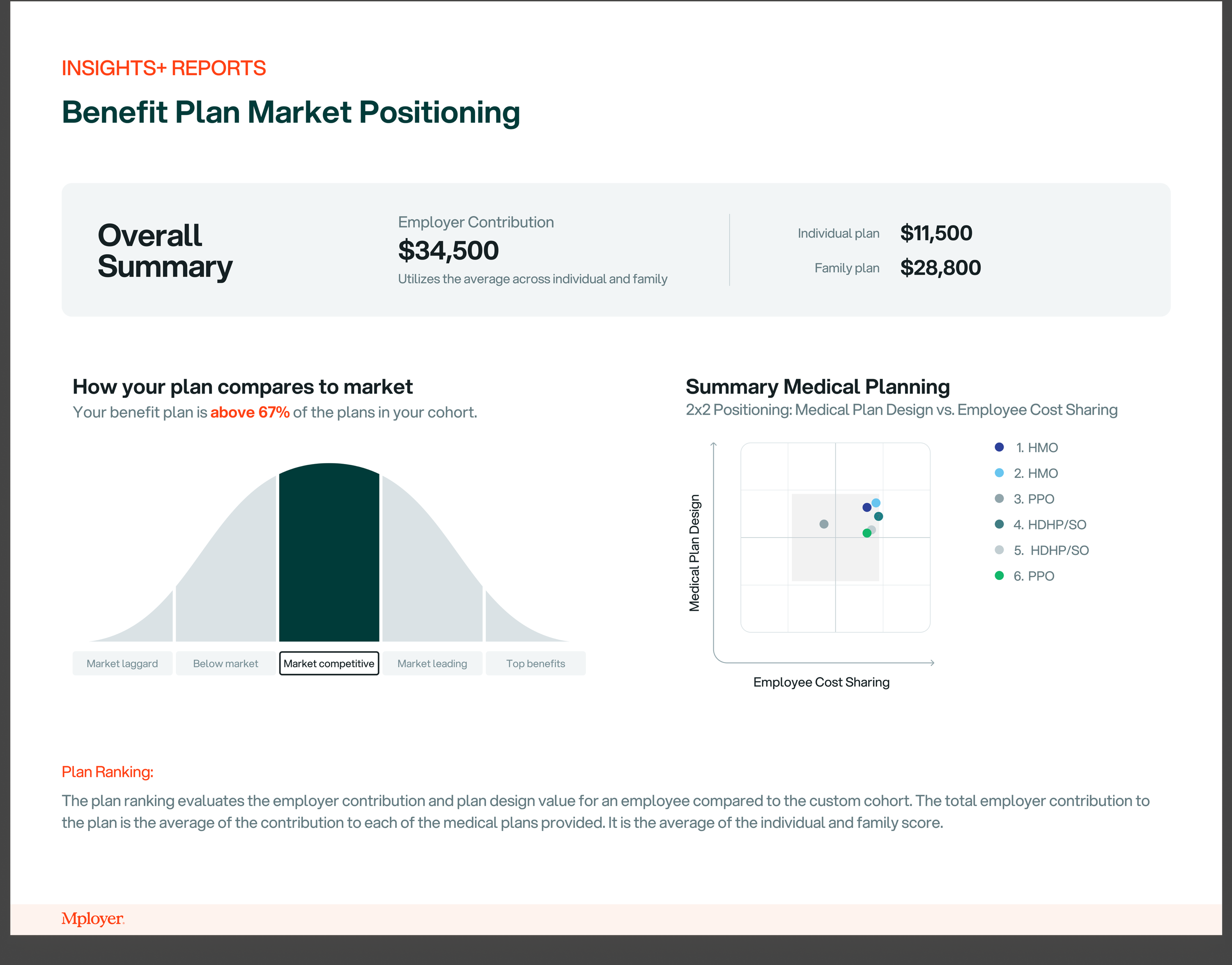

We benchmark your plan against a custom peer group of employers like you, same industry, region and size —not a generic industry average.

You receive a full report and rating that you can share with your team, inclusive of:

An overall rating (it’s pretty great)

Strengths, weaknesses, and gaps

Comparison vs. peers on spending and participation

Plus, if your score ranks highly—you receive a recognition toolkit with ready-to-use materials for employee education, recruiting, and brand positioning

This isn’t a one-size-fits-all solution. It’s a proprietary methodology built on a 30,000+ employer dataset, kept current through direct employer uploads, broker partnerships, and more.

How We Score Benefits: The Four Core Components

Competitive benefits can’t be measured by a single number like "how much you spend" or whether you offer a 401(k). It takes a holistic view—and that’s what our four-pillar scoring system does.

These are the four foundational categories we use to assess the true competitiveness of a plan:

1. Medical

This includes everything from your monthly premiums to deductible levels, plan options, and employer contribution percentages. It’s typically the most expensive part of your benefits package—and the most scrutinized by employees. We evaluate depth of coverage, choice, affordability, and access and compare your plan to your cohort.

2. Ancillary

Dental, vision, disability, life and voluntary insurance fall here. Our methodology weighs plan richness, employer contribution for each individual line item. While often considered secondary, ancillary benefits play a big role in perceived value—and they’re a low-cost lever for improvement.

3. Leave

PTO, holidays, parental leave, and—critically—flexibility (remote, hybrid, compressed schedules). We evaluate not just what's offered, but how it compares to market expectations within your peer group. Leave policies are increasingly make-or-break in competitive industries.

4. Retirement

401(k), 403(b), ESOPs, and other savings mechanisms. We assess both participation structures (e.g., automatic enrollment, matching formulas) and actual dollar contributions compared to peers.

Our scoring system blends employee perception, plan design, cost, and participation data to generate a truly holistic and market-relevant evaluation.

No other system in the industry brings this level of depth, customization, and credibility. Want to see how you compare? Let us know.

Benchmarking Against a Custom Peer Group

Forget comparing yourself to national averages or sample data from a survey two years ago. With Mployer, you benchmark against a precisely matched peer group.

We offer the largest and most granular dataset in the industry, covering over 30,000 employers and growing. This enables you to compare your benefits offerings against statistically valid cohorts based on:

30+ Industries (from healthcare to logistics to tech)

8 Organization Sizes (from <25 employees to 10,000+)

8 U.S. Regions (ensuring geographic relevance)

Only with us can you create a peer group so tailored that it mirrors your recruiting market, reflecting what companies like yours—and hiring for the same roles—are doing.

Whether you’re a manufacturing firm in Ohio or a startup in Austin, your competitive landscape looks different. We ensure your comparison group matches reality, not abstraction.

Competitive Benefits as a Strategic Advantage

We say it often because it’s true: benefits are more than a cost center—they’re a strategic asset.

When your benefits are perceived as strong, you get:

More applicants (especially the ones you actually want)

Fewer people leaving for marginal improvements elsewhere

Stronger employee engagement and satisfaction

But all of that starts with knowing how you compare—and having the data to back it up.

Insights+ doesn’t just show you where you stand. It gives you the tools to improve, the proof to showcase what you already do well, and the recognition materials to ensure your benefits investment is seen and appreciated by the people who matter.

See How Your Benefits Stack Up

If you’re ready to move beyond guesswork and prove that your benefits are truly competitive, Insights+ is your next step.

You’ll get:

A customized, data-backed Benefits Competitiveness Score

Insights into where you're ahead or behind the curve

Benchmark comparisons across size, region, and industry

A recognition kit if you score well—complete with messaging tools, badges, and recruiting assets

Best of all? It’s free for employers to get started.

Let us show you what great benefits really look like—on paper, in practice, and in perception.

Editor's Note: This report is based on survey data from April 2025 that was published in May 2025. This is the most recent data available. (Source: Bureau of Labor Statistics)

The job market once again proved to be more resilient than economists were predicting, with US employers adding 177 thousand jobs over the course of April as the unemployment rate held steady at 4.2%.

That figure of 177 thousand new jobs significantly exceeds the approximate 135 thousand new jobs that economists had forecast and is on par with the prior month’s ultimate report of 185 thousand new jobs (revised down from an initially-reported and headline-grabbing 228 thousand new jobs).

The number of long-term unemployed people rose by about 180 thousand to reach 1.7 million people, which is an increase of almost 12%. Long-term unemployed people - those who have been out of work but seeking it for 27 weeks or more - account for almost one-quarter of all unemployed people. Long term unemployment has increased by more than one-third over the last 12 months, up from about 1.25 million in April of 2024.

There was little change across most other metrics over the course of the month, however, with the employment population ratio (60%), labor force participation rate (62.6%), the number of people working part time for economic reasons (4.7 million), and the number of people who want a job (5.7 million) all essentially holding steady over the month.

Of the 177 thousand net jobs added last month, the healthcare industry was responsible for the largest proportion, adding 51 thousand jobs over the course of April, which is just below the 52 thousand net new payroll entries averaged each month over the last 12.

The transportation & warehousing industry had the next largest net job increase in April, increasing its ranks by abou 29 thousand, with the financial activities industry and the social services industry claiming the addition of 14 thousand net employees and 8 thousand net employees, respectively, as well.

While there was no significant change over the month in most other industries, federal government employment did register a noteworthy drop of 9 thousand employees, bringing the total number of net federal jobs lost in 2025 to 26 thousand, although that figure does not represent the entirety of the situation - more on that to come.

Average hourly pay rose by about 6 cents to an even $36.06 per hour (an increase of 0.2%) over the month while the increase was about 3.8% over the last year - up from $34.67 per hour for privately employed, non-farm workers.

The length of the average workweek grew slightly over the month to 34.3 hours per week.

Mployer’s Take

The headline story from the jobs report is the continued strength of the labor market even in the face of economic forces like the threat and/or implementation of sweeping global tariffs, but the labor market alone does not tell the entire story of the economic moment.

For one, the federal workforce reductions instituted by Elon Musk’s Department of Government Efficiency may be 10 times larger than the 26 thousand jobs that have so far registered in this data, but those numbers won’t show up until those employees severance/leave pay has expired.

Even more importantly, the GDP dropped by .03% through the first 3 months of 2025, which is the first contraction of GDP in 3 years, and while looming tariffs and federal firings were certainly contributors, those factors are more likely to have an increasing influence over the economy as a whole in the coming months than a decreasing influence.

Still, despite the lag in capturing federal employees whose jobs were recently terminated in these data sets and despite the uncertainty surrounding both the tariffs and their impact, this jobs report indicates that employers are still carrying on hiring, which itself is a kind of vote of confidence for the continued resilience of the US economy.

Further, inflation is up only 2.3% from last year and the rate of increase is trending downward, which is another positive sign, yet many economists (and employers) remain pessimistic about our chances for avoiding economic downturn in the months ahead.

The Federal Reserve will soon be facing the decision again about what to do with interest rates, and although inflation is nearing the Fed’s stated target of 2% annualized inflation, in light of the potential inflationary pressure that tariffs are capable of producing, the Fed may be less eager to lower interest rates now than they otherwise may have been given the current inflation levels.

We’ll know more about the Fed’s short term plan for interest rates in just a couple days, but we are still a ways off from knowing the ultimate impact of tariffs and federal workforce restructuring.

In light of the first quarter economic contraction, however, and in light of the fact that economic recession can be defined as two consecutive quarters of negative GDP growth, it’s entirely possible that the current economic conditions are retroactively labeled as a recession as soon as July, even with the labor market still humming along.

Each month, Mployer collects and presents some of the most relevant and most pressing recent changes in law, compliance, and policy in areas related to employee benefits, health care, and human resources.

I-9 Form Update

US Citizenship and Immigration Services released a new I-9 form on April 2, 2025. Some of the updates include replacing the word “non-citizen” with “alien” and the word “sex” has replaced “gender.”

The previous I-9 forms - released on August 1, 2023 - remain valid until their listed expiration dates, in 2026 and 2027, respectively.

Tennessee: As of April 11, 2025, employers in Tennessee are required to pay out all owed earnings in the event of an employee’s death. Previously, Tennessee employers could cap those payments at $10,000. You can read more here.

Washington: Beginning June 27, 2025, employees in Washington state will be permitted to use sick leave in order to address immigration-related issues. You can read more here.

The Washington state legislature has also updated several laws governing when minors are allowed to work, employee protections, health care worker rest breaks, and workplace safety measures in certain industries. You can find those bills here, here, here, and here, respectively.

Beginning July 27, 2025, Washington employers will no longer be able to require that employees have driver’s licenses unless driving is part of the job function and/or central to a legitimate business purpose. You can read more here.

As of May 1, 2025, minimum wage in the city of Bellingham, Washington increased to $18.66 per hour. You can read more here.

Wisconsin: The Wisconsin Supreme Court ruled that state laws that protect job candidates and workers from arrest-record discrimination also apply to non-criminal offenses like civil violations. You can read more here.

Colorado: Beginning July 1, 2025, Colorado employers that collect biometric data (e.g. fingerprints, retina scans, etc.) from employees and/or job candidates must follow the expanded guidelines laid out in the Colorado Privacy Act, which include implementing a written policy addressing biometric collection protocol and obtaining consent for the collection of biometric data. You can read more here.

Beginning February 1, 2026 Colorado employers that use artificial intelligence to evaluate employees and job applicants will be required to take proactive measures to ensure that those platforms are not enabling discriminatory practices. You can read more here.

Massachusetts: Employers with more than 50 employees must post the new veterans services poster that was just released by the Massachusett Executive Office of Labor and Workforce Development. The poster must be conspicuously displayed in an area that is accessible to all employees. You can find the poster here.

New York: As of March 2, 2025, all New York employers are prohibited from requiring job applicants to provide a copy of their criminal history record, which closes a loophole employers had been exploiting to obtain such records despite restrictions regulating their access to those records.

As of March 22, 2025, all New York employers regardless of size are prohibited from requiring job applicants or employees from providing a copy of their criminal history report that was obtained via the New York State Division of Criminal Justice Services.

Beginning May 8, 2025, NY employers with more than 3 employees must conspicuously post their lactation room accommodation policies and guidelines as well as the relevant state requirements both somewhere accessible by all employees and on the organization's intranet if applicable.

Beginning June 2, 2025, employers with 10 or more retail employees must have in place a written policy and training program for violence prevention measures and retail employers with 500 or more employees must install and/or maintain silent response buttons to alert authorities about emergencies. This legislation was originally slated to take effect March 4, 2025, But was amended to clarify employer responsibilities.

Further, as of January 1, 2025, New York employers are required to provide 20 hours of paid prenatal leave during a 52 week period. Also, as of the new year, the characteristics to which equal protection was extended via the New York State Human Rights Law and the resulting protections are formally enshrined in the New York State Constitution. Those characteristics include: age, disability, ethnicity, gender identity, gender expression, national origin, pregnancy, and anything else related to reproductive healthcare.

Oregon: As of January 1, 2025, Paid Leave Oregon provides leave for employees completing necessary legal steps associated with adopting and/or fostering children.

Minimum Wage For Federal Contractors Rescinded

On March 14, President Trump rescinded Executive Order 14026 - which Biden signed in 2021 and raised the minimum wage for federal contractors from $10.10 per hour to $15 per hour with mechanisms contained within the order to continue increasing this wage minimum over time.

On January 1, 2025, in accordance with EO 14026, the minimum wage for federal contractors increased to $17.75 per hour, but now that Trump has rescinded EO 14026, it is unclear what the current minimum wage for federal contractors is.

Alternative Manner For 1095-B & 1095-C Distribution

If your organization is using the alternative method for distributing 1095-B and 1095-C forms in accordance with the Paperwork Burden Reduction Act, your website must be in compliance from the first business day of March through at least October 15th. You can find guidance from the IRS about how to properly follow compliance protocols here.

DEI Executive Orders Paused

On February 21, 2025, a federal judge put a stay on Trump’s Executive Order limiting the ability of federal agencies and federal contractors to operate Diversity Equity and Inclusion programs. The court questioned whether the order violated free speech rights and potentially illegally restricted otherwise legal actions taken by private entities. You can find the decision here.

Form 300A Submission Due

From February 1st to April 30th, non-exempt (low hazard) employers who had at least 11 employees at some point in 2024 must post in a conspicuous place a copy of OSHA Form 300A, Summary of Work-Related Illness and Injury, certified by a company executive.

For non-exempt employers that had 250 or more employees at some point last year and employers with 20 or more employees in specified high risk industries, OSHA requires electronic submissions, which are due by March 2nd, 2025.

In his first days since returning to office, President Trump signed a series of executive orders dealing with labor and employment issues for federal employees and federal contractors, with more expected still to come.

While thus far these orders don’t apply to private employers in general - with the exception of those that accept federal funds and/or are federal contractors - these orders will not only affect a sizeable portion of the workforce directly, but they will also likely inspire some private employers to modify their practices and follow the example set by the executive branch.

The new rule that will most likely have the largest impact beyond the sphere of federal employees is Executive Order 11246, which makes it so that federal contractors no longer have to practice affirmative action in the hiring process for most protected classes. The only protected classes excepted from the order are veterans and individuals with disabilities, for whom affirmative action standards still apply.

Although federal contractors will no longer be required to maintain affirmative action programs, Title VII of the Civil Rights Act remains in effect to prevent discrimination against protected classes like race, gender, sexual orientation, and national identity.

A Federal District Court Judge in Northern Texas ruled that American Airlines had breached its fiduciary duty by working with an investment manager that promoted ESG practices in a way that ran counter to the economic interests of the employee retirement fund beneficiaries.

The repercussions of this ruling could be industry-reshaping if upheld, although there were many additional conflicts of interest between American Airlines and their investment fund manager that may limit how broadly applicable the ruling will ultimately prove to be.

The judge has already found American Airlines in breach of their fiduciary duty, but he has yet to assess damages, which will influence the probability of appeal and the likelihood of copycat cases.

As of January 13, 2025, the extension period for certain renewal Employee Authorization Document (EAD) applications filed on May 4, 2022 or later has been formalized at 540 days.

As of January 1, 2025, the IRS mileage reimbursement rate for road miles driven for business purposes increased by 3 cents per mile from 67 to 70 cents per mile driven.

PCORI Fee Increase

The IRS released a statement announcing a 25-cent increase in Patient-Centered Outcomes Research Institute fees for covered plan years ending on or after October 1, 2024, and before October 1, 2025.

In response to a Federal Court of Appeals Decision that vacated the so-called 80/20/30 rule that was instituted in 2021, the Department of Labor officially reverted to the previous tip credit rule.

As of January 1, 2025, the threshold for what qualifies as affordable coverage is now 9.02%, which means that an employee’s required contribution to the plan can be no more than 9.02% of their salary in order for the plan to be considered affordable and to avoid potentially paying the penalty.

You can read more about the affordability threshold here.

EAP & Highly Compensated Exception Update

A federal court in Texas determined that the Department of Labor exceeded its authority last summer by increasing the minimum pay thresholds for employees to qualify under the executive, administrative, and professional and highly-compensated employee exceptions to minimum wage and overtime protections.

Those minimum pay thresholds have reverted to their prior levels - back to $684 per week for the EAP exemption (down from $844 per week under the now defunct rule), and back to $107,432 per year for the HCE exemption (down from $132,964 per year under the now defunct rule).

NLRB Says No Captive Audience Meetings on Unionization Issues

The National Labor Relations Board has issued a decision prohibiting employers from forcing employees under threat of punishment to attend meetings during which the employer will share views on unionization or its impacts.

Employers are allowed, however, to convene employees and share their views on unionization and potential impacts so long as employees are not disciplined or adversely affected in any way for not attending (or leaving early). Employers should not even keep or maintain such attendance records.

IRS Publishes 2025 Annual Retirement Plan Maximums

The 401(k) annual contribution limit increased from $23,000 to $23,500 in 2025.

The catch-up contribution limit stayed unchanged at $7,500 for participants aged 50 and over.

The SECURE Act 2.0 also instituted a new type of catch-up contribution, which enables participating people (age 60 to 63) to contribute up to $11,250 annually.

The HFSA contribution max is $3,300 (maximum carryover is $650 for HFSAs with carryover features).

The QSEHRA max for total reimbursements is $6,350 for single coverage and $12,800 for family coverage.

The max employee tax credit for adoption assistance is $17,280, with additional conditions depending on employee salary range.

The monthly parking and mass transit benefit max is $325.

You can find the complete IRS 2025 benefit contribution limit list here.

ERISA Guidance for Long-Term Part-Time Employees

You can find guidance for ERISA 403(b) plan eligibility requirements for long-term, part-time employees according to the updated standards from the Secure ACT 2.0 here.

Nearly 9 out of 10 employers relied upon stop-loss insurance to cover a high-cost claim between 2029 and 2022.

The price of high-cost treatments was up 4.4% over the year in 2024, climbing to an average expense of about $421 thousand per claimant.

High-cost claimants typically make up less than 2% of plan membership but cost almost 30 times more than the average plan member, but there are many steps employers can take to better control costs associated with the most expensive conditions and treatments.

ARTICLE I Employers’ Guide to Controlling High-Cost Healthcare Treatments & Conditions

Rising costs have been a chronic condition of the US healthcare system for decades, with out-of-pocket expenses adjusted for inflation approximately doubling over the last 50 years.

Given that employers have largely been bearing the brunt of these increases while covering between about 67% and 85% of employee and employee family healthcare costs depending on the plan, it is especially understandable why many employers have been expressing an increasing urgency to get these costs under control.

As is often the case, however, better controlling healthcare costs is a task much more easily said than done, but one often overlooked place to find savings is improved management of particularly high-cost conditions, procedures, and pharmaceuticals, which are eating up an increasing proportion of employer healthcare budgets but also provide an opportunity for employers to make small changes that can have big, positive impacts on their bottom line.

According to data from Sun Life, between 2019 and 2022 there was an 87% chance that an employer would encounter a claim so expensive that it exceeded the threshold triggering stop-loss insurance in any given year.

According to the National Alliance of Healthcare Purchaser Coalitions, the cost of high-cost treatments was up 4.4% over the year in 2024, climbing to an average expense of about $421 thousand - an average that is in part inflated by extremely high-cost new treatments/technologies (i.e. ~$7 million gene therapy) as well as the longevity-increasing impacts of improved treatments/technologies that can abate chronic conditions over longer periods of time (e.g. $60 thousand per month cancer drugs).

Historically, only 1.2% of plan members are high-cost claimants, but they cost about 29 times more than the average plan member, amounting to an average annual expense per high-cost claimant of about $122 thousand.

Over the last 4 years, the conditions that have resulted in the greatest number of high-cost claims include malignant neoplasm, cardiovascular system issues, cancer, prenatal/neonatal care, musculoskeletal problems, respiratory issues, sepsis, gastrointestinal conditions, neurological problems, and urinary/kidney diseases.

The list grows even smaller when looking at the types of conditions/treatments responsible for the largest number of $1 million plus claims, such as sepsis, cancer, prenatal/neonatal, and cardiovascular disease.

Cancer:

Cancer is one of the most complex diagnoses, often requiring coordinated care from a number of different providers.

Improved cancer-fighting treatments can significantly increase longevity but also come with significantly increased costs, improving the relative ROI for prevention.

How can Employers reduce cancer-related costs?

Invest in cancer prevention efforts by prioritizing and rewarding both healthy lifestyle behaviors and early cancer screenings.

Offer employees help coordinating care and navigating the often confusing healthcare system by supplying case management assistance.

Consider exploring various new initiatives and cancer treatment pilot programs in order to determine which approach or approaches may be best for a given patient and/or type of cancer.

Standardize obtaining second diagnoses to limit the incidence of misdiagnosis.

Sepsis:

Sepsis kills more in-patients in a hospital than any other affliction and hospital-acquired sepsis is one of the most preventable of the high-cost conditions.

For every hour that medical attention is delayed, the survival rate for sepsis decreases by 7.6%.

How can Employers reduce sepsis-related costs?

Educate employees about risk-reduction prevention and symptom identification.

Push healthcare system touchpoints to improve infection transmission protocols.

Collect & analyze claims data to identify patterns and improve prevention/minimization efforts.

Prenatal/Neonatal Issues:

More than 1 out of 10 births in the US are premature, which increases total healthcare costs by more than $26 billion each year.

Premature births can result in costs exceeding $600 thousand per baby and there is very little that can be done to promote prevention beyond the status quo.

How can Employers reduce prenatal/neonatal-related costs?

Utilize regular care management and hospital audits to ensure billing accuracy.

Provide managed fertility benefits to limit unwanted multiple births which have higher associated risks and costs than single births.

Reduce costs through bundling maternity monitoring services and optimizing NICU utilization management.

Cardiovascular Disease:

Between 2020 and 2050 the risk factors associated with cardiovascular disease are expected to triple, and more than 1 in 3 US adults have already received care for a cardiovascular risk factor.

The cost of cardiovascular disease to the US health system over that time frame is expected to increase from about $3.9 billion to $1.4 trillion - more than quadrupling over that 3-decade span.

How can Employers reduce cardiovascular disease-related costs?

Conduct work-site blood pressure screenings.

Encourage and reward heart-healthy lifestyle behaviors.

Educate employees about symptoms of cardiovascular conditions as well as measures to prevent the onset of some heart problems in order to improve early detection to limit their occurrence.

Gene Therapy:

Heart Disease, cancer, and blood conditions like hemophilia are among the many ailments that emerging gene therapies are being utilized to treat.

Costs for many gene therapy procedures are heavily frontloaded as these treatments are often one-time events.

How can Employers reduce gene therapy-related costs?

Consider that many insurance carriers are reducing coverage for some rare diseases by adding conditional waivers for some conditions, as well as warranties, amortized payment schedules, and per-member per-month fees.

Consult an experienced benefits broker to become educated about the latest gene therapies to confirm the efficacy and necessity of such treatments.

Other High-Cost Specialty Drugs:

Specialty drugs account for more than 40% of net payer prescription costs.

Increasing competition for current biologic drugs will see increasing competition from generic and biosimilar drugs which will help keep costs down for employers and benefits managers who stay current.

How can Employers reduce specialty-drug-related costs?

Some employers are managing specialty drug costs by reducing access to them in the formulary, while other employers are addressing the challenge by instituting employee assistance programs for drug expenses that exceed a certain threshold (e.g. $5 thousand).

Monitor internal and external data to ensure the right patient receives the right dosage of the right drug at the right time in the right place at the right price.

Consider alternative strategies like contracting with drug manufacturers directly and evaluating less-costly medication options and or treatment facilities (e.g. facilitating in-home infusion over more expensive hospital infusion when possible).

There is little doubt among either experts or casual observers that there are systemic issues within the US healthcare system that will require system-wide solutions.

Individual employers - even those of substantial size - only have so much influence over rising healthcare costs that often seem more akin to a runaway train car than a properly functioning public and private health network.

Too often, however, employers misconstrued this limited control as though it were no control, which is when the train really starts picking up enough speed to jump the tracks.

In reality, there are many things that employers can be doing to exercise greater cost controls over their healthcare expenditures - and that is especially true for the highest-cost ticket items.

While employers historically have depended on the assistance of third-party administrators and pharmacy benefit managers to handle claims above a certain threshold, with these costs continuing to climb and no systemic relief currently in sight, forward-looking employers might be wise to take a more proactive approach in holding service providers to account and exploring cost-sharing approaches that don’t compromise quality of care.

There is no one solution to the high-cost claim issue, nor is there a one-size-fits-all solution that can be replicated and reapplied from one high-cost claim to the next, but there are many solutions - often starting with better data collection - that together can be form-fitted to cover the high-cost claim exposure of any given employer that recognizes the value of doing so, which will be an increasing number of employers as net costs for high-cost treatments keep rising.

Editor's Note: This report is based on survey data from March 2025 that was published in April 2025. This is the most recent data available. (Source: Bureau of Labor Statistics)

US employers added 228 thousand jobs last month, far outpacing economic forecasts that predicted about 140 thousand new jobs.

At the same time, the national unemployment rate ticked up to 4.2% - an increase of 0.1% - which is a minor lift, although 4.2% matches the highest the US unemployment rate has been since October 2021 when the US was still recovering from the pandemic-induced unemployment spike.

Since November 2021, this report represents only the third time that US unemployment has hit 4.2%, the first of which was July 2024 followed by November 2024.

The labor force participation rate rose by one-tenth of a point from 62.4% to 62.5%, while the employment population ratio held steady at 59.9%, which is the third time this figure has been below 60% since November 2022.

After an 11% spike last month in the number of people employed part-time for economic reasons, that figure has come down significantly from about 4.94 million to 4.78 million, representing a reduction of about 160 thousand people - although this subset of the population has seen substantial growth over the last 12 months, increasing by about 11% in total.

The 228 thousand jobs added last month amount to an increase of almost 45% over the 155 thousand jobs added in the US on average in each of the last 12 months, further underscoring the resilience of the labor market even as it has cooled over the past year.

The healthcare industry added the largest number of new payroll entries last month with about 54 thousand jobs - just over the 52 thousand monthly average healthcare job additions over the last year.

The social assistance industry also had a strong month, adding 24 thousand jobs for an increase of more than 26% over the 19% monthly average recorded over the previous 12 months.

Further, retailers added 24 thousand jobs last month, in part due to more than 20 thousand food and beverage workers returning to the job post labor strike, and the warehousing and transportation industry added a comparable 23 thousand jobs as well, which is almost a 92% increase.

The only industry to see a workforce reduction over the last month is the government, which fell by about 4 thousand workers, driven by a decrease of 11 thousand federal workers - although the loss of federal workers substantially undercounts the number of recent terminations conducted by the Department of Government Efficiency under Elon Musk that have not yet been captured by these surveys.

Average hourly pay rose by about 9 cents to an even $36 per hour (an increase of 0.3%) over the month while the increase was about 3.8% over the last year - up from $34.67 per hour for privately employed, non-farm workers.

The length of the average workweek saw no significant movement over the month at 34.2 hours per week.

Mployer’s Take

This report represents only the second set of complete monthly data collected under the second Trump administration.

With most incoming administrations, the first 100 days often moves at a frenetic pace as the new office-holder implements a number of policy changes that depart from those of their predecessor, and Trump’s latest stretch occupying the White House has been no different in that regard.

While many of the early actions undertaken since Trump was re-sworn in were focused on deregulation, deportation, and decreasing the size of the federal workforce, with just a few weeks left in the first 100 days of his second term, Trump focused his attention on tariffs and used executive orders and emergency powers in order to impose import taxes on goods arriving from nearly every international trading partner the US has.

As we noted in the wake of last month’s employment situation report, many of the impacts of Trump’s early actions have yet to become overtly apparent in the labor market or economy at large as experienced by most Americans.

Those delayed effects are especially true for Federal layoffs which may exceed a quarter million workers based on some estimates, very few of which have shown up in the labor market data yet due to how these figures are counted and when.

Also, the Trump administration has been rehiring some inadvertently terminated personnel who work in sensitive areas like nuclear safety and infectious disease prevention, so the total number of federal employees who have lost their jobs in the last couple of months may still decrease.

That said, there are tens if not hundred of thousands of federal workers who are already or will soon be out of a job, and those results will certainly have an impact on the labor market, potentially increasing the number of unemployed people in the US by more than 3%, and that doesn’t account for all the complementary support jobs in the private sector that will be eliminated due to the smaller federal workforce.

It remains to be seen, of course, just how many jobs will be lost due to these cuts or what the broader economic and other impacts may be, and that will likely continue to be true for many months if not years to come.

All that to say, the delay and uncertainty surrounding the early actions of the second Trump administration will take some time to play out before the final outcomes can be known, and that is largely true for the latest tariff actions, as well - but the scale of the potential tariff-related repercussions may be much bigger, although, to be clear, those impacts are very much still in flux and subject to change as countries come to the negotiating table, reevaluate existing trade partnerships, and/or forge new ones.

After what Goldman Sachs described as the largest equity selloff in 15 years in just the first days since Trump announced and implemented this latest round of sweeping, global tariffs, the short-term economic impacts are likely to be considerably more pronounced than the short-term economic impacts caused by shrinking the federal workforce or disrupting the agricultural supply chain have been.

While the long-term impacts of these actions - especially the tariffs - will likely remain a subject of debate for years, there is much more agreement about the probable short-term impacts, which both supporters and opponents of the Trump administration believe will result in additional stress and strain on the US economy, leading to economic pain - the main questions are how severe it will be and for how long.

Each month, Mployer collects and presents some of the most relevant and most pressing recent changes in law, compliance, and policy in areas related to employee benefits, health care, and human resources.

Minimum Wage Increase For Federal Contractors Rescinded

On March 14, President Trump rescinded Executive Order 14026 - which Biden signed in 2021 and raised the minimum wage for federal contractors from $10.10 per hour to $15 per hour with mechanisms contained within the order to continue increasing this wage minimum over time.

On January 1st of 2025, in accordance with EO 14026, the minimum wage for federal contractors increased to $17.75 per hour, but now that Trump has rescinded EO 14026, it is unclear what the current minimum wage for federal contractors is.

Alternative Manner For 1095-B & 1095-C Distribution

If your organization is using the alternative method for distributing 1095-B and 1095-C forms in accordance with the Paperwork Burden Reduction Act, your website must be in compliance from the first business day of March through at least October 15th.

You can find guidance from the IRS about how to properly follow compliance protocols here.

DEI Executive Orders Paused

On February 21, 2025, a federal judge put a stay on Trump’s Executive Order limiting the ability of federal agencies and federal contractors to operate Diversity Equity and Inclusion programs. The court questioned whether the order violated free speech rights and potentially illegally restricted otherwise legal actions taken by private entities.

From February 1st to April 30th, non-exempt (low hazard) employers who had at least 11 employees at some point in 2024 must post in a conspicuous place a copy of OSHA Form 300A, Summary of Work-Related Illness and Injury, certified by a company executive.

For non-exempt employers that had 250 or more employees at some point last year and employers with 20 or more employees in specified high risk industries, OSHA requires electronic submissions, which were due by March 2nd, 2025.

In his first days since returning to office, President Trump signed a series of executive orders dealing with labor and employment issues for federal employees and federal contractors, with more expected still to come.

While thus far these orders don’t apply to private employers in general - with the exception of those that accept federal funds and/or are federal contractors - these orders will not only affect a sizeable portion of the workforce directly, but they will also likely inspire some private employers to modify their practices and follow the example set by the executive branch.

The new rule that will most likely have the largest impact beyond the sphere of federal employees is Executive Order 11246, which makes it so that federal contractors no longer have to practice affirmative action in the hiring process for most protected classes. The only protected classes excepted from the order are veterans and individuals with disabilities, for whom affirmative action standards still apply.

Although federal contractors will no longer be required to maintain affirmative action programs, Title VII of the Civil Rights Act remains in effect to prevent discrimination against protected classes like race, gender, sexual orientation, and national identity.

A Federal District Court Judge in Northern Texas ruled that American Airlines had breached its fiduciary duty by working with an investment manager that promoted ESG practices in a way that ran counter to the economic interests of the employee retirement fund beneficiaries.

The repercussions of this ruling could be industry-reshaping if upheld, although there were many additional conflicts of interest between American Airlines and their investment fund manager that may limit how broadly applicable the ruling will ultimately prove to be.

The judge has already found American Airlines in breach of their fiduciary duty, but he has yet to assess damages, which will influence the probability of appeal and the likelihood of copycat cases.

As of January 13, 2025, the extension period for certain renewal Employee Authorization Document (EAD) applications filed on May 4, 2022 or later has been formalized at 540 days.

As of January 1, 2025, the IRS mileage reimbursement rate for road miles driven for business purposes increased by 3 cents per mile from 67 to 70 cents per mile driven.

PCORI Fee Increase

The IRS released a statement announcing a 25-cent increase in Patient-Centered Outcomes Research Institute fees for covered plan years ending on or after October 1, 2024, and before October 1, 2025.

As of January 1, 2025, the threshold for what qualifies as affordable coverage is now 9.02%, which means that an employee’s required contribution to the plan can be no more than 9.02% of their salary in order for the plan to be considered affordable and to avoid potentially paying the penalty.

You can read more about the affordability threshold here.

EAP & Highly Compensated Exception Update

A federal court in Texas determined that the Department of Labor exceeded its authority last summer by increasing the minimum pay thresholds for employees to qualify under the executive, administrative, and professional and highly-compensated employee exceptions to minimum wage and overtime protections.

Those minimum pay thresholds have reverted to their prior levels - back to $684 per week for the EAP exemption (down from $844 per week under the now defunct rule), and back to $107,432 per year for the HCE exemption (down from $132,964 per year under the now defunct rule).

NLRB Says No Captive Audience Meetings on Unionization Issues

The National Labor Relations Board has issued a decision prohibiting employers from forcing employees under threat of punishment to attend meetings during which the employer will share views on unionization or its impacts.

Employers are allowed, however, to convene employees and share their views on unionization and potential impacts so long as employees are not disciplined or adversely affected in any way for not attending (or leaving early). Employers should not even keep or maintain such attendance records.

IRS Publishes 2025 Annual Retirement Plan Maximums

The 401(k) annual contribution limit increased from $23,000 to $23,500 in 2025.

The catch-up contribution limit stayed unchanged at $7,500 for participants aged 50 and over.

The SECURE Act 2.0 also instituted a new type of catch-up contribution, which enables participating people (age 60 to 63) to contribute up to $11,250 annually.

The HFSA contribution max is $3,300 (maximum carryover is $650 for HFSAs with carryover features).

The QSEHRA max for total reimbursements is $6,350 for single coverage and $12,800 for family coverage.

The max employee tax credit for adoption assistance is $17,280, with additional conditions depending on employee salary range.

The monthly parking and mass transit benefit max is $325.

You can find the complete IRS 2025 benefit contribution limit list here.

ERISA Guidance for Long-Term Part-Time Employees

You can find guidance for ERISA 403(b) plan eligibility requirements for long-term, part-time employees according to the updated standards from the Secure ACT 2.0 here.

State Updates

Colorado: On February 1, 2026 Colorado employers that use artificial intelligence to evaluate employees and job applicants will be required to take proactive measures to ensure that those platforms are not enabling discriminatory practices. You can read more here.

Massachusetts: Employers with more than 50 employees must post the new veterans services poster that was just released by the Massachusett Executive Office of Labor and Workforce Development. The poster must be conspicuously displayed in an area that is accessible to all employees. You can find the poster here.

New York: As of March 2, 2025, all New York employers are prohibited from requiring job applicants to provide a copy of their criminal history record, which closes a loophole employers had been exploiting to obtain such records despite restrictions regulating their access to those records.

As of May 8, 2025, NY employers with more than 3 employees must conspicuously post their lactation room accommodation policies and guidelines as well as the relevant state requirements both somewhere accessible by all employees and on the organization's intranet if applicable.

Beginning June 2, 2025, employers with 10 or more retail employees must have in place a written policy and training program for violence prevention measures and retail employers with 500 or more employees must install and/or maintain silent response buttons to alert authorities about emergencies. This legislation was originally slated to take effect March 4, 2025, But was amended to clarify employer responsibilities.

Further, as of January 1, 2025, New York employers are required to provide 20 hours of paid prenatal leave during a 52 week period. Also, as of the new year, the characteristics to which equal protection was extended via the New York State Human Rights Law and the resulting protections are formally enshrined in the New York State Constitution. Those characteristics include: age, disability, ethnicity, gender identity, gender expression, national origin, pregnancy, and anything else related to reproductive healthcare.

New York employers that receive criminal history records for applicants and employees must also now provide those applicants and employees with a copy of those records and a copy of the applicable New York corrections law as well as an opportunity to correct any inaccurate information that may be contained in those records.

Oregon: As of January 1, 2025, Paid Leave Oregon provides leave for employees completing necessary legal steps associated with adopting and/or fostering children.

Editor's Note: This report is based on survey data from February 2025 that was published in March 2025. This is the most recent data available. (Source: Bureau of Labor Statistics)

For two straight months now, US employers have added about 150 thousand new jobs according to initial reports, which is down slightly from the approximate 170 thousand new jobs added monthly over the past year, but not too far off track.

Despite those new payroll entries - only 3 states experienced net growth in total in-state jobs over the month, while the remaining 47 and Washington DC saw no significant change in payroll size.

The national unemployment rate ticked up one-tenth of a percentage point to 4.1%, but Florida was the only state that individually recorded a significant change in unemployment, climbing from 4.5% to 4.6% over the month.

Below is the breakdown of the Bureau of Labor Statistics’ (BLS) market employment summary from the March 2025 report.

States With the Highest Unemployment Rates

Nevada had the highest unemployment rate for the 4th month in a row, holding steady over the month at 5.8%.

California, Michigan, and Washington DC had the next highest unemployment rates at 5.4% each, followed by Kentucky at 5.3%, with Illinois at 4.8% rounding out the only 6 states with unemployment rates above the national average of 4.1%.

Florida was the only state to see an increase in unemployment rate over the last month, but over the course of the last 12 months, 30 months have seen unemployment rise, with the largest increases recorded by Michigan (plus 1.4%), Mississippi (plus 1.0%), and Colorado (plus 0.8%).

States With The Lowest Unemployment Rates

South Dakota - holding steady over the month at 1.9% unemployment - continued its streak of claiming the lowest unemployment rate in the country, which now stretches to 14 months.

North Dakota and Vermont shared the next lowest unemployment rate - both holding steady over the month at 2.6% - followed by Nebrask, New Hampshire, and Hawaii at 3%.

In total last month, 18 states had unemployment rates meaningfully lower than the US average of 4.1%.

Over the last 12 months, 30 states have recorded an increase in unemployment.

States With New Job Losses

No state recorded significant net job losses over the last month or over the last year.

States With New Job Gains

Missouri, New Jersey, and Ohio were the only states that recorded a net increase in payroll figures last month, growing by 0.4% each, amounting to increases of about 13 thousand, 19 thousand, and 23 thousand jobs, respectively.

Over the last 12 months, 17 states in total have recorded net job additions. The largest proportional gain was recorded in Idaho, which increased its workforce by 2.7% over that time frame, followed by South Carolina and Utah at plus 2% each.

Texas, Florida, and New York had the largest raw number of job gains over the past year at about 14 million, 10 million, and 10 million, respectively.

Mployer’s Take

This market summary represents a positive improvement over last month’s market summary which showed month-to-month net job losses across several states.

That said, while this data comes from the first full month of the second Trump administration, the economic impacts that will result from the policy changes that accompanied the transfer of power have not yet become apparent in these labor market reports.

It is difficult to pinpoint exactly how many federal workers have been laid off, which some observers claim added up to more than 60 thousand in February alone while the Department of Government Efficiency itself claims that figure is much smaller when voluntary retirements and resignations are taken into account.

Even less clear are the number of tangential private sector workers whose work is supported by federal employees and/or federal funding that may now be less available and/or less effective than it was in the past, so the secondary effects of federal workforce funding cuts are even further from having worked down the pipeline.

As a result, the holding pattern continues, and will likely continue for at least another couple of months as Trump wraps up the first 100 days of his second term in April - the period during which president’s are often most productive in executing their agendas.

Of course, there is no set deadline at which point the outcomes of these actions will be ultimately evaluated, and the effectiveness of some of those actions may well be a point of differing opinion well into the future.

But the early signs and indications about some of the near-term effects we can reasonably expect from the policy changes that have already been implemented may start to appear in the data as early as next month.

Editor's Note: This report is based on survey data from January 2025 that was published in March 2025. This is the most recent data available. (Source: Bureau of Labor Statistics)

Nearly 150 thousand jobs were added by US employers in February - the month when this data was collected - and the national unemployment rate fell by one-tenth of a point to 4%.

Looking at the state data, however, there was very little movement of significance in state unemployment levels, with the exception of Pennsylvania which recorded a 0.1% increase in state unemployment, rising from 3.7% to 3.8%.

Similarly, despite the net job additions, no state recorded a significant increase in payroll figures, but 4 states actually saw a reduction in in-state employment: Georgia, Missouri, and West Virginia, which all recorded a 0.6% decrease in employment, and Indiana, which recorded a 0.4% decrease.

Below is the breakdown of the Bureau of Labor Statistics’ (BLS) market employment summary for February 2025.

States With the Highest Unemployment Rates

For the third month in a row, Nevada had the highest unemployment rate, which is up slightly at 5.8%, followed by California at 5.4%, which is down from 5.5% the month before.

Washington DC, Kentucky, and Michigan all came in at 5.3% unemployment, but Washington DC is dropping while Kentucky and Michigan are seeing unemployment climb.

Illinois - at 4.9% unemployment - was the only other state above the national average of 4% during February.

Over the last year, 32 states have recorded an increase in unemployment, the largest of which was reported in Michigan, which saw its level of unemployment rise from 4.0% to 5.3% between January 2024 and January 2025.

Colorado and South Carolina also saw a significant increase in unemployment over the course of the last 12 months when both saw a 0.9% increase, while Mississippi and Wyoming fared nearly as poorly at plus 0.8% unemployment.

States With The Lowest Unemployment Rates

As we entered the new year, South Dakota held steady at 1.9% unemployment and continued its streak of maintaining the lowest unemployment rate in the country, which stretches for 13 consecutive months now.

North Dakota and Vermont had the next lowest unemployment levels at 2.6%, followed by Montana at 2.8% and Nebraska and New Hampshire at 2.9%.

17 states in total had unemployment rates below the national average.

Over the last 12 months, only Montana and Washington state have registered decreases in unemployment at 0.2% and 0.3%, respectively.

States With New Job Losses

Georgia had the largest net loss in jobs, recording a net decrease in its workforce of more than 28 thousand over the course of the month, which represents a 0.6% decrease.

Missouri and West Virginia each recorded workforce reductions of 0.6% as well, though the net job losses at minus 17 thousand and about minus 4 thousand, respectively, were much smaller than in Georgia due to their relatively smaller populations.

Indiana also saw a reduction in its workforce, which amounted to a drop of about 0.4% and amounted to a little less than 13 thousand jobs.

States With New Job Gains

No state saw statistically significant job gains over the month, although 17 states did record net increases in jobs over the last year.

Alaska and Idaho had the largest percentage gains in workforce size at plus 2.8% over the year, followed by Texas at 2.4% and Utah at 2.1%.

Texas, Florida, and New York saw the largest number of net new jobs over the last 12 months at about plus 14 thousand, 10 thousand, and 10 thousand respectively.

Mployer’s Take

Due to the timing of the latest state release from the Bureau of Labor Statistics, this report came out much later than usual relative to the collection of the data that the report is based on, and we’ll actually be getting updated data from the states by the end of the week at this point.

In fact, we’ve already seen follow-up data on the employment situation nationally, which showed the unemployment rate tick up by a tenth of a point despite the addition of another 150 thousand jobs to US payrolls.

On Friday when we get new state employment data again, it will likely look very similar to this set, although it will be interesting and informative to see which additional states start to see their unemployment rates moving in the wrong direction.

But in terms of the bigger picture, our analysis and the economy itself in many ways are in a holding pattern in the short term as the policy changes overseen by the new administration begin to manifest and the real-world impacts become more clear.

We’ll check in after the new data is made available later this week, and it’s possible there will be additional noteworthy developments between now and then - potentially including additional stock market volatility and/or new policy announcements - but barring major unforeseen developments, the next report will closely resemble this one.

It will take a bit more time before the full momentum and trajectory of the US economy can fully respond to policy changes that have already occurred - not to mention whatever additional changes may be in store - but we’ll be keeping an eye out in the meantime for noteworthy markers pointing toward what’s to come as they start to appear.

A significant number of major US corporations have been pulling back from Diversity, Equity, and inclusion (DEI) initiatives in recent months in response to perceived changes in political, regulatory, and social perception of these programs.

Target was an early torchbearer for the DEI cause but has since scaled back its DEI investment, and has been the subject of boycotts and/or lawsuits initiated by groups both supportive and opposed to DEI programs.

The principles of promoting diversity, equity, and inclusion in the workplace and the advantage of doing so long predate the DEI movement, and while some employers are distancing themselves from DEI language, the intra-organizational groups pursuing the underlying goals of DEI may continue doing so after being reorganized, restructured, and renamed in many cases.

Target and The Future of DEI

Diversity, Equity and Inclusion (DEI) programs experienced a rapid increase in stature followed by a near equally rapid rise in pushback over the last 5 years. Perhaps no company has felt that whiplash more than multi-category retail giant Target, whose experience provides an excellent case study to understand what has been happening with DEI policy as well as what will happen next.

Over the course of February 2025, Target found itself on the receiving end of a class action lawsuit brought by shareholders who claim Target’s pro-DEI policies led to significant losses of stock value, while at the same time, facing a targeted boycott led by pro-DEI supporters who aim to punish Target for rolling back some of those very same DEI policies that led to the class action suit.

If they were aiming to find themselves between a rock and a hard place, it looks like Target may have hit the bullseye.

While the momentum certainly appears to have shifted against DEI policies over the last couple of years, the coming months and years will likely be even more instrumental in determining the ultimate fate of the DEI movement and whether the accompanying programs will be retired, resurrected, or if they will simply be reorganized to continue the mission of promoting the principles of diversity, equity and inclusion under a different acronym.

Target and The Rise of DEI

The roots of modern DEI programs date back to the summer of 2020 when George Floyd was killed less than 10 minutes from Target’s headquarters in Minneapolis, and that proximity was a significant factor in inspiring Target to lead the way in mainstream corporate DEI adoption.

In response to that incident and the resulting movement which turned the spotlight around on systemic racism and other prejudice, Target pledged to establish a Racial Equity Action and Change committee, increase its proportion of black employees by 20%, and spend more than $2 billion dollars with black-owned businesses.

Of course, Target was not alone in joining the DEI bandwagon, with one McKinsey study estimating that companies worldwide spent about $7.5 billion on DEI-related expenditures in 2020, and as recently as early 2023 that figure was projected to double to $15.4 billion by 2026.

Over the course of 2023, however, DEI program adoption seemed to have hit a peak according to a study from Paradigm, which estimated that 54% of US companies budgeted for DEI program expenditures in 2023, which was down from 58% who had done so in 2022.

While the percentage of companies that had a specific DEI strategy fell by an even greater margin between 2022 and 2023 (minus 9%), 2023 wasn’t all bad news for DEI programs given that the percentage of US firms with senior DEI leadership roles increased by 6% over the year, and an additional 3% began tracking race representation in the lines of business of each of their executives.

2023 also happens to be the year in which most of the DEI-related activities and relevant events alleged in the class action suit against Target took place.

City of Riviera Beach Police Pension Fund vs. Target

On the last day of January 2025, the police pension fund for the city of Riviera Beach, Florida initiated a class action suit in federal court against Target claiming that Target’s DEI-related activities were a violation of the Securities Exchange Act.

According to the complaint, Target defrauded shareholders by failing to disclose the risks associated with their DEI (and ESG) mandates, which made Target’s share price artificially high as a result, so that anyone who purchased Target stock during the period of artificial inflation should be due compensation (August 26, 2022, through November 19, 2024).

The lawsuit alleges that those theoretical DEI risks became real losses in May 2023 when a boycott was staged against Target due to its Pride campaign, which resulted in a drop in stock price of almost 25% from the middle of May 2023 to the Middle of June 2023, as well as a 5% drop in sales during the second quarter of 2023, which caused another 15% stock price reduction when those sales figures were released in mid-August 2023.

Proceedings will continue in April 2025 after the notice period for potential lead plaintiffs to come forward has concluded.

New Pro-DEI Target Boycott Emerges

Exactly one week before the Riviera Beach police pension fund initiated its civil complaint in federal court, Target announced that it would be concluding its 3-year diversity equity and inclusion goals and would not be renewing its Racial Equity Action and Change initiatives.

The seemingly abrupt end of those programs was quickly followed by calls for a new boycott of Target, this time led by pro-DEI groups like the Racial Justice Network and churches, which has resulted in Target’s inclusion among a group of US companies that were subject to a 1-day blackout boycott on the last day of February 2025 and calls for an additional boycott of Target over the Lent holiday from March 5 through April 17, 2025.

In short, Target is still in the middle of the storm - the stock price has fallen by more than 18% in the time since the announced closure of these DEI programs and this writing (March 11, 2025), 15% of which occurred before the major market corrections of the past week - and the accompanying loss of sales won’t be reported until June when the stock price is likely to take another substantial hit depending on how effective, widespread, and lasting/repeated the boycotts are.

And Target is not the only company facing these boycotts and/or threats of boycotts, nor is it the only one backing away from previous DEI positions and commitments.

Corporate America and the Decline of DEI

Forbes constructed a timeline that documents how US companies have been responding to the changing DEI environment, which taken as a whole highlights just how quickly the momentum against DEI initiatives has developed.

In the spring of 2024, Harley Davidson ended some of its DEI-related activities. A few months later in mid-summer of 2024, John Deere announced that it would remove from company materials any messages that were socially motivated, and it would no longer support certain cultural awareness events like pride parades.

Over the next several months leading up to the 2024 election, several major corporations - including Lowes, Boeing, Coors, Ford, and Jack Daniels manufacturer Brown-Forman - followed suit and rolled back DEI initiatives in one way or another, ranging from no longer participating in diversity surveys to removing DEI-related goals, either as benchmarks for internal incentives or external suppliers.