.svg)

If you are shopping around for health insurance, chances are you have heard the term ‘insurance broker’ thrown around a few times. While both insurance agents and insurance brokers act as intermediaries between insurance sellers and buyers, they have different job functions.

Where an insurance agent represents one or more insurance companies, an insurance broker works directly for the client. On the other hand, brokers work for you and only you and will use their experience to provide the best insurance package for your specific needs.

When shopping around for a business insurance broker, there are a few things you should ask to ensure they are the best fit for what you are looking for. Here’s an insider’s guide of what an employer should ask an insurance broker before hiring them.

You’ll want to know more about your broker’s business to get a sense of their experience. A business insurance brokerage that has been around for a while is a great sign that they are well-versed with a lot of different business types and the issues you may face. It’s also a good idea to ask for references and to ask about what some of their success stories are. Doing this will help you see their track record, and if their previous experience aligns well with your goals.

There’s no such thing as a good answer or a bad answer to this question, but make sure to follow your gut. Your insurance broker’s job is to represent you, but if something seems off, make sure to act on it.

Insurance brokerages can be quite large, and you want to make sure that you are more than just a number to them. It is important to ask about who you will be working with, as this gives you an idea of how this firm operates. They should provide you with a dedicated account manager that serves as your only point of contact, but if they don’t, proceed with caution. An account manager makes sure that all your needs are met, and that you are treated as an individual. You will need to evaluate if a large firm or small firm is best. Who are you working with and how long have they been in the business.

You may already have some type of insurance coverage, and an experienced broker can take a look at what is working well for you and what isn’t. Based on their findings, they can create a customized plan for your needs, and fill in any coverage gaps you may be experiencing. Make sure to sit down with the broker to analyze your specific plan before you start discussing other options, as you want to make sure your concerns are heard before you enroll in a new plan.

Not all plans are created equally, so you will want to hear out all the different types of options available to you before you decide. There is no such thing as a one-size-fits-all type of insurance plan, so take your time listening to the plans they offer, and ask as many questions as possible.

Additionally, you’ll want to find out about the different types of health plans. Indemnity plans are a type of health plan that require you to pay a certain percentage of healthcare costs when the healthcare company pays the rest. There are also managed care systems, health maintenance organizations (HMOs), and preferred provider organizations (PPOs), that can add versatility to your health insurance plans. At the very least, you should expect your broker to provide a comprehensive list of health insurance terms, rates, and benefits for multiple options for your review.

Some insurance brokerages have salaried workers, whereas others rely only on commission-based sales. The health insurance company will pay the broker out of their end of the sale, so it doesn’t cost you anything to use a broker’s service. But sometimes, they add on an extra brokerage fee on top of your plan.

Asking upfront about any extra charges ensures you’re not surprised down the line.

Each brokerage handles the open enrollment process in a different way. Some may take care of enrolling for you when others require the clients to do it themselves. It is important to ask your insurance broker how they will streamline the entire process to make everything easy for you. They may even offer some tools that can make the process a bit easier for you, but again, this may take some time to learn. You want to be as prepared as possible going into open enrollment, and asking all these questions ahead of time will set you up for success.

You will need to renew your plan every single year, and some insurance brokerages have certain automatic renewal processes set up as a way to streamline the entire process. Generally speaking, a systematic renewal process will go into place about 45 to 60 days leading up to the renewal date. But it is important to be aware of your insurance brokerage’s renewal process because it is best practice to ask your broker to negotiate a better rate for you every year, and you don’t want to get enrolled in the same plan if you wanted to make a change.

It is best to know your business insurance broker’s capabilities in the following three areas:

The answers to these questions will shed light on how the brokerage works, and if its operations align with what you are seeking.

Finding the right business insurance broker for your business doesn’t have to be a daunting task. With these questions to help guide the conversation, you’ll be confident in knowing that you’ll be making the right decision for your business needs and goals. Looking for more exclusive content? Check out what’s trending on the Mployer Advisor blog.

August Release Notes: Catalyst and Insights

Welcome to our latest release. We are excited for you to try the new features. This release focused on four things: making Mployer AI available throughout every product, rebuilding each product's home page to put the AI assistant front and center, adding new filters in Catalyst to help you find more opportunities, and opening free tiers on all products. Below is a summary of the major changes.

Mployer AI throughout Catalyst

The Mployer AI panel is now available on every Catalyst search grid: Employer, Commercial P&C, Broker, Carrier, Company, PEO, and Retirement. You can ask questions about your results without leaving the search.

The home page search bar has been replaced with the same AI chat. You can ask about companies, OSHA data, or benefits in plain language from the top of the page, and your chat history is retained on your device.

All AI surfaces in Catalyst, including the in-app chatbot and home page search, now run on an updated MCP backend, making every assistant significantly smarter.

Commercial Search

Experience Mod, carrier relationship, modeled payroll, and premium are now available as filters and columns in Commercial Search. OSHA and DOT records show violation gravity, the number of employees exposed, and 12-month trend direction across violations, crashes, and drivers. P&C brokers can now build prospect lists around financial exposure and compliance risk directly in the grid.

PEO Search

PEO Search, Snapshot, and Company Snapshot now show a single view of an employer's most recent PEO affiliation, with full switching history available from the same place. Previously, multiple affiliations could appear as separate records. Filters, columns, and exports now include Filing Source, PEO status, Benefits and Overall Rating, Most Recent Filing, EIN, and NAICS, bringing PEO Search in line with Employer Search.

Export and contact visibility

The export modal now shows your remaining credit balance and the actual record count and cost after exclusions, before you confirm. The "Exclude Previously Exported" option now covers the past 12 months rather than your full export history.

Contact records display an email verification status at all times, and you can filter contacts by that status when prioritizing outreach.

Mployer AI on the Insights home page

You can now ask questions about your book of business directly from the Insights home page. An AI assistant sits alongside your submissions and works against your client data, so you can ask which clients scored below benchmark, which reports are complete, which clients qualify for an award, or "show me completed reports where voluntary STD is offered," and get the answer without building filters by hand.

You can filter submissions by benchmark score, lifecycle state, and award eligibility, run reports from the same view, and export any filtered result to CSV.

Free tiers on all products

Every product now includes a free tier. We encourage you to try out all the resources now available to you.

AI panel on Insights+ reports

The Mployer AI panel on Insights+ HTML reports has been redesigned to match the AI panels in the rest of the platform, with the same layout, controls, and prompt patterns. Generate recommendations and ask any questions about the report and data, and get answers instantly.

Help Center

A new Help Center is live, with a home page, per-product detail pages, and a video tutorial library. Webinars, product updates, a glossary, and FAQs will be added within the same structure.

If you have questions about any of these changes, contact Partner Success or reach us through the Help Center.

The Likely Fastest-Growing Line in Your Benefits Budget

Modern medicine has produced remarkable advances. Cancer therapies that were not available five years ago are now extending and saving lives. Treatments for autoimmune diseases, multiple sclerosis, and rare genetic conditions are giving employees and their families real options where few existed before. As an employer, providing access to these treatments through your benefit plan is one of the most meaningful things your organization does for the people who work there.

It also comes with a financial reality that every benefits decision maker needs to understand clearly. Over 25% of total employer health benefit expenses are now driven by prescription drugs, and within that figure, a small number of specialty drugs account for an outsized share of the cost. A single covered employee on an oncology therapy can generate $100,000 to $170,000 or more in annual drug spend. A handful of members on these treatments can represent a larger budget impact than the entire pharmacy spend of the rest of your workforce combined. The goal is not to restrict access to these medications. The goal is to understand how the system works, how costs flow, and how to structure your plan so that both your employees and your organization are best positioned for the long term.

This piece covers how the pharmacy benefit system works, how your plan’s tier structure determines who pays what, how stop-loss insurance interacts with high-cost drug claims, and what employers can do to manage this exposure thoughtfully.

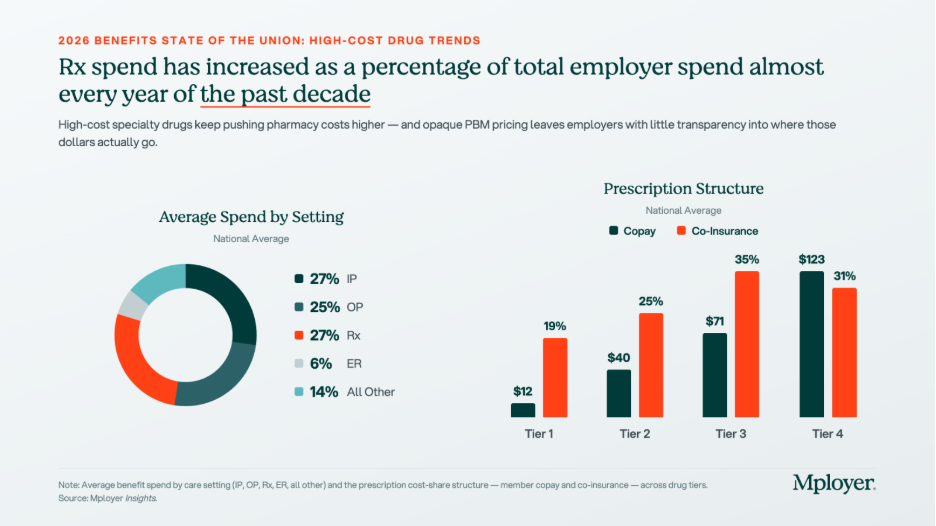

The tier structure in the chart above reflects how plans already account for the cost complexity of specialty drugs. Tier 4, which is where specialty biologics and injectables are typically placed, carries significantly higher cost-sharing than the other tiers: an average employee copay of $123 and coinsurance requirements in 31% of plans. But Tier 4 behaves very differently from the other tiers. On Tier 1, 2, and 3 drugs, cost-sharing is relatively predictable and manageable. On Tier 4, the combination of high drug cost and percentage-based coinsurance can generate out-of-pocket exposure that approaches or exceeds a patient’s annual out-of-pocket maximum in a single month of therapy. How Tier 4 is structured, what controls are in place, and how the plan manages cost is one of the most consequential design decisions an employer makes.

Understanding Your Benefit Plan’s Pharmacy Options

How Pharmacy Benefit Managers Work

Most employer health plans do not manage pharmacy benefits directly. That function is delegated to a Pharmacy Benefit Manager, or PBM, which acts as the intermediary between the health plan, the pharmacy, and the drug manufacturer. The PBM builds and maintains the formulary, negotiates drug prices and rebates with manufacturers, contracts with pharmacy networks, and processes pharmacy claims. The three dominant PBMs, Express Scripts (owned by Cigna), CVS Caremark (owned by CVS Health / Aetna), and OptumRx (owned by UnitedHealth Group), together manage the pharmacy benefits of approximately 80% of covered lives in the United States. Each is affiliated with a major carrier, meaning that employers who use an ASO medical arrangement often default to the carrier’s affiliated PBM without realizing it. Independent PBMs such as Capital Rx, Navitus, and MedOne Pharmacy Benefit Solutions operate on transparent, pass-through pricing models that return all rebates to the plan rather than retaining them as PBM revenue. PBMs are compensated through administrative fees, spread pricing (charging the plan more than the pharmacy receives and keeping the difference), manufacturer rebates in exchange for formulary placement, and specialty pharmacy margin. For any employer managing meaningful specialty drug spend, understanding which of these revenue sources applies to your contract is essential.

How Drug Tiers and Cost-Sharing Work

Every pharmacy benefit plan organizes covered drugs into tiers, with cost-sharing that increases as you move from Tier 1 generics (avg. $12 copay) through Tier 2 preferred brands ($40), Tier 3 non-preferred brands ($71), and into Tier 4 specialty drugs ($123 copay, with coinsurance in 31% of plans). The tier placement of a drug affects both what the employee pays and, indirectly, what the plan pays, since tier placement drives utilization patterns. Plan sponsors have real levers here: step therapy (requiring a patient to try a lower-cost drug first), prior authorization, specialty pharmacy channel mandates, and formulary exclusions all affect Tier 4 cost without eliminating clinical access. These controls require balancing cost management with the reality that for many specialty drugs, no lower-cost alternative achieves the same clinical outcome.

How Stop-Loss Insurance Interacts with High-Cost Drug Claims

For self-funded employers, specialty drug claims are now among the most common triggers for individual stop-loss reimbursement. A single employee on a cancer therapy or rare disease treatment can generate pharmacy claims that exceed the plan’s specific stop-loss deductible, which averages $141,938 nationally for self-insured plans, within a single plan year. The mechanics: the employer pays all claims up to the deductible threshold, and the stop-loss carrier reimburses costs above it. Several dynamics are specific to high-cost drugs. At renewal, stop-loss carriers may laser a known high-cost member by raising their individual deductible or excluding them from coverage. Some carriers now specifically carve out GLP-1 medications or other high-utilization drug categories from stop-loss reimbursement, so employers adding new drug coverage should verify what their contract covers. Specialty drugs can also be administered under either the pharmacy benefit or the medical benefit depending on whether they are self-administered or clinic-administered, and some stop-loss contracts apply different terms to each channel. Employers should model their actual specialty drug cost distribution against their stop-loss deductible at every renewal to understand where the plan’s real exposure sits.

The Costliest Specialty Drugs: What They Treat and What They Cost

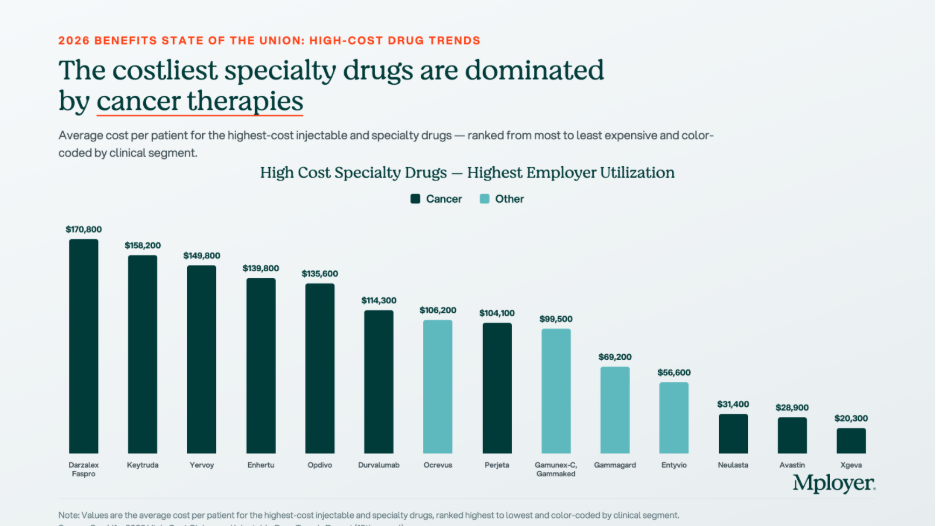

The chart below shows the highest-cost specialty and biologic drugs by average cost per patient, ranked from most to least expensive. Cancer therapies dominate the top of the list, but treatments for autoimmune conditions, MS, and inflammatory disease also appear, reflecting how broadly specialty drug spending is distributed across a workforce.

Biosimilars: The Cost Opportunity Most Employers Are Not Fully Using

A biosimilar is a biologic drug that is highly similar to an already-approved reference biologic, with no clinically meaningful differences in safety, purity, or potency. Biosimilars are not generic drugs in the traditional sense, because biologic drugs are complex proteins manufactured from living cells and cannot be chemically replicated exactly. But they go through an FDA approval pathway that confirms their clinical equivalence to the reference product, and they cost significantly less. The biosimilar market has expanded rapidly as major biologic patents have expired. Humira, the world’s best-selling drug for much of the past decade, now has multiple biosimilar competitors in the U.S. Stelara has followed. The oncology biosimilar pipeline is maturing, with more approvals expected in the next two to three years.

The chart above shows what biosimilar substitution looks like in dollar terms. For Humira, the net price after rebates and negotiated discounts is $2,370 per box. The biosimilar Yusimry has an estimated net price of $635, a 73% reduction. For Stelara, the reference drug net price is $7,636 per box. The biosimilar Starjemza has an estimated net price of $4,010, a 47% reduction. For an employee on monthly Humira therapy, the difference between the reference drug and the biosimilar is approximately $21,000 per year in net plan cost. For a Stelara patient, the annual difference is approximately $43,500. Across even a small number of members on these therapies, biosimilar substitution is one of the highest-return cost management interventions available.

Plan sponsors have four main tools to drive biosimilar adoption: preferred formulary placement (putting the biosimilar on a lower tier and the reference drug on a higher tier), step therapy for new patients, automatic substitution where state law permits, and formulary exclusion of the reference drug entirely. The most important variable in any biosimilar strategy is whether your PBM has a financial incentive to keep the reference drug preferred. A PBM earning a large rebate on Humira has a direct financial reason to keep Humira on the preferred formulary, even when the biosimilar costs the plan less on a net basis. Independent PBMs operating on pass-through pricing remove this conflict entirely, because all rebates return to the plan and formulary decisions are made without a competing financial interest.

What Employers Should Be Asking About Their Pharmacy Benefit

High-cost drug management requires active decisions about PBM contract structure, formulary design, specialty pharmacy strategy, and stop-loss alignment. The questions worth asking at every renewal:

Know How Your Pharmacy Benefit Compares

Pharmacy is now one of the two or three most consequential cost management decisions in health plan design. The employers managing it well are not restricting access to the medications their employees need. They are ensuring that the structure of the benefit, the PBM contract, the formulary design, and the stop-loss coverage work together in the plan’s interest, and that every dollar spent on high-cost drugs is spent as efficiently as possible.

Mployer’s benefits rating evaluates pharmacy benefit design as part of the Medical pillar score, benchmarked against a custom cohort matched by size, region, and industry. Knowing where your pharmacy benefit stands relative to employers who actually look like you is the starting point for making better decisions.

See how your benefits package compares to your custom cohort at MployerAdvisor.com.

Sources

Mployer Insights: Average Spend by Setting, Prescription Structure, and High-Cost Specialty Drugs. Source: Mployer Insights analysis.

MedOne Pharmacy Benefit Solutions: Biosimilar substitution impact data for Humira/Yusimry and Stelara/Starjemza. MedOne is a leading independent PBM focused on improving health outcomes and reducing net costs for self-funded employers. [email protected].

Mployer 2025 and 2026 Employee Benefit Plan Design Study, covering 50,000+ employer plans. Individual stop-loss avg $141,938 self-insured.

Consolidated Appropriations Act of 2021, Section 202: broker/consultant compensation disclosure requirements for group health plans.

FDA Biosimilar approval framework: 42 U.S.C. Section 262(k).

Parental and Maternity Leave: What Employers Need to Know

If there is one area of employee benefits where employer decisions signal values as loudly as economics, it is parental leave. How an organization treats employees who are growing a family, both during the leave itself and in how it structures the financial support, tells candidates and employees a great deal about whether the organization means what it says about supporting its people.

This is Part 2 of our leave benefits series. Part 1 covered the foundations: vacation, paid holidays, sick leave, consolidated vs. non-consolidated plans, workplace flexibility, and the federal and state legal framework. This post goes deeper on maternity and parental leave specifically: what the terms mean, how the programs are structured, what federal and state law requires vs. what employers choose to provide, and how the data from 50,000+ employer plans describes the current state of the market.

The data in this post is at the national all-employer average. The variation beneath that headline, by industry, employer size, and region, is significant. A technology employer in a major metro area competing for mid-career talent faces a very different parental leave benchmark than a regional manufacturer or a healthcare employer in a mid-size market. Both contexts are worth knowing. The national benchmarks in this post show where the floor and the ceiling are. Knowing where your specific cohort sits requires a custom comparison.

Key Terms Every Benefits Decision Maker Should Know

What the Law Requires: Federal and State Baseline

Federal FMLA

Federal FMLA, covered in depth in Part 1, provides the baseline: up to 12 weeks of unpaid, job-protected leave for the birth, adoption, or foster placement of a child. This applies to employers with 50 or more employees. The critical word, again, is unpaid. FMLA does not require the employer to pay anything during parental leave. It only requires that the job be protected and that group health insurance continue during the leave period on the same terms as if the employee had not taken leave.

FMLA also applies to both parents, which is a point often overlooked. The non-birth parent, whether an adoptive parent, a same-sex partner, or a non-birth parent of any kind, is entitled to the same 12 weeks of unpaid job protection under federal FMLA as the birth parent, assuming all eligibility requirements are met.

State Paid Family Leave Programs

The paid leave piece, when it exists at state level, comes from state paid family and medical leave programs. These are state-administered insurance programs that pay a wage replacement benefit, typically 60 to 90 percent of the employee’s wage up to a weekly cap, to employees on qualifying parental or family leave. The most established programs are in California, New Jersey, New York, Washington, Massachusetts, Connecticut, Oregon, Colorado, Rhode Island, and the District of Columbia, with additional states phasing in programs in the coming years.

These programs are funded through payroll contributions, typically deducted from employee wages, sometimes matched by employers. The benefit is paid by the state program, not directly by the employer, though the employer is responsible for administering eligibility, managing payroll deductions, and coordinating the state benefit with any employer-provided leave. Employers in states with paid leave programs should understand how the state benefit interacts with their own leave policy, including whether employees are required or permitted to use accrued PTO concurrently with state paid leave.

Pregnancy Discrimination and PUMP Act

Two additional federal laws shape the employer’s obligations around pregnancy and parental leave. The Pregnancy Discrimination Act prohibits employers with 15 or more employees from discriminating against employees on the basis of pregnancy, childbirth, or related conditions. The PUMP for Nursing Mothers Act, enacted in 2022, requires employers to provide reasonable break time and a private space for nursing employees to express breast milk for up to one year after the child’s birth. These are separate from FMLA and apply to a broader range of employers.

Maternity Leave: What the National Data Shows

68% of employers nationally offer dedicated maternity leave beyond statutory short-term disability. 32% do not, meaning those employees rely entirely on STD for any paid income during leave, typically six to eight weeks at whatever percentage the disability plan covers. Among the 68% who do offer dedicated maternity leave, eight weeks of additional paid leave is the most common duration at 31%, with twelve weeks close behind at 26%. Together those two categories account for more than half of all programs. 16% of employers offer thirteen or more weeks of additional paid leave, placing them at the generous end of the market nationally.

Reading this data correctly requires understanding what these weeks represent. The duration bars in the chart show the additional paid leave added on top of disability coverage, not the total leave period. An employee at an employer offering eight weeks of additional leave on top of a six-week STD benefit has fourteen weeks of paid leave total before any unpaid FMLA job protection kicks in. That total is what candidates and employees are actually comparing when they evaluate a parental leave program.

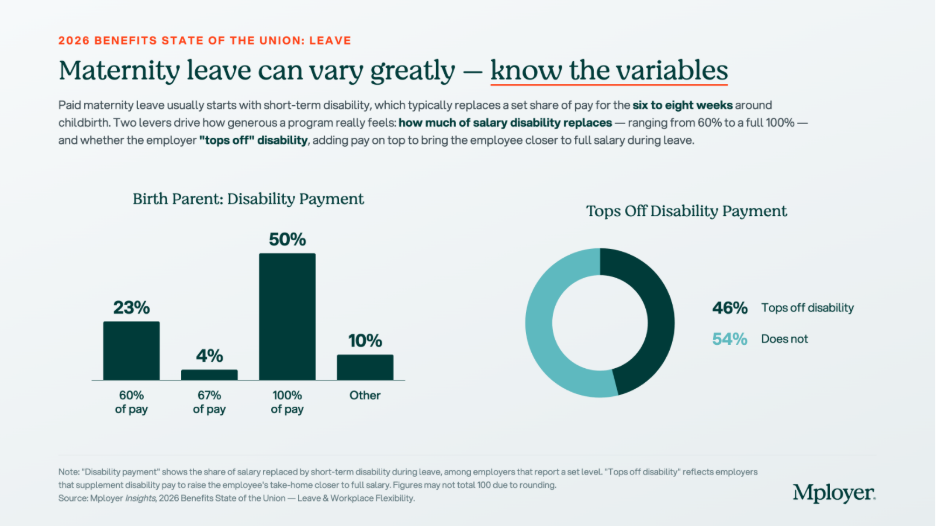

Disability Payment Rates and Top-Off: The Variables That Define Generosity

The chart above tells the real story of how financially supportive maternity leave programs are. On the disability payment rate, the market has split sharply: 50% of employers with a defined disability payment rate pay 100% of salary during the disability period, while 23% pay the traditional 60% of salary. The gap between these two is meaningful. An employee earning $80,000 per year on a six-week disability period at 60% of pay receives approximately $5,538. At 100% of pay, she receives $9,231. That $3,693 difference is real money for a new parent.

The top-off picture is similarly divided. 46% of employers supplement the disability benefit to bring the employee closer to full salary. 54% do not. An employer who pays STD at 60% of salary and does not top off is providing the minimum financial support that a standard disability plan delivers. An employer who pays 100% of salary or who tops off a 60% plan to full pay is making a meaningfully different statement about how much they value employees during one of the most important transitions of their lives

The combination of these two variables, disability payment rate and top-off, is what candidates from competitive talent markets are increasingly asking about directly. It is not enough to say your company offers paid maternity leave. The question they are asking is: how much will I actually receive, and for how long?

Non-Birth Parent Leave: A Growing Expectation, Not Yet a Standard

41% of employers nationally offer dedicated non-birth parent leave, meaning leave specifically provided for partners, fathers, adoptive parents, and same-sex parents who are not the birth parent. 59% do not. Among those who do offer non-birth parent bonding leave, twelve weeks is the most common duration at 32%, with six weeks next at 23%. The 30% in the Other category reflects the wide variation in how these programs are structured, including tiered policies, programs that vary by tenure, and policies that provide different durations based on the type of parental event.

The gap between maternity and non-birth parent leave offer rates, 68% vs. 41%, reflects the historical pattern of parental leave being designed primarily around biological motherhood and disability recovery. That framing is shifting. Candidates across generations, and particularly millennial and Gen Z candidates who are entering or approaching family formation years, are increasingly evaluating parental leave as a package: not just what the birth parent receives, but whether the partner can also be present. An employer offering generous maternity leave but no paternity or bonding leave is offering a program that structurally assumes only one parent takes significant time away, which does not match how many families today want to organize the early months of a child’s life.

Non-birth parent leave also has a practical retention implication. Employees who take bonding leave and feel supported by their employer during it are more likely to return to work and remain engaged. The data on parental leave and retention consistently shows that leave policies affect long-term retention rates, not just initial job acceptance.

Fertility and Adoption Benefits: Rare but Rising

28% of employers nationally offer IVF coverage as part of their medical or family-building plan. 11% offer adoption assistance. Both numbers reflect concentrated adoption among larger employers and in specific geographies and industries, particularly technology, financial services, and professional services employers in major metropolitan markets. Coverage terms, lifetime maximums, and eligibility criteria vary widely among the minority of employers who offer these benefits, making direct comparisons difficult without plan-level detail.

IVF treatment costs can reach $15,000 to $30,000 or more per cycle, with most patients requiring multiple cycles. For employees who need IVF to build a family, employer coverage is not a luxury benefit. It is a financial necessity that directly affects whether they can afford to pursue treatment at all. For employers, IVF coverage is a high-signal benefit: it communicates investment in the full arc of an employee’s family life, not just the period after a child arrives. Among employers competing for talent in industries where IVF coverage has become a common offering, its absence is noticed.

Adoption assistance typically covers qualified adoption expenses such as legal fees, agency fees, home study costs, and travel, up to an annual maximum that varies by employer. The IRS allows employers to provide up to $17,280 in adoption assistance per child tax-free in 2026. Adoption leave policies, separate from adoption assistance, are covered under FMLA for qualifying placements and under many state paid leave programs as well.

Parental Leave as a Talent and Retention Strategy

Parental leave is one of the most emotionally charged benefit decisions a candidate makes. It is also one of the most concrete. Unlike dental coverage or life insurance multiples, parental leave generates direct, personal financial calculations: how much will I receive, for how long, and what will that mean for my family’s finances and my ability to be present during a period that does not repeat?

Employers who have invested in a strong parental leave program and are not talking about it are leaving one of their best recruiting assets on the table. A program that offers twelve or more weeks of additional paid leave, a top-off to full salary, and bonding leave for non-birth parents is well above the national market on all three dimensions. That is a specific, documentable competitive advantage in candidate conversations, offer letters, and employer brand communications. It does not require marketing language. It requires knowing what your program provides and being willing to state it clearly.

Employers who are uncertain about where their program stands face a different challenge. If you are not sure whether your maternity leave duration, your disability payment rate, your top-off policy, and your non-birth parent bonding leave compare favorably to the employers recruiting against you, you cannot use those elements as differentiators, and you cannot address them strategically at renewal. The national benchmarks in this post give you the market context. The custom cohort analysis Mployer builds from employers matching your industry, region, and size gives you the specific comparison that matters for your talent market.

Parental leave policy is not static. The market has moved meaningfully in the past five years and continues to move. Employers who last reviewed their parental leave program three or more years ago are likely benchmarking against a standard that has already shifted. Knowing where you stand today is the starting point for deciding whether to maintain, improve, or actively use your program as a recruiting asset.

See how your parental leave and full benefits package compare to your custom cohort at MployerAdvisor.com.

Sources

Mployer Insights, 2026 Benefits State of the Union: Leave & Workplace Flexibility. Source: Mployer Insights analysis of 50,000+ employer benefit plans. All Nation Average.

Family and Medical Leave Act of 1993 (FMLA), 29 U.S.C. Section 2601 et seq. Applies to employers with 50+ employees.

Pregnancy Discrimination Act, 42 U.S.C. Section 2000e(k). Applies to employers with 15 or more employees.

PUMP for Nursing Mothers Act (2022), amending the Fair Labor Standards Act. Applies to most employers.

State paid family leave programs: California (SDI/PFL), New Jersey (TDI/FLI), New York (NY DBL/PFL), Washington (WA PFML), Massachusetts (MAPFML), Oregon (OPFML), Colorado (FAMLI), Rhode Island (TCI), Connecticut (CTPFML), District of Columbia (DC PFML).

IRS adoption assistance exclusion 2026: $17,280 per child, per IRS Notice 2025-61.

.svg)

.svg)

.svg)

.svg)