.svg)

Key Takeaways

ARTICLE I Employers’ Guide to Controlling High-Cost Healthcare Treatments & Conditions

Rising costs have been a chronic condition of the US healthcare system for decades, with out-of-pocket expenses adjusted for inflation approximately doubling over the last 50 years.

Given that employers have largely been bearing the brunt of these increases while covering between about 67% and 85% of employee and employee family healthcare costs depending on the plan, it is especially understandable why many employers have been expressing an increasing urgency to get these costs under control.

As is often the case, however, better controlling healthcare costs is a task much more easily said than done, but one often overlooked place to find savings is improved management of particularly high-cost conditions, procedures, and pharmaceuticals, which are eating up an increasing proportion of employer healthcare budgets but also provide an opportunity for employers to make small changes that can have big, positive impacts on their bottom line.

While there is no set definition of where to draw the line between regular health insurance claims and high-cost claims, just about half of surveyed employers (44%) define high-cost claims as those that cost $100 thousand or more.

According to data from Sun Life, between 2019 and 2022 there was an 87% chance that an employer would encounter a claim so expensive that it exceeded the threshold triggering stop-loss insurance in any given year.

An even greater proportion of employers (94%) expect to see an increase in high-cost claims over the next 3 years and 84% view high-cost treatments as a threat to their business, which are reasonable forecasts given that the number of health plan claims of $3 million or more than doubled between 2016 and 2020, and that was before the healthcare system absorbed the COVID shock and the associated spike in inflation.

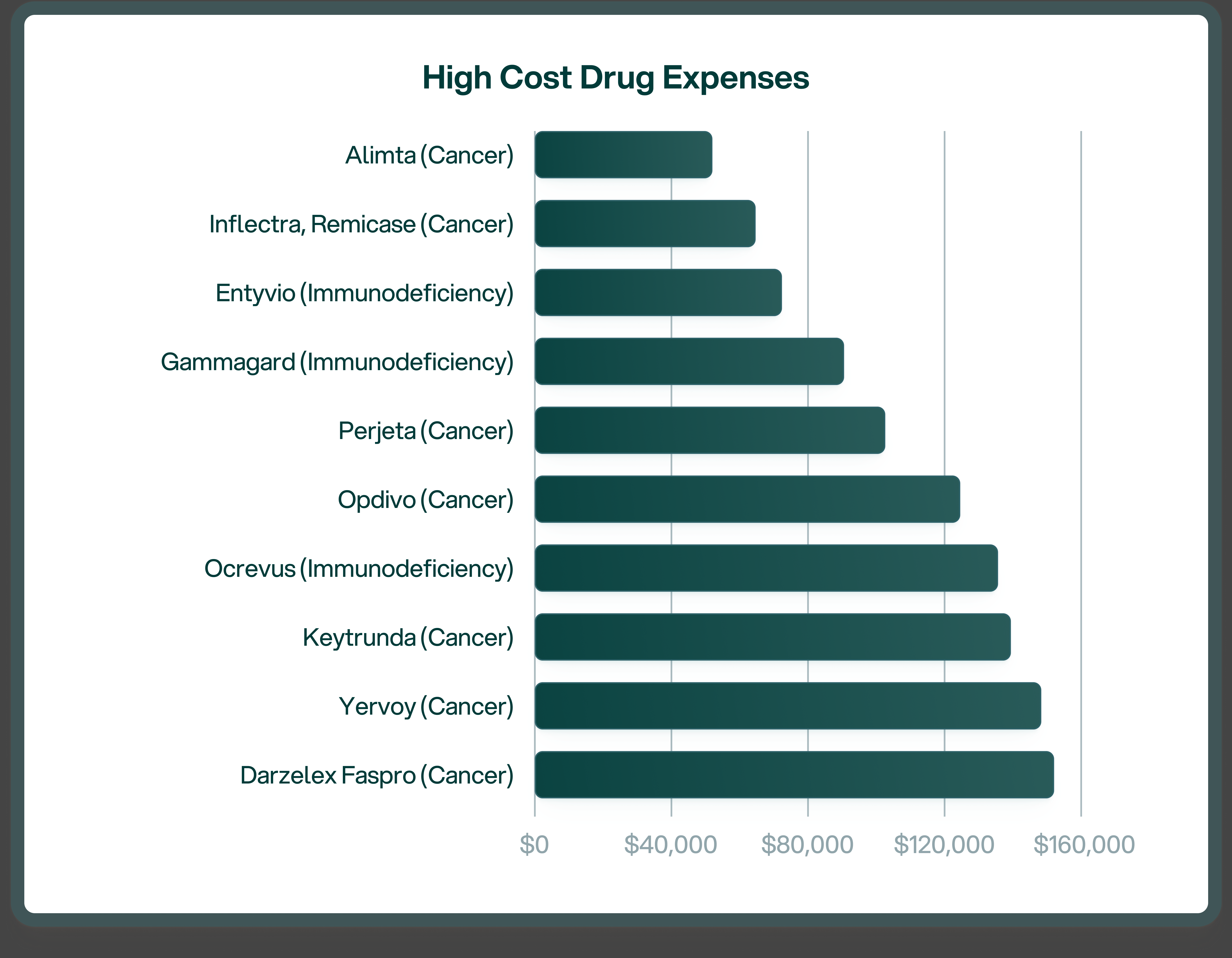

According to the National Alliance of Healthcare Purchaser Coalitions, the cost of high-cost treatments was up 4.4% over the year in 2024, climbing to an average expense of about $421 thousand - an average that is in part inflated by extremely high-cost new treatments/technologies (i.e. ~$7 million gene therapy) as well as the longevity-increasing impacts of improved treatments/technologies that can abate chronic conditions over longer periods of time (e.g. $60 thousand per month cancer drugs).

Perhaps most concerning, high-cost claims are on the rise among the younger demographics which employers and insurers rely upon to pay more into the system than they take out in order for the system to remain solvent.

Historically, only 1.2% of plan members are high-cost claimants, but they cost about 29 times more than the average plan member, amounting to an average annual expense per high-cost claimant of about $122 thousand.

FREE Insights+ Reports For Qualifying Employers

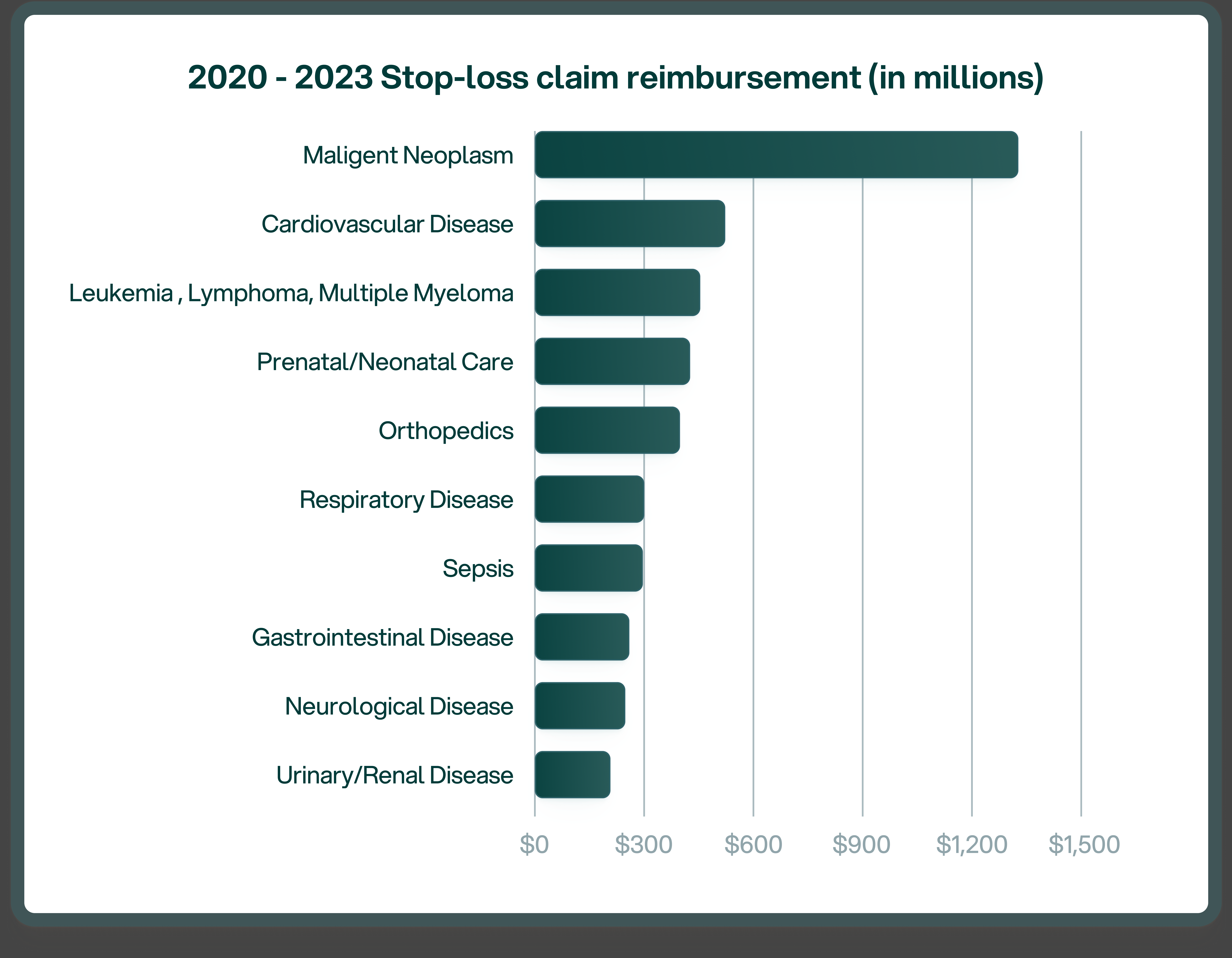

Over the last 4 years, the conditions that have resulted in the greatest number of high-cost claims include malignant neoplasm, cardiovascular system issues, cancer, prenatal/neonatal care, musculoskeletal problems, respiratory issues, sepsis, gastrointestinal conditions, neurological problems, and urinary/kidney diseases.

The list grows even smaller when looking at the types of conditions/treatments responsible for the largest number of $1 million plus claims, such as sepsis, cancer, prenatal/neonatal, and cardiovascular disease.

FREE Insights+ Reports For Qualifying Employers

There is little doubt among either experts or casual observers that there are systemic issues within the US healthcare system that will require system-wide solutions.

Individual employers - even those of substantial size - only have so much influence over rising healthcare costs that often seem more akin to a runaway train car than a properly functioning public and private health network.

Too often, however, employers misconstrued this limited control as though it were no control, which is when the train really starts picking up enough speed to jump the tracks.

In reality, there are many things that employers can be doing to exercise greater cost controls over their healthcare expenditures - and that is especially true for the highest-cost ticket items.

While employers historically have depended on the assistance of third-party administrators and pharmacy benefit managers to handle claims above a certain threshold, with these costs continuing to climb and no systemic relief currently in sight, forward-looking employers might be wise to take a more proactive approach in holding service providers to account and exploring cost-sharing approaches that don’t compromise quality of care.

There is no one solution to the high-cost claim issue, nor is there a one-size-fits-all solution that can be replicated and reapplied from one high-cost claim to the next, but there are many solutions - often starting with better data collection - that together can be form-fitted to cover the high-cost claim exposure of any given employer that recognizes the value of doing so, which will be an increasing number of employers as net costs for high-cost treatments keep rising.

.png)

Competing for Talent in a Constrained Market

The labor market remains highly competitive, particularly for skilled and high-performing roles. Despite some macroeconomic cooling, the structural shortage of qualified talent persists: nearly three-quarters of employers continue to report difficulty filling key positions. At the same time, employee expectations have evolved — flexibility, security, and well-being now weigh as heavily as base compensation in determining employer preference.

For most organizations, benefits represent one of the largest investments in the total rewards portfolio. Yet in practice, those investments are often under-leveraged in the recruiting process. Health coverage, retirement plans, paid time off, and wellness programs frequently appear as a brief bullet point in job descriptions or are mentioned only when an offer is extended. By that stage, the opportunity to differentiate has largely passed.

Mployer’s recent survey of more than 700 companies across 17 industries found that employers who clearly communicate the value of their benefits — and substantiate that value through credible data or recognition — are nine times more likely to be selected by candidates and to convert accepted offers. Transparency and validation drive both higher-quality applicant flow and stronger offer acceptance rates.

Transparency Converts Interest Into Action

In a competitive market, candidates are no longer applying indiscriminately. They evaluate prospective employers through publicly available information, reviews, and visible signals of value. When benefit information is vague, candidates interpret that as a risk. “Competitive benefits” have become shorthand for “average,” and uncertainty creates hesitation.

Conversely, when an organization provides a clear, quantified, and credible overview of its benefits, the dynamic changes immediately. Candidates are more willing to engage early, stay active through the interview process, and make faster, more confident decisions.

.png)

The Missed Opportunity: The Awkward Offer Conversation

In many recruiting processes today, the discussion around benefits occurs only after a verbal or written offer is made. The exchange is familiar: the candidate receives the offer, reviews the salary, and then pauses at the benefits section — uncertain whether what’s being offered is “good” or “below market.”

Recruiters often find themselves attempting to explain why the plan is competitive, citing anecdotal points about employer contributions or coverage levels. But without comparative data, the explanation sounds defensive, not differentiating. The candidate may nod politely but remain unconvinced — or worse, use the ambiguity to negotiate or delay.

At that stage, the opportunity to use benefits as a selling point has already been lost. The employer is reacting rather than leading.

In contrast, organizations that proactively communicate the strength of their benefits — in quantitative and comparative terms — enter offer discussions from a position of confidence. The candidate already understands the total value being provided and perceives the offer as comprehensive, not partial.

This is the distinction between defending your benefits and leveraging them. One undermines momentum; the other accelerates decisions.

Making Benefits a Strategic Differentiator

Leading employers are now approaching benefits communication as a core component of their talent strategy — not an HR formality. Several best practices have emerged:

These practices shorten time-to-hire, increase offer acceptance rates, and strengthen employer brand equity in measurable ways.

From Hidden Cost to Competitive Advantage

For many organizations, benefits are treated primarily as a cost center — a compliance requirement and a necessary expense. In reality, they are one of the most powerful levers available for talent attraction and retention.

When the value of those benefits is communicated with clarity, evidence, and confidence, the perception shifts. The benefits package becomes part of the employer’s market narrative — a tangible signal of how the company invests in its people.

In a tight labor market, that clarity doesn’t just help you attract candidates; it helps you close them.

How Mployer Enables Employers to Compete

Mployer helps organizations turn their benefits into a verified strategic advantage. We independently evaluate and rate employee benefit plans, comparing them across thousands of employers nationwide.

Participating organizations receive a clear assessment of how their benefits stack up against peers, along with recognition materials and benchmarking insights that can be shared directly with candidates. These assets — digital badges, comparison visuals, and concise summaries — give recruiting teams the ability to communicate benefit value credibly and consistently.

Employers across the country are already using Mployer’s data-driven validation to increase applicant volume, improve offer acceptance rates, and reinforce their reputation as employers of choice.

If you’d like to see how your benefits compare, we offer a free initial benchmark report to qualified employers. Join thousands of organizations already leveraging independent proof to strengthen their talent strategy — and move from explaining your benefits to winning with them.

In today’s hyper-competitive labor market, the fight for high-end talent has become a defining business challenge. Organizations invest significant resources into hiring and developing high- performing employees—only to lose them to competitors offering slightly higher pay or better benefits. The cost of voluntary turnover is not only financial; it disrupts operations, damages customer relationships, and erodes company culture.This white paper explores how offering market-competitive benefits—and communicating them effectively—dramatically reduces voluntary turnover. Backed by Mployer’s proprietary benchmarking and benefit rating data, we’ll show how employers that promote their benefits will experience on average 27% lower voluntary turnover each year and potentially up to 51% lower annual turnover compared to peers.

The Cost of Losing Great Talent

Every HR leader and CFO understands the financial cost of turnover—but few quantify its full scope. When an employee leaves voluntarily, costs include:

• Recruiting and onboarding new talent (often 30–50% of annual salary)

• Lost productivity during ramp-up and training

• Knowledge drain, as institutional know-how walks out the door

• Team disruption and morale impacts

• Customer relationship risks when account-facing employees depart

For specialized or customer-integrated roles, this loss compounds. A trained employee with both technical knowledge and deep integration into your teams and clients is a valuable asset—one not easily replaced. Studies show total turnover costs can exceed 1.5x–2x the employee’s annual salary for mid-level positions.

The Talent War: Competing Beyond Compensation

Across industries, the labor market remains tight. Wage competition has intensified, especially in sectors where every dollar per hour matters—manufacturing, wholesale trade, and financial services among them. Employees are increasingly willing to move for small pay increases, unless they clearly understand the total value of their benefits package.This is where benefit perception and communication become critical. When employees can see and understand the full value of what you provide—healthcare coverage, retirement matching, paid leave, mental health support—they’re less likely to be swayed by modest salary increases elsewhere. In short, benefits visibility equals retention power.

The Data: Better Benefits, Better Retention

Mployer Advisor’s analysis found that companies with highly rated benefits and effective benefits communication experience an average of 27% lower voluntary turnover than their peers. That’s a significant impact—one that directly translates into stronger productivity, reduced recruiting costs, and better workforce stability.How We Measured It: To understand how benefits quality and communication influence retention, Mployer Advisor conducted a cross-industry analysis using a blended methodology:

• Sample Group: Thousands of U.S. employers across key industries were evaluated, each with at least 50 full-time employees.

• Benefit Quality Scoring: Companies were benchmarked using Mployer’s proprietary benefit rating system, which integrates multiple data sources—including public ratings, plan benchmarking data, and employee feedback metrics.

• Communication Effectiveness: We measured not just the quality of benefits offered, but how clearly and frequently those benefits were communicated to employees through internal channels, digital materials, and recognition programs.

• Turnover Tracking: Over a 12-month period, we compared voluntary turnover rates among high-rated employers versus industry averages, focusing on trained, professional employees who had completed at least one year of tenure.The outcome was consistent and striking across every major sector: employers who both provide strong benefits and communicate them effectively retain significantly more of their trained workforce.

What this means in Practice - Let's put these numbers into context:

• Example 1: Mid-Sized Manufacturing Firm (200 Employees) Suppose a manufacturing company employs 200 workers with an annual average salary of $60,000 and a typical voluntary turnover rate of 20%. That’s 40 employees leaving each year. Replacing and retraining them at a conservative cost of 1.5× salary would total $3.6 million annually. With improved benefits communication and recognition, this firm could reduce its turnover by 44%—down to 22 separations a year—saving over $1.6 million annually in direct and indirect costs.

• Example 2: Growth-Stage Tech Company (50 Employees) A 50-person software firm might see a 25% voluntary turnover rate in a competitive labor market. Replacing those 12–13 employees could cost roughly $25,000 each in lost productivity and recruiting, totaling $300,000 per year. By improving benefits visibility and achieving results similar to the 27% national average reduction, the company could retain an additional 3–4 key employees annually—saving $75,000–$100,000 and preserving critical institutional knowledge.

The data and the dollars tell the same story: when employees both receive and recognize valuable benefits, they stay longer. Employers who treat benefits as a strategic investment—not just a line-item cost—achieve stronger retention, higher engagement, and measurable savings year over year.

Why Communication Matters as Much as the Benefits Themselves

Even the most generous benefits package fails to deliver ROI if employees don’t fully understand it. HR leaders often underestimate how little employees know about their coverage and perks. A recent survey found that:

• 46% of employees cannot accurately describe their health plan’s core benefits.

• Only 35% believe their employer communicates benefits “very effectively.”

• Yet 68% say that well-communicated benefits would increase their loyalty to the company.

Communicating benefits is no longer a once-a-year open enrollment exercise. It’s a year-round engagement effort that connects the dots between employee well-being and company investment.

Turning Benefits into a Competitive Advantage

This is where the Mployer Benefit Recognition Program makes the difference.

Through our Employer Benefit Award and recognition system, Mployer provides third-party validation that your benefits are not only competitive—but also worthy of public recognition.

Participating employers receive:

• An unbiased benefits rating benchmarked against industry peers

• A benefit summary report highlighting your strongest advantages

• Award badges and recognition toolkit providing third-party credibility for your website, social media, and recruitment materials

• Ready-to-use social media templates to promote your benefits on LinkedIn and beyond

• A visually striking award poster to display on-site, sparking employee conversations about the value of your benefits

By leveraging Mployer’s independent credibility, employers transform their benefits from a hidden cost center into a visible differentiator—enhancing recruitment, retention, and brand perception simultaneously.

Retention Starts with Recognition

In an era defined by labor shortages and rising turnover costs, the companies that win will be those that treat employee benefits not as an expense, but as a strategic investment.

The data tells the story: organizations that both offer competitive benefits and communicate them effectively enjoy up to half the turnover rates of their peers. Recognition, transparency, and consistent messaging are key to helping employees see the true value of what you provide.

Your workforce is your most valuable asset. Make sure they know how much they’re worth.

Learn more or see if your company qualifies for an Employer Benefit Award by visiting Mployer.

The modern labor market is defined by choice. In this competitive landscape, the time it takes to fill a critical position—your Time to Fill (TTF)—has become a painful metric. TTF measures the days between when a job is posted and when an offer is accepted, and every extra day costs your business. These are not just abstract numbers; they are tangible losses: decreased productivity from overburdened teams, halted projects, missed revenue targets, and increased recruiting fees (Source 1).

The solution to a high TTF doesn't lie solely in higher base salaries or aggressive sourcing. It lies in your benefits package.

Exceptional benefits are no longer a perk; they are the most efficient talent acquisition strategy to drastically reduce TTF. By treating your benefits package as a competitive differentiator, you can accelerate candidates through the hiring pipeline faster, saving thousands in the process.

The Attraction Phase: Benefits as a Candidate Magnet

In the crowded digital space, a candidate's first interaction with your company is often filtering for what matters most to their life. This is where your benefits package first accelerates the process.

Filter Efficiency and Signal Quality

Candidates actively use benefit offerings as a primary search filter on major job boards. By offering superior benefits, your role gains instant visibility among highly qualified candidates who are explicitly looking for employer support.

Furthermore, a robust benefits package serves as a powerful signal quality indicator. It immediately tells a prospective hire that your company is stable, healthy, and genuinely employee-first. This signals a positive company culture, immediately making your job more attractive than competitors offering standard, minimal coverage.

High-Value Benefits That Reduce Hesitation

Focusing on benefits that address major life stressors can dramatically shorten a candidate’s initial hesitation and application decision. High-perceived-value benefits like generous Paternity and Maternity Leave policies, comprehensive Mental Health Coverage, and practical Flexible Work Arrangements (Hybrid/Remote) instantly elevate your offer. These concrete; life-changing benefits are far more persuasive than a generic promise of a "competitive salary."

The Conversion Phase: Benefits as a Negotiation Accelerator

Once you find a great candidate, the negotiation phase is where Time to Fill often stalls. Strong benefits act as rocket fuel, accelerating the offer acceptance and minimizing costly, time-consuming back-and-forth.

Reducing Offer Time

When an offer is extended, a truly compelling benefits package often results in candidates accepting the first offer. They don't feel the need for lengthy counter-offers focused solely on base salary because the total value is already overwhelming.

A clear, well-articulated benefits statement in the offer letter minimizes follow-up questions, builds trust, and speeds up the decision-making process. The certainty and value provided by the benefits act as an irresistible closing tool.

Framing the Total Compensation Advantage

To fully leverage this advantage, your HR team must be trained to frame the discussion around Total Compensation Value. Show candidates how elements like a 100% 401(k) match, fully-funded health insurance options, or student loan repayment programs can easily surpass a perceived $5,000 difference in base salary.

When candidates are weighing multiple offers, the company that provides the most security, flexibility, and value outside of the paycheck will significantly shorten the candidate's decision time, often securing the top talent before competitors can react.

The Long-Term Ripple Effect on TTF

The benefits ROI doesn't stop once the offer is signed. A strategic benefits package initiates a powerful, long-term ripple effect that fundamentally lowers your overall vacancy rate and future TTF.

Boosted Employee Referrals

Happy employees are your best and fastest source of talent. When staff are genuinely satisfied with their compensation and benefits (especially high-value items like Sabbatical programs or generous PTO), they become powerful advocates. This satisfaction increases the likelihood of employees referring high-quality candidates, who are typically onboarded faster because of the pre-vetted nature of the relationship. Referral hires are consistently the fastest and cheapest source of talent for any organization.

Lower Turnover Rate

Ultimately, a high TTF is often symptomatic of high employee turnover. Strong benefits increase employee retention, meaning you have fewer open jobs to fill in the first place. Since TTF is calculated using both the vacancy rate and the duration of those vacancies, better benefits effectively tackle both components simultaneously.

Quantifying the Benefits: TTF vs. Public Perception

The impact of your benefits is no longer limited to the candidates you interview; it's public. When candidates research a company, they immediately consult public review platforms like Glassdoor. These platforms link candidate sentiment directly to your hiring efficiency.

Mployer’s recent analysis of 300 companies and over 2,000 open roles during a 120-day period revealed a critical connection between public sentiment and hiring speed. We compared organizations with exceptionally high Glassdoor benefit ratings (a key proxy for positive external perception) against those with mid-to-lower ratings. The result was a dramatic acceleration in the hiring funnel: for companies with top-tier benefit ratings, the average Time to Fill (TTF) was just 19 days, compared to 27 days for their counterparts—a significant 32% reduction in hiring time. While this trend was most pronounced among smaller organizations (like local businesses to mid-market firms), large global corporations (including Samsung, Morgan Stanley, and GE) demonstrated the same efficiency gain, affirming the universal impact of a strong benefit-based Employer Value Proposition.

Companies with an "Excellent" or "Above Average" benefit rating (4.0+ stars on Glassdoor, for example) consistently report a Time to Fill that is 15-20% shorter than industry peers with "Average" or "Poor" benefit ratings (Source 2). This efficiency is driven by the immediate credibility and trust built before the candidate even submits an application. A strong public rating reduces the need for the candidate to perform extensive due diligence, further accelerating the initial application phase.

Enhanced Employer Brand

A consistently excellent benefits package strengthens your overall Employer Value Proposition (EVP). This enhanced brand, which is now supported by public data, naturally improves all future recruiting efforts by attracting passive candidates who have been watching your company’s reputation grow.

Conclusion: The Investment That Pays for Itself

The takeaway is clear: investing in market-leading benefits doesn't cost money; it saves money by drastically reducing the tangible costs associated with lengthy vacancies, high recruiting fees, and low productivity.

Benefits act as an accelerant across all three critical phases of hiring: they Attract more candidates, convert them faster, and ensure their Retention, fueling a steady stream of future referral hires.

Action Item: Review your current benefits package through the lens of a prospective, top-tier candidate. Where can you add immediate, high-impact value? The race for talent is won by the company that makes the quickest, most compelling offer—and that starts with great benefits.

To gain a competitive edge and identify your specific TTF acceleration points, benchmark your offerings today. See how your benefits stack up against industry peers through a free, unbiased rating: Visit https://mployeradvisor.com/employer-rating

Sources

.svg)

.svg)

.svg)

.svg)