.svg)

The PBM Challenge in Today's Market

(An easy to understand guide)

Prescription drug costs have surged dramatically in recent years, placing increasing strain on employer-sponsored health plans. Between 2000 and 2020, retail prescription drug spending in the U.S. nearly doubled (a 91% increase) and continues to climb—outpacing most other healthcare cost categories. The rise stems from two primary factors: expensive new specialty therapies (like weight-loss and biologic treatments) and the opaque role of Pharmacy Benefit Managers (PBMs) in setting prices. What makes matters worse is that Americans pay dramatically more than people in other high-income nations—U.S. drug prices average 2.78 times higher than in 33 comparable countries, and brand-name drugs can cost more than four times as much. This steep cost trajectory and global overpayment emphasize why understanding and managing PBMs has become essential for employers aiming to control healthcare spend and protect employees.

How PBMs Actually Work

When an employer designs its health plan, it either chooses a PBM directly or selects a carrier that already has a PBM embedded in its plan. From there, the PBM takes control of the prescription drug benefit. They build the formulary—the list of drugs that are covered—and negotiate with manufacturers to decide which drugs make the list. By narrowing coverage to certain products, PBMs gain leverage to demand better deals. They also restrict which pharmacies are in-network, again concentrating volume to maximize bargaining power.

This means PBMs effectively set the market, costs, and tiers employees experience: whether a drug falls into Tier 1 with a $10 copay or Tier 4 with a 25% coinsurance is dictated by the PBM’s design. On the back end, PBMs collect rebates from drug makers. A rebate is essentially a kickback payment from the manufacturer to the PBM, offered in exchange for favorable placement of a drug on the formulary or higher expected utilization. For example, if two similar drugs treat the same condition, the manufacturer willing to pay a higher rebate is more likely to have their drug chosen. Some portion of these rebates is passed back to the employer to lower plan costs, but a significant share is often kept by the PBM—one of the biggest transparency concerns in the system

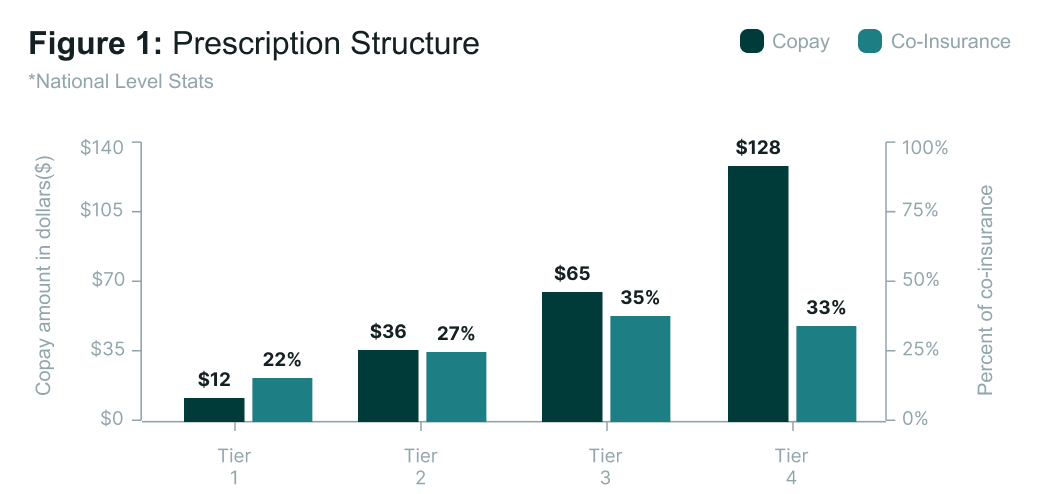

How Drug Tiers and Payment Structures Work

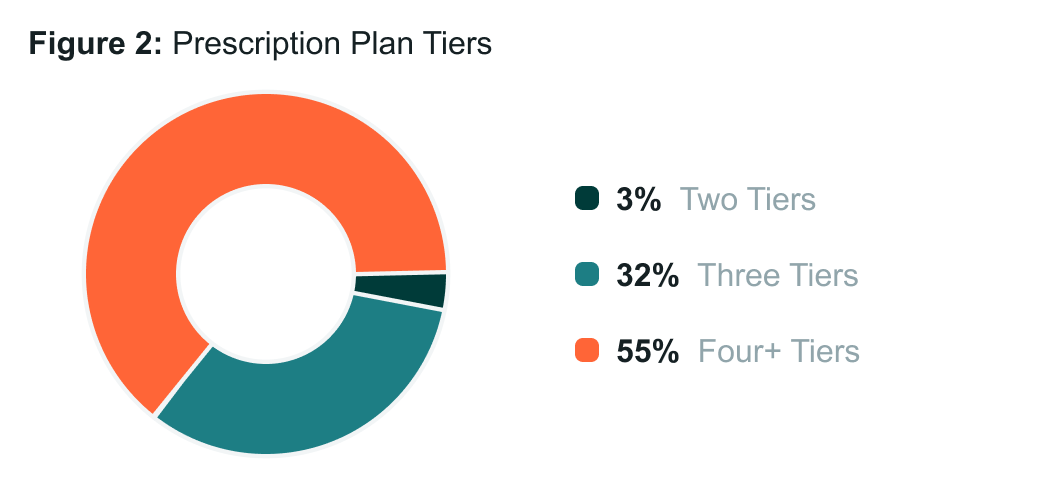

Most employer health plans organize prescription coverage into tiers, which determine both access and cost-sharing for employees.

- Tier 1 (Generics): Lowest-cost drugs, usually just a $10–$20 copay. They are widely accessible and often encouraged as first-line therapy.

- Tier 2 (Preferred Brands): Brand-name drugs that PBMs have negotiated discounts on. Employees typically pay $30–$50 copays or around 20% coinsurance.

- Tier 3 (Non-Preferred Brands): Higher-cost brand drugs not favored on the formulary. Employees may owe 40%+ coinsurance, leading to hundreds in out-of-pocket costs.

- Tier 4 (Specialty Drugs): High-cost therapies for serious conditions like cancer or hemophilia. These usually require coinsurance (20–30%), which can mean thousands of dollars per month. Although they make up less than 2% of prescriptions, specialty drugs drive nearly half of total drug spending.

Copays vs. Coinsurance

- A copay is a fixed, predictable dollar amount per prescription.

- Coinsurance is a percentage of the total drug cost until the deductible or out-of-pocket maximum is reached. While it helps share costs, it creates unpredictability—especially for specialty drugs, where 25% coinsurance could mean $250 on a $1,000 medication or much more on therapies costing thousands each month.

For employers, understanding how tiers and cost-sharing are structured is critical, since they directly affect both plan expenses and employee affordability.

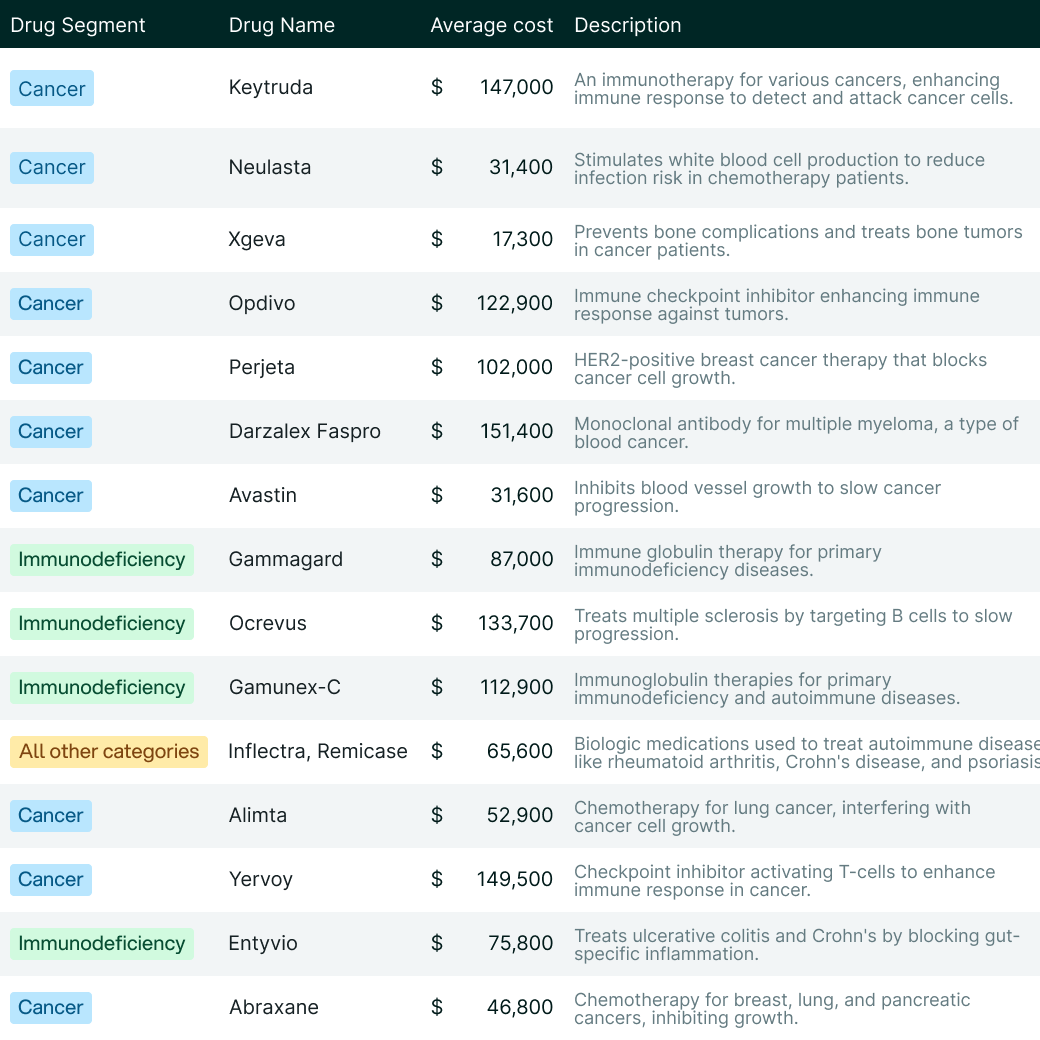

High-Cost Drugs and Their Outsized Impact

While high-cost drugs represent only a small fraction of total prescriptions, their impact on employer health plans is staggering. Specialty medications—such as those for cancer, hemophilia, and autoimmune disorders—account for less than 2% of prescriptions but drive close to 50% of all drug spending. Their costs have grown at double-digit rates year over year, fueled by new biologics, gene therapies, and infusion-based treatments that can run into hundreds of thousands of dollars annually. According to Sun Life’s High-Cost Claims Report, in many catastrophic claim categories like hemophilia or leukemia, prescription drugs make up more than 90% of the total cost of care. For employers, this means a single claimant on a specialty drug can dramatically shift overall plan spend, making pharmacy benefits one of the most volatile and financially significant areas to manage.

How Carriers Handle High-Cost Drugs

Carriers cover most FDA-approved specialty drugs but tightly manage access and cost. They use formularies to decide which drugs are included (and on what tier), require prior authorization or step therapy before approving treatment, and often restrict dispensing to their own specialty pharmacy networks. Coverage is generally limited to drugs deemed medically necessary, while experimental or non-formulary drugs are excluded unless appealed. For employees, this can mean higher coinsurance, delays in approval, and fewer choices on where prescriptions can be filled.

Who Controls the PBM Market—and Who’s Challenging It

Today, most carriers are tied to the “Big Three” PBMs, which together control more than 75% of the market:

- Aetna/CVS → CVS Caremark

- Cigna → Express Scripts

- UnitedHealthcare → OptumRx

- Anthem/Blue Cross (varies by region) → Caremark or Express Scripts

This consolidation means that for many employers, pharmacy benefits are automatically bundled with one of these large PBMs, leaving little room for visibility or flexibility.

The remaining 25% is made up of disruptors offering more transparent models. Players like SmithRx (pass-through pricing with detailed reporting), MedOne (independent PBM with customizable formularies and full rebate pass-through), and Mark Cuban’s Cost Plus Drugs (a direct-to-consumer model selling drugs at cost plus a small margin) are challenging the status quo. For employers, knowing which PBM their carrier relies on—and whether a carve-out to one of these disruptors is possible—can be a critical step in controlling pharmacy costs.

Legislation and Reform Efforts

In recent years, lawmakers have increasingly targeted the opaque practices of PBMs, introducing multiple federal bills like the Pharmacy Benefit Manager Transparency Act (S. 127, 2023) and the PBM Transparency Act of 2025 (S. 526). These aim to ban spread pricing, require full rebate pass-through, and mandate detailed reporting—but none have passed into law yet. Similarly, a 2025 House bill dubbed the PBM Reform Act proposes greater transparency around Medicare Part D contracts and delinking PBM compensation from drug prices, but it remains pending in committee.

At the state level, all 50 states have enacted some degree of PBM regulation. Few states have gone further: for example, Iowa is considering a law imposing minimum pharmacy dispensing fees, and Arkansas passed legislation curbing PBMs’ ownership of pharmacies—though that law has been temporarily blocked by a federal judge

In short: there's plenty of activity at both federal and state levels—but no sweeping reforms have become law yet, leaving employers to manage PBM challenges proactively on their own.

Be Educated: Key Questions to Ask Your Broker

- Who is our PBM, and is it bundled with our carrier?

- Do we receive 100% of rebates, or are they retained?

- Can we carve out our PBM given our size and funding model?

- Which high-cost drugs are driving our spend?

- Do we get claim-level reporting from our PBM? (often not)

- What specialty drug management strategies are in place?

- How does our plan compare to industry peers?

Closing Thoughts

Prescription drug costs are no longer a side issue—they’re a central driver of employer healthcare spend. The combination of high-cost specialty therapies and the opaque role PBMs play in setting formularies, controlling access, and managing rebates makes this one of the most complex and consequential areas of benefit management. For employers, the path forward starts with awareness: knowing which PBM you’re tied to, how rebates flow, which drugs are shaping your spend, and what levers you have to push for transparency or carve out alternatives.

While legislation at the federal and state levels may eventually bring more clarity and accountability to the PBM market, employers cannot afford to wait. By asking sharper questions, exploring disruptive PBM models, and partnering with brokers who understand this space, employers can take meaningful steps today to control costs and support employees more effectively.

Bottom line: Prescription drug costs are only going up. Employers that engage now—by digging into the details and holding PBMs and carriers accountable—will be best positioned to protect both their budgets and their people.

.svg)

.svg)

.svg)

.svg)