The average US employee costs their employer about $45.42 per hour in total compensation expenses, excluding members of the armed forces. A little less than 70% ($31.29) of that total compensation was earned in salary and/or wages while a little more than 30% ($14.13) of that expense covered employee benefits and perks according to the BLS.

Benefits and perks cross a number of segments. Below is the full breakdown but as you can imagine, the majority comes from medical, social security, leave, and retirement. While life, disability, dental and vision are all important, the only represent a small percentage of the full medical.

Employers each year invest over $1T into their employee's benefits, this is over 5% of the US GDP. Your firm does the same, employee benefits are often one of the top five expenses each year for an employer, in some industries it is in the top three.

Going one level deeper, the average hourly wage/salary costs were nearly identical between service employees and goods producing employees at $30.34 and $30.31 hours, respectively, whereas the average hourly employee benefits expense was a couple dollars higher for goods-producing employees at $14.44 an hour per employee than for service employees at $12.44 an hour per employee.

Expenses derived from leave, however, whether paid time off or sick leave, were slightly higher for the service industries at $3.34 per hour relative to the $2.82 per hour average leave expense for employees in industries that produce goods.

Employee Compensation Costs by Industry

First, lets take a look by industry. As the following chart illustrates, the information industry had both the largest wage/salary expense at $48.25 per hour and the largest employee benefits expense at $26.60 per hour, for an average total compensation expense of $74.85 per employee per hour.

Despite paying a slightly lower average wage/salary expenses per employee at $47.95 than the information industry’s $48.25, the utilities industry nonetheless has the highest average hourly total employee compensation expense at $76.91 as a result of boasting the largest average hourly employee benefits expense of $28.96.

The other services industry had the lowest average total employee compensation costs of just $17.82, followed by leisure and hospitality at $19.44, and the retail industry at $25.08 before making the jump up to the manufacturing industry, which spends an average of $43.68 on employee compensation per hour.

Interestingly, despite paying the lowest wages and salaries, the other services, leisure and hospitality, and retail industries pay the largest proportion of total employee compensation in the form of wages and salaries. In short, the pay is relatively bad in these industries and the benefits are even relatively worse.

Employee Benefit Expense Breakdown

As noted above, the split between wages/salary expenses and employee benefits expenses was about 70% to 30%.

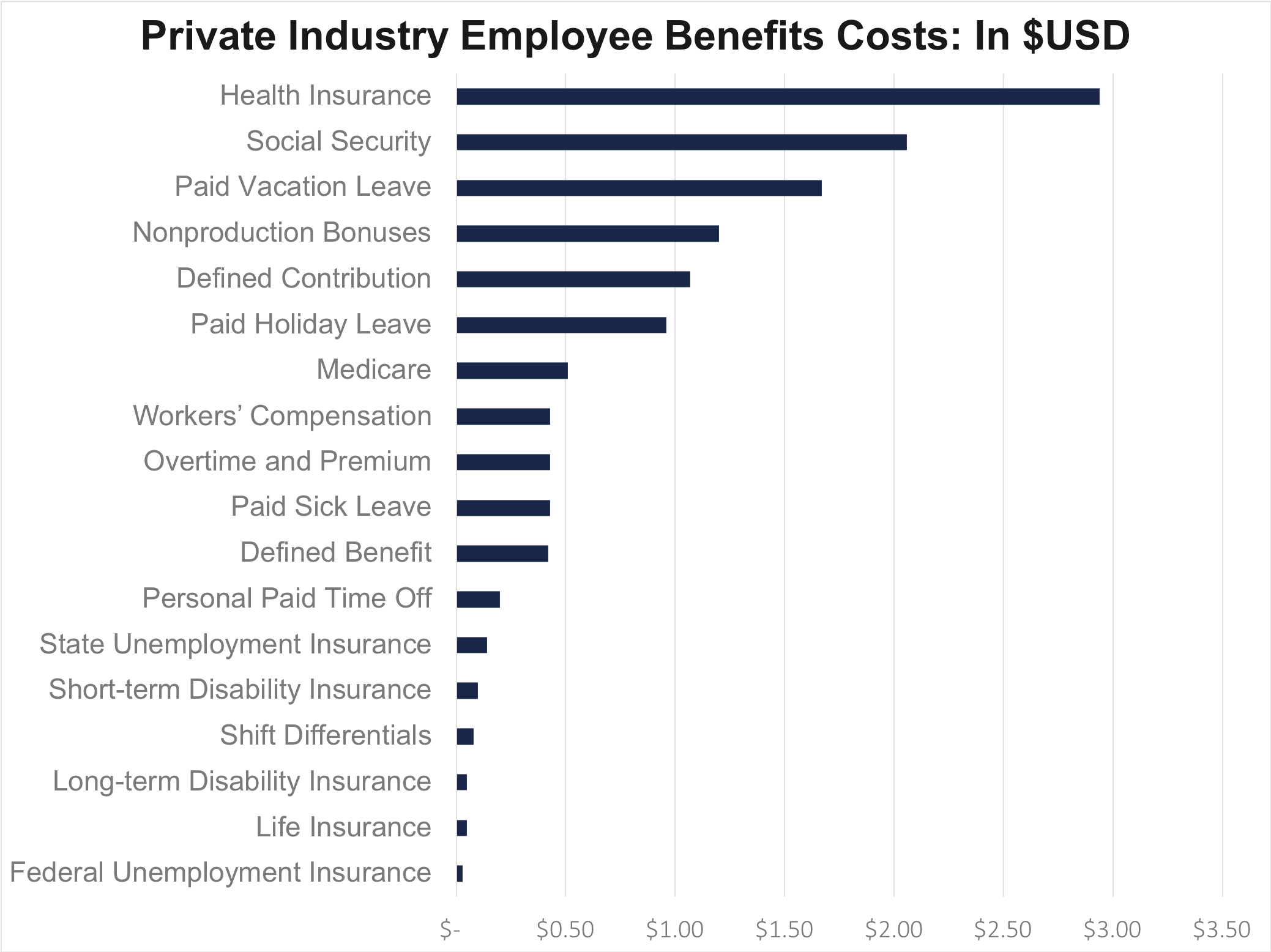

The 30% of total employee compensation expenses that went toward employee benefits can be further broken down, the largest portion of which went to health insurance of course, which cost private employers about $2.94 per hour per employee on average.

Social Security contributions were the next largest expense at $2.06 per employee per hour, followed by paid leave at $1.67, non-production bonuses at $1.20, and defined contribution benefits which cost employers an average of $1.07 per employee per hour in 2023.

Those 5 employee benefit expenses alone (totally $8.97 per employee/hour) accounted for more than 70% of the average total hourly employee compensation expense of $12.77 per hour.

The least expensive eight benefits expenditures combined to equal a little more than $1 in total cost per employee per hour, or a bit over 8% of the total average employee benefits expense.

While the list stacks up for the minor benefit offerings, with a negligible impact on cost. some of them are the most important to certain segments of employees. As noted above, the split between wages/salary expenses and employee benefits expenses was about 70% to 30%.

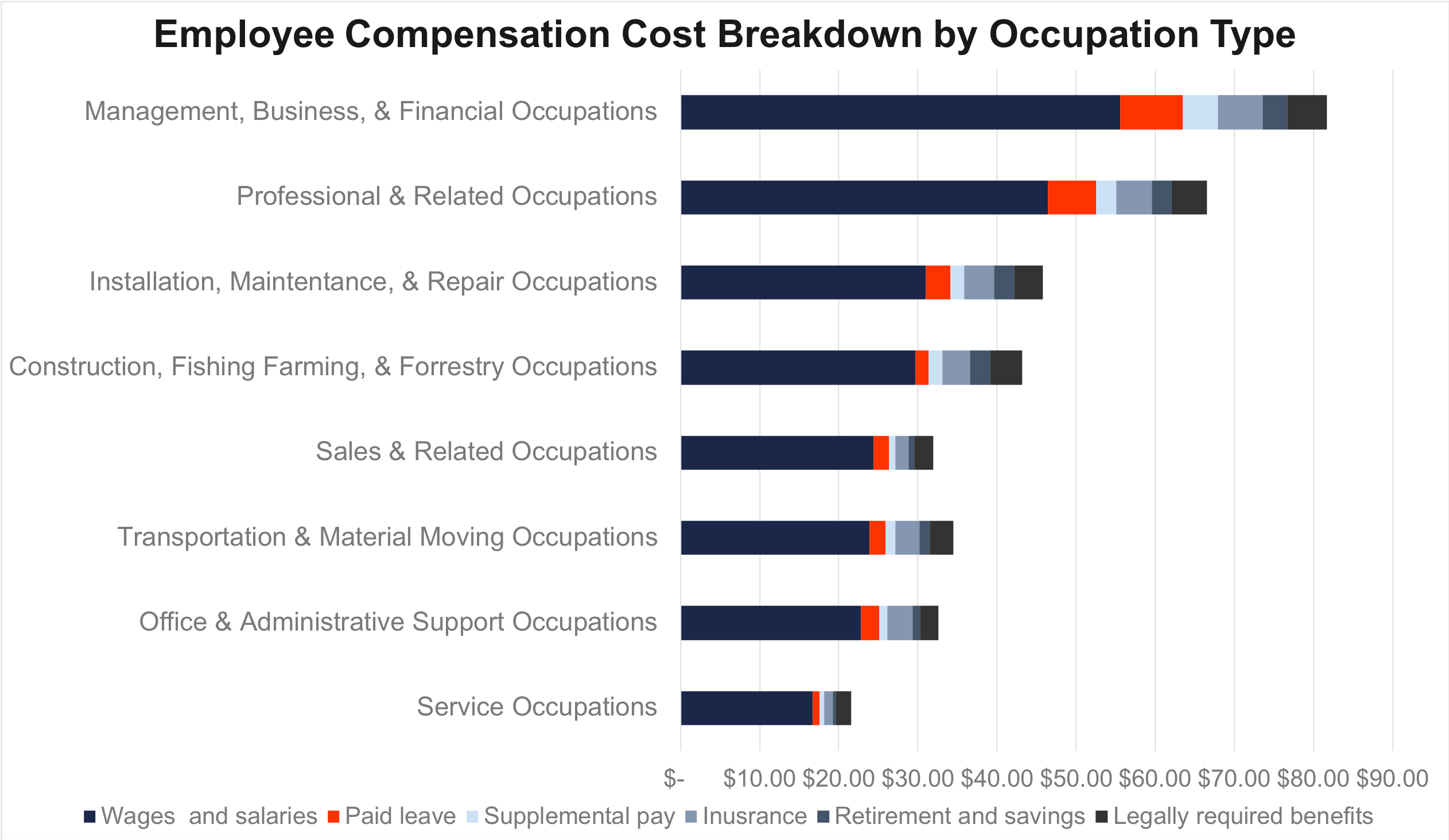

Employee Compensation Costs by Occupation Type

Next, lets look at the specific occupation. While workers in private industry cost their employers $43.11 per hour in total compensation expenses, those figures unsurprisingly varied quite significantly based on occupation type.

Management, business, and financial occupations had the highest average hourly compensation costs at $81.72, followed by professional and related occupations at $66.53.

Construction, fishing, farming, and forestry employees cost their employers an average of about $44.50 per hour in compensation expenses, while sales, transportation, and office and administrative employees had an average compensation expense of about $33 per hour. Service industry employees came in at the bottom of the list costing just $21.55 per hour in total compensation.

It is worth noting that the benefits expenses incurred for sales employees is surpassed by all other occupations outside service occupations, and although sales occupations pay higher wages and salaries than transportation and office/administrative jobs, transportation and office/administrative jobs are nonetheless more expensive in total compensation because of their relatively more substantial benefits offerings.

Employee Compensation Costs by Industry & Occupation

When accounting for both industry and occupation type at the same time, the combined effect that these independent factors have on average employee compensation expenses can be seen even more clearly, as in the following charts outlining employee compensation costs by industry, further broken down by occupation type.

For example, management, business, and financial jobs in the professional and business services industry cost their employers ($89.79 per hour) more than $12 more an hour in total compensation expenses than employees in the same field that work in the manufacturing industry ($77.56 per hour).

On the other hand, office and administrative support jobs compensation expenses were slightly more expensive in the manufacturing industry, albeit largely consistent across industries - $34.4 per hour in the manufacturing industry, $32.31 in the professional and business services industry, and $32.38 per hour in the trade, transportation, and utilities industries.

In a future installment, we’ll take a look at how these employee compensation expenses also vary by company size and region as well as how occupation and employee headcount combine to affect average hourly employee compensation cost.

.webp)